2021 Tax Update

WHAT CAN WE EXPECT IN THE UPCOMING TAX BILL?

On September 13, 2021, the House Ways and Means Committee released a list of revenue-raising items to be included in the upcoming fiscal year 2022 budget reconciliation bill.[1] These measures are designed to pay for various federal spending programs in the bill, known as the “Build Back Better Act.” Below we summarize the tax proposals that we believe will be of most interest to clients of 1919 Investment Counsel.

The final legislation, if and when it passes, will certainly be different than the proposed bill. However, the proposal lays out the framework for the approach Congress is taking. For most upper-income individuals, these changes are mostly “tweaks” to existing law, not fundamental changes. However, for some, the proposed changes could be more consequential. And for IRAs and grantor trusts, the changes represent a major shift in the rules of the game.

Most of the proposed changes would take effect on January 1, 2022. Apart from setting the effective date on the capital gains tax increase as of September 13, 2021, there are no retroactive taxes in the proposal affecting individuals, estates or trusts.

Proposed Tax Changes:

Individuals

- Increases top individual tax rate from 37% to 39.6% starting at $400,000 ($450,000 for married couples filing jointly)

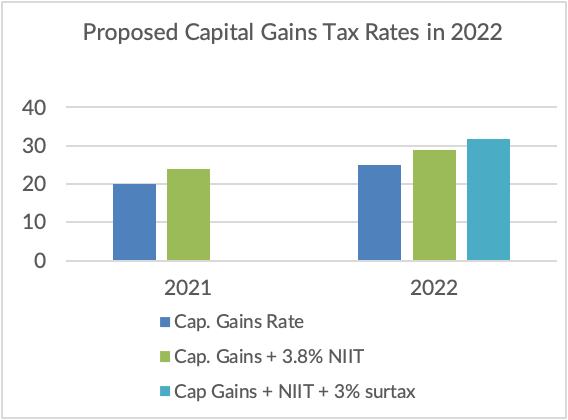

- Increases top rate on long-term capital gains from 20% to 25%

- This new rate would take effect on September 13, 2021

- Top tax rates for non-grantor trusts apply at $12,500 (per existing law)

- Qualified dividends are taxed at the same rate as long-term capital gains (per existing law)

- Imposes a new 3% surtax on modified adjusted gross income over $5,000,000 ($100,000 for trusts and estates) and applies to all types of income

- Tightens tax rules on crypto-currency transactions

Retirement accounts

- Prohibits contributions to traditional and Roth IRAs if you have more than $10 million in retirement accounts (includes IRAs and Defined Contribution plans)

- Requires that persons with more than $10 million in retirement accounts take withdrawals to reduce their balances

- Prohibits all Roth conversions for individuals with taxable income over $400,000 (or $450,000 for married couples filing jointly), which will prohibit “back-door” Roth conversions for affected individuals

- Prohibits after-tax contributions to employer-sponsored retirement plans (such as 401(k) plans), which will eliminate “mega back-door” Roth conversions

- Prohibits IRAs from holding investments in most types of private placements

Wealth transfer tax increases

- Reduces Federal estate, gift and GST tax exemption by half (from $10 million to $5 million plus inflation adjustments (and currently $11.7 million per person))

- This is an acceleration of the sunset provision in the Tax Cuts Jobs Act, which would have been December 31, 2025

- All grantor trusts created (or funded) after the date of enactment are included in the estate of the deceased grantor

- All transfers from new grantor trusts to anyone other than the grantor (or his or her spouse) would be treated as a taxable gift

- For example, GRATs created after the date of enactment are affected by these proposed changes and will become ineffective estate planning tools going forward

- However, existing GRATs are grandfathered

- For affected trusts, switching off grantor trust status would be treated as a taxable gift

- These rules would affect other types of grantor trusts as well

- For example, GRATs created after the date of enactment are affected by these proposed changes and will become ineffective estate planning tools going forward

- For grantor trusts created after the date of enactment, transactions with the grantor (such as swaps or sales) are treated as sales triggering capital gains recognition

- Prevents valuation discounting of non-business assets (such as family limited partnerships and LLCs) for lack of marketability, minority interests, and the like for transfer tax purposes

- Applies to transfers after the date of the enactment

What about the SALT deduction limitation?

- The Committee’s proposal does not include an increase in the State and Local Tax (SALT) deduction limitation (now $10,000 for all taxpayers). However, the Ways and Means Committee issued a separate statement saying they would be working on an increase in the SALT limitation. One possibility some insiders have mentioned might be a 2-year suspension of the limitation and then increasing the SALT cap to $40,000

- It is noteworthy that a resident of New York City who is subject to the 3% surtax could have an effective marginal tax rate of 61% under these new rules!

Corporations & Business Owners

- Increases top corporate tax rate from 21% to 26.5%, with graduated rates starting at 18% on the first $400,000

- Expands the category of income subject to the 3.8% Net Investment Income Tax (NIIT) to include income from businesses not otherwise subject to FICA taxes

- Imposes tighter limits on the Sec. 199A Qualified Business Income Deduction

- For carried interests (i.e., in-kind compensation for certain investment fund managers and real estate developers), the bill expands long-term capital gains holding period from 3 to 5 years

What’s not included in the bill?

- There is no mention of:

- Removing stepped-up cost basis at death

- Taxing capital gains at death or upon gift

- Increasing estate /gift tax rates

- Limiting annual exclusion gifts

- Limiting Sec. 1031 like-kind exchanges

- Raising Social Security taxes

- Imposing a new financial transactions tax

- Imposing a new wealth tax

The bill also doesn’t include things like “SECURE Act 2.0,” a new retirement overhaul which would, among other things, further postpone Required Minimum Distributions from IRAs to age 73 in 2022 and then out to age 75 by 2032. Nor does it include any reform of rules for private foundations or Donor Advised Funds, both of which have been targeted by certain lawmakers. However, much remains to be seen.

If you are considering making a large gift this year, we urge you do it soon.

Year-end planning (more urgent than usual)

If you are considering making a large gift this year before the estate and gift tax exemption could be reduced, we urge you do it soon. Not only is December 31, 2021, potentially a new deadline, but so is the date the tax bill is enacted (which could be a few weeks from now). Obviously, major steps such as this should done in consultation with your lawyer and tax advisor.

Since conversions to Roth IRAs could be eliminated for taxpayers with over $400,000 of income, we suggest evaluating whether to do a Roth conversion this year. Doing so would trigger a substantial tax for 2021 but a Roth IRA offers greater long-term tax deferral for your assets (no RMDs) and withdrawals are tax-free for you, your spouse and your heirs. Moreover, 2021 tax rates would apply on the conversion.

Conclusion

It seems clear that these proposals represent a partial undoing of the Tax Cuts and Jobs Act of 2017 and reflect an intention to tax wealthier taxpayers with incomes over $400,000. While most of these ideas fall within the existing statutory framework, a few of them, such as the new rules on very large IRAs and the 3% surtax, represent a major change for affected individuals. The proposed changes affecting grantor trusts also constitute a fundamental shift in the tax treatment of trusts as wealth transfer vehicles. However, the proposals don’t include such controversial changes as a Federal wealth tax or taxing capital gains at death.

The razor-thin Democratic majority will constrain Congress’ ability to pass some of these tax increases. Moreover, there are urgent needs, such as raising the debt ceiling, which will likely garner no Republican support, and which will put pressure on getting something passed ASAP. The result will be that some tax proposals end up on the cutting room floor.

We will issue another tax update in the coming weeks after we have more clarity. However, we think it is important to get this information out to you now so you know the state of affairs and can plan accordingly. Do not hesitate to contact your Portfolio Manager or Client Advisor about these and other matters of concern to you.

WARWICK M. CARTER, JR

Principal, Senior Wealth Advisor

Warwick M. Carter, Jr. is a Principal at 1919 Investment Counsel based in New York. As a Senior Wealth Advisor, his primary focus is generational wealth planning for high net worth individuals and families. He also advises on philanthropic planning. When giving advice, Warwick takes a comprehensive approach to assessing all aspects of a client’s tax, financial and family situation. Warwick works closely with Portfolio Managers and Client Advisors in all of our offices to integrate wealth strategies with a client’s investments. He regularly meets with outside advisors to devise appropriate solutions that will help grow wealth in a tax-aware way over the long term.

Warwick is a graduate of Denison University and the Columbus School of Law at The Catholic University of America. He also holds a master’s in taxation from Georgetown University. He is admitted to the bar in New York and the District of Columbia. Warwick is also a member of the New York State Bar Association and the Society of Trust and Estate Practitioners (STEP).

Email address: wcarter@1919ic.com

[1] Congress already passed one budget reconciliation bill in 2021 (The American Rescue Plan), which was for the fiscal year ending 2021. Congress will attempt to pass a second budget reconciliation bill in the same calendar year for fiscal year 2022. However, under House and Senate rules, only one such bill can be passed per fiscal year. Given the thin majority of Democratic lawmakers and the Republicans’ refusal to support any part of the bill, it will be critical to include as many high priority budgetary items as possible in the bill, such as an increase in the debt ceiling, which must pass by September 30, 2021.