Investment Review & Outlook - July 2025

Key Takeaways

- The impact of tariffs, immigration policies and the growing US deficit will likely keep US economic growth below 2%, although with the pause in tariff implementation and the enactment of the One Big Beautiful Bill (OBBB), the near-term risk of recession has subsided.

- Equity valuations remain elevated, leaving little room for government policy errors or disappointing corporate earnings. Above-average volatility should be expected after a quarter in which investors seemed to conclude that US policies and geopolitics will have little long-term impact on equity returns.

- Before cutting rates, the Federal Reserve will look for greater clarity around inflationary pressures from tariffs, as well as employment trends. Current expectations are for two rate cuts in 2025, which likely will result from signs of a slowing economy. However, rising US debt levels may pressure longer-term yields higher, regardless of Fed policy.

Total Returns and Values as of 6/30/25

| QTD Return | YTD Return | Price/Value | |

|---|---|---|---|

| Dow Jones Industrial Average | 5.5% | 4.5% | 44,095 |

| S&P 500 Index | 10.9% | 6.2% | 6,205 |

| Equal-Weighted S&P 500 Index | 5.5% | 4.8% | 7,373 |

| Bloomberg US 2000 | 7.8% | -3.0% | 1,493 |

| MSCI EAFE Index | 12.1% | 19.9% | 2,655 |

| MSCI EM (Emerging Markets) | 12.2% | 15.6% | 1,223 |

| Bloomberg US Aggregate | 1.2% | 4.0% | 93 |

| Bloomberg Municipal Bond | -0.1% | -0.3% | 100 |

| Gold (NYM $/ozt) Continuous | 5.0% | 25.2% | $3,307.70 |

| Crude Oil WTI (NYM $/bbl) Continous | -8.9% | -9.2% | $65.11 |

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

Economic Outlook

The US economy has remained relatively stable, with little discernible change after the April tariff announcements. Retail sales have edged downward, inflation has inched higher, currently at a 2.4% annual rate, and GDP growth has slowed. While none of these shifts constitute a significant change in economic momentum, and are not alarming in isolation, these indicators reflect a fragile equilibrium that has not yet felt the impact of tariff policy, geopolitical instability, and fiscal imbalances.

In early April, President Trump announced the most sweeping tariff hikes since the Smoot-Hawley Tariff Act of 1930, which are estimated to generate about $660 billion in revenue. Following 7 days of chaos, with the stock market dropping 12% and bond yields spiking, Treasury Secretary Bessent stepped in to calm the markets and implementation of most tariffs was delayed. Fiscal stimulus from the OBBB will help offset, to some degree, the higher cost of goods due to tariffs, but the final effect will not be known until negotiations are finished. Regardless, tariff revenue alone will not cover the additional spending in the OBBB, and US debt will continue to rise from an already unhealthy level of GDP.

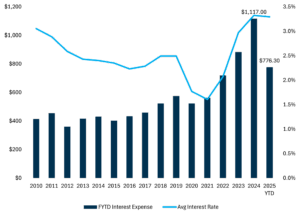

US Deficit & Debt Expansion – A Looming Fiscal Challenge

As is often quoted, it’s not a problem until it’s a problem sums up the US fiscal deficit and debt situation. While a growing federal deficit and related interest expense may not appear to be immediately critical, the risks have been rising quietly for years, with the potential to balloon into a serious economic challenge.

US government securities are a critical component of the global financial system, and their safe-haven role has allowed the US to finance its debt at favorable rates, keeping debt service costs relatively low. However, with nearly $36 trillion of debt outstanding, annual interest payments exceeding $1 trillion, and proposed legislation that will increase the deficit for years to come, this fiscal trajectory is unsustainable.

US Federal Interest Payments ($ Billions) vs. Average Interest Rate (%)

Source: The Bureau of Economic Analysis (BEA)

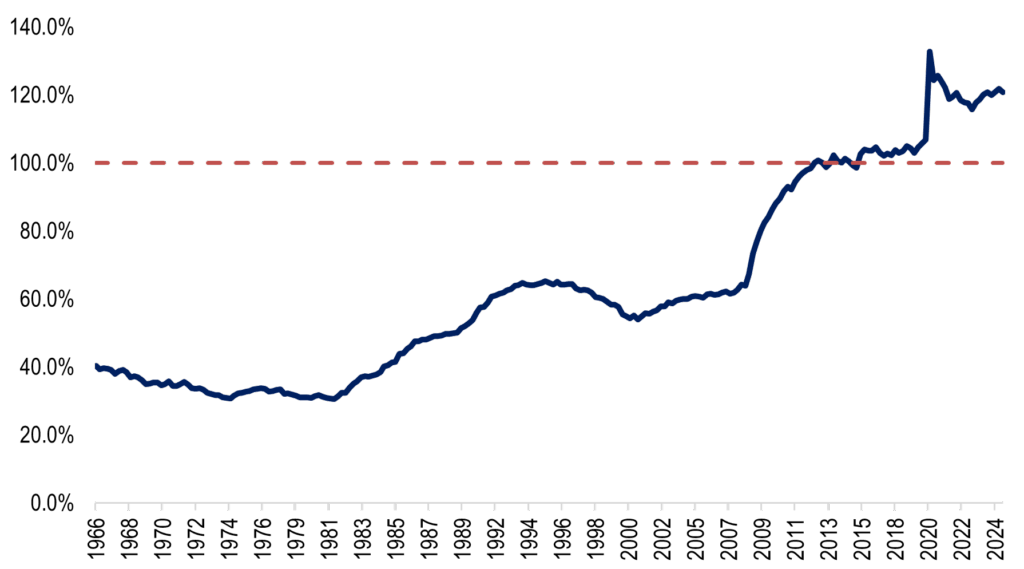

US National Debt as % of GDP

Source: Federal Reserve Economic Data, Federal Reserve Bank of St. Louis

As the deficit grows, bond investors may require a higher return in exchange for lending money to a more-leveraged borrower, the US government. This would result in higher bond yields, which, in turn, increase borrowing costs, posing a threat to the nation’s economic stability. As a result of sharply higher rates and increased borrowing, the current federal government interest cost is more than double the amount of five years ago. The nation now spends more on interest than it does on defense. If longer-term US Treasury yields breach 5%, we would expect a downward adjustment in valuations across equity markets.

Credit Rating Considerations

In May, Moody’s downgraded the US credit rating to Aa1 from Aaa, following similar actions by the other rating agencies, Fitch and S&P, that began in 2011. This downgrade was primarily driven by the nation’s growing deficit and the rising costs of debt service. However, Moody’s also noted a lack of fiscal discipline in Washington, political gridlock, and a diminished ability to respond in a future economic crisis as reasons for the credit change.

Budget deficit concerns have been reflected in indicators such as the US Dollar Index. The US dollar fell to its weakest level in three years, primarily due to concerns over tariffs and the outlook for the US economy. Year-to-date, the dollar has declined more than 8%. A weaker dollar makes imports more expensive for US consumers, which can add to inflationary pressures. However, it makes US goods and services more attractive to businesses and consumers outside the US, thereby supporting the domestic economy.

The Challenge of Policy Volatility

The current administration’s policy direction has been characterized by abrupt shifts that have created a challenging environment for capital allocation, business planning, employment, and investor confidence. Without clarity, companies struggle to plan and allocate resources for hiring, capital investments, and future growth. For equity investors, the tariffs announced in April triggered a market decline, dropping nearly to bear market levels (-20%) from the February market high, before rebounding sharply as the Trump administration paused or negotiated some of the tariffs.

Any escalation or failure to resolve trade tensions, especially with China, has the potential to disrupt supply chains, affecting corporate earnings and global competitiveness. We expect tariff-related price hikes to have a larger economic impact later in 2025 and into 2026.

Labor Market Challenges

The labor market has remained steady despite federal government layoffs and policy uncertainty. Companies are likely to stay cautious regarding hiring until the economic landscape becomes more predictable.

Immigration policies have led to some structural shortages, particularly in sectors that rely on low-wage or immigrant labor, such as hospitality, agriculture, construction. These labor shortages drive up costs because businesses must pay more to attract workers.

Concerns about the nation’s ability to attract and retain highly skilled global talent, which is a key factor for technological innovation, artificial intelligence, healthcare, and related frontier industries, are also present. The brain drain that may result from stricter immigration policies, as well as the defunding of universities and scientific research, can significantly impact the nation’s innovative and competitive edge, as talented workers seek employment elsewhere.

Monetary Policy & the Fed’s Outlook

The Fed remains cautious in its approach to monetary policy changes. While markets expect two rate cuts in 2025, the Fed is maintaining its data-dependent approach. Chairman Powell has resisted political pressure, stressing the importance of clarity on inflation, employment, and trade policy effects before reducing rates.

The US Consumer

Signs of stress among consumers are emerging, with a decline in spending despite some having purchased items earlier this spring before the tariff announcements. Retailers are carefully managing inventory and absorbing cost increases for now, but higher prices from tariffs that are passed on to consumers are likely to emerge later in the year. These increases will impact consumers during the key back-to-school and holiday shopping seasons.

The cost of food is another area of consumer spending that likely will become more expensive. Americans increasingly rely on food that is imported. With a 10% tariff rate in place on all imports and the potential for higher tariff rates as the administration’s pause expires, household food budgets are expected to rise. Likewise, domestic agriculture is an industry with a work force that is heavily reliant on immigrant labor. President Trump’s ongoing immigration crackdown may make it more difficult to fully staff US agricultural businesses.

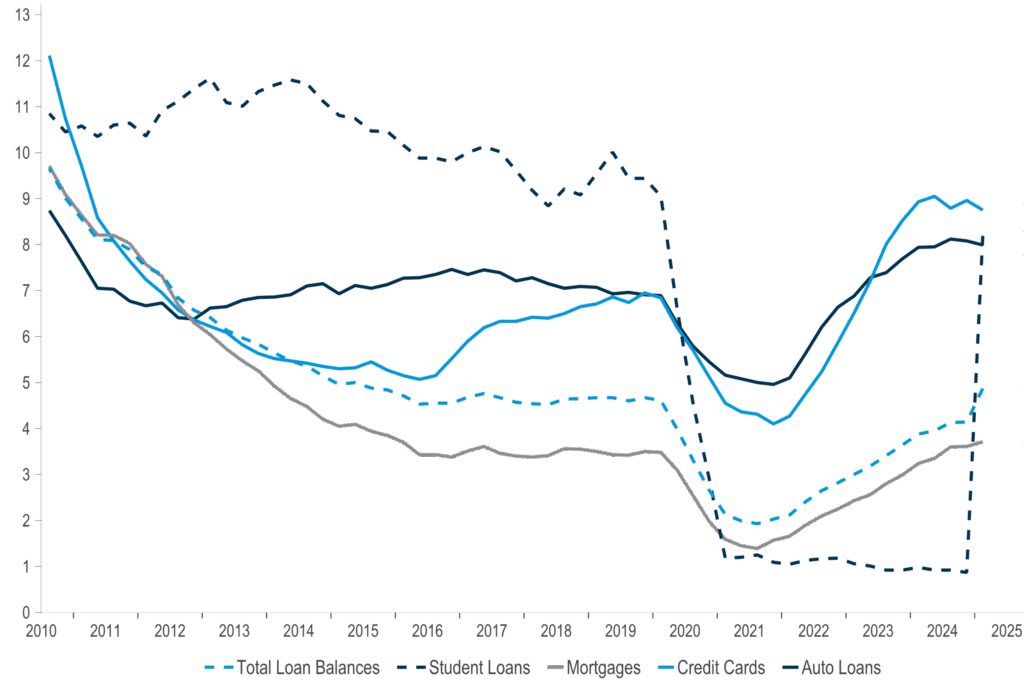

Tariff-related price hikes may also align with the resumption of student loan repayments. Student loan delinquency rates have risen to about 8.5% in 2025, reflecting financial strain on recent graduates and younger consumers. According to the New York Fed’s Center for Microeconomic Data, student loan balances reached $1.63 trillion in 2025, with a significant increase in the rate at which balances shift from current to delinquent, due to the restart of reporting student loans on credit reports after a five-year pause.

Delinquencies by Category

Source: FactSet

Equity Markets

Renewed Optimism, Valuations & Diversification

Information Technology stocks and those of related companies regained their appeal in the quarter. Led by Nvidia, many companies with expectations for double-digit sales and earnings growth continued to meet or exceed them. As tariff-related fears abated, investors reembraced risk and the hopes for robust growth offered by current and anticipated benefits of AI.

Concerns over changing policies for drug pricing, along with Medicare and Medicaid reimbursement rates, led to significant headwinds for stocks across the healthcare sector. While this policy uncertainty and related stock pressure may persist for several quarters, the valuations and underlying long-term fundamentals are attractive.

At the end of the quarter, equity valuations remained high, following a sharp rebound from the early April market decline triggered by the tariff announcements. The administration’s unpredictable stance on tariffs, immigration, and regulations was eventually shrugged off by investors who seemed to believe that if the markets dropped enough, the administration would backpedal and change policy.

For example, in early April, after the announcement of planned global tariffs, the S&P 500 neared a 20% decline from its February peak, which would qualify as a bear market. A few days later, on April 9th, when some of the tariffs were retracted or paused, the index rose nearly 10%, marking one of the largest one-day gains in S&P 500 history.

In this type of investment environment, diversification is not just prudent, it is essential. We expect this heightened volatility to persist for the remainder of 2025, as investors remain highly reactive to the latest headlines.

Looking beyond the near-term outlook, historical studies by Robert Shiller at Yale and others who are well-known for their examination of valuation and long-term returns (10+ years) suggest that lower long-term returns for large-cap US stocks may lie ahead, due to current elevated levels. While this analysis has limited value in planning for the next 1-5 years, it helps develop longer-term projections and manage expectations.

In addition to elevated valuations for large-cap US equities, there is concern about longer-term effects on stock valuations from a potential increase in bond yields if investors become more focused on US government deficits. Long-term bond yields rising above 5% would trigger investors to reprice risk assets, putting downward pressure on stocks.

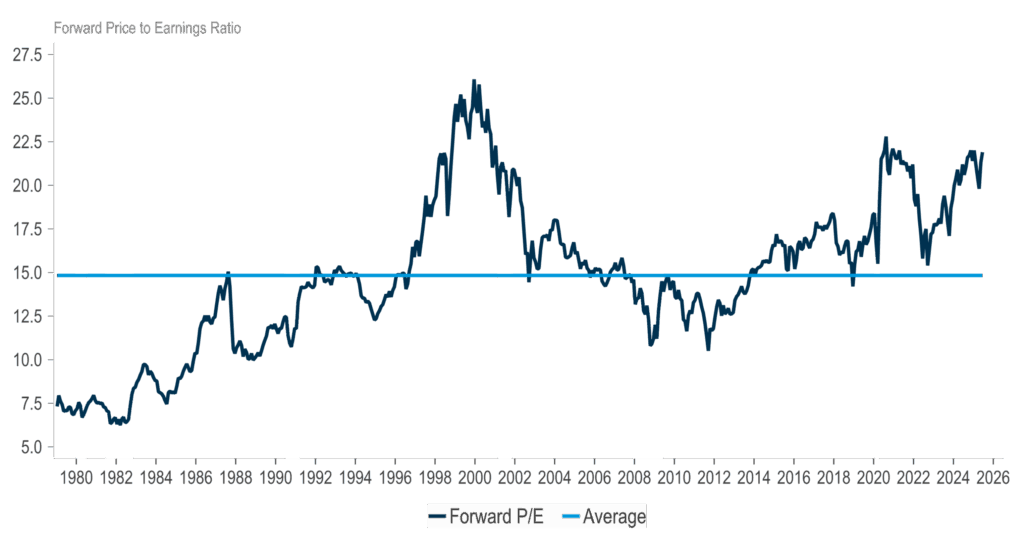

Equity Market Valuation

S&P 500 Price to Forward Twelve Months Estimated Earnings

Source: S&P Global, S&P 12M Forward Monthly data available from January 1979 to June 2025,last released on Monday, June 30, 2025

Fixed Income

Steady Despite Volatility

Following a tariff-driven rise in long-term rates, fixed-income markets stabilized, supported by strong demand for Treasuries, despite the weakening dollar. Credit spreads remain tight, indicating investor confidence that significant recession risk is contained for now.

However, the outlook remains complex. As deficit spending increases and Treasury issuance rises, there could be an upward pressure on yields. Strong demand for US Treasuries by international buyers also has played a large part in keeping the cost of US debt relatively low. However, the weakening US dollar may influence foreign demand for US bonds as it makes them less attractive to a foreign buyer. China has reduced its holdings of Treasuries to where its current holdings are 40% lower than the high reached in November 2013.

While a slowing economy and a weaker labor market will likely cause the Fed to lower the short-term Federal Funds rate, if investors become more concerned about US deficit spending, longer yields can rise, driven by increasing debt levels, regardless of Fed policy.

Closing Thoughts

Our Commitment to You

As stewards of your capital, we remain focused on what matters most: preserving and growing your wealth through all market cycles. We are actively monitoring the evolving landscape and adjusting strategies where appropriate, always with your long-term objectives in mind.

We appreciate the trust you place in us and look forward to continuing to serve you with insight, integrity, and care.

All information herein is as of March 31, 2025 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2025, 1919 Investment Counsel, LLC. MM-00001869