The One Big Beautiful Bill Act and How it Might Affect You

On July 4, 2025, President Donald J. Trump, signed into law the One Big Beautiful Bill Act (“OBBBA”), a budget reconciliation bill that passed both houses of Congress by the thinnest of margins. The Act makes permanent a number of expiring tax provisions that were enacted in the Tax Cuts and Jobs Act (“TCJA”) in 2017 during Trump’s first term. Most notably, the federal estate and gift tax exemption (now $13.99 million), which was set to revert to $5 million in January 2026, will be permanently increased to $15 million per person effective in 2026.¹ The OBBBA also introduces some new rules (such as “no tax on tips”) and eliminates clean energy tax credits (like the electric vehicle tax credit) and imposes new taxes on large college endowments.

In the course of the legislative process, there were several proposals in the House bill that ended up being substantially changed by the Senate (such as the “SALT” deduction and new savings vehicles for children called “Trump” accounts). A few of the House’s proposals were dropped in the final version (e.g., the “Revenge Tax” and increased taxes on the net investment income of private foundations). And the final Senate bill differed slightly from the one the Finance Committee issued, partly due to tweaks made by the Senate parliamentarian, who acts as an arbiter of what can be included in a budget reconciliation bill per the Senate’s rules.

The OBBBA consists of 870 pages of budgetary legalese and covers a wide range of matters. We will not attempt to summarize the entire Act here. We explain the parts that we think will be of greatest interest to you, our clients. We also highlight a few planning opportunities that are presented by the One Big Beautiful Bill Act.

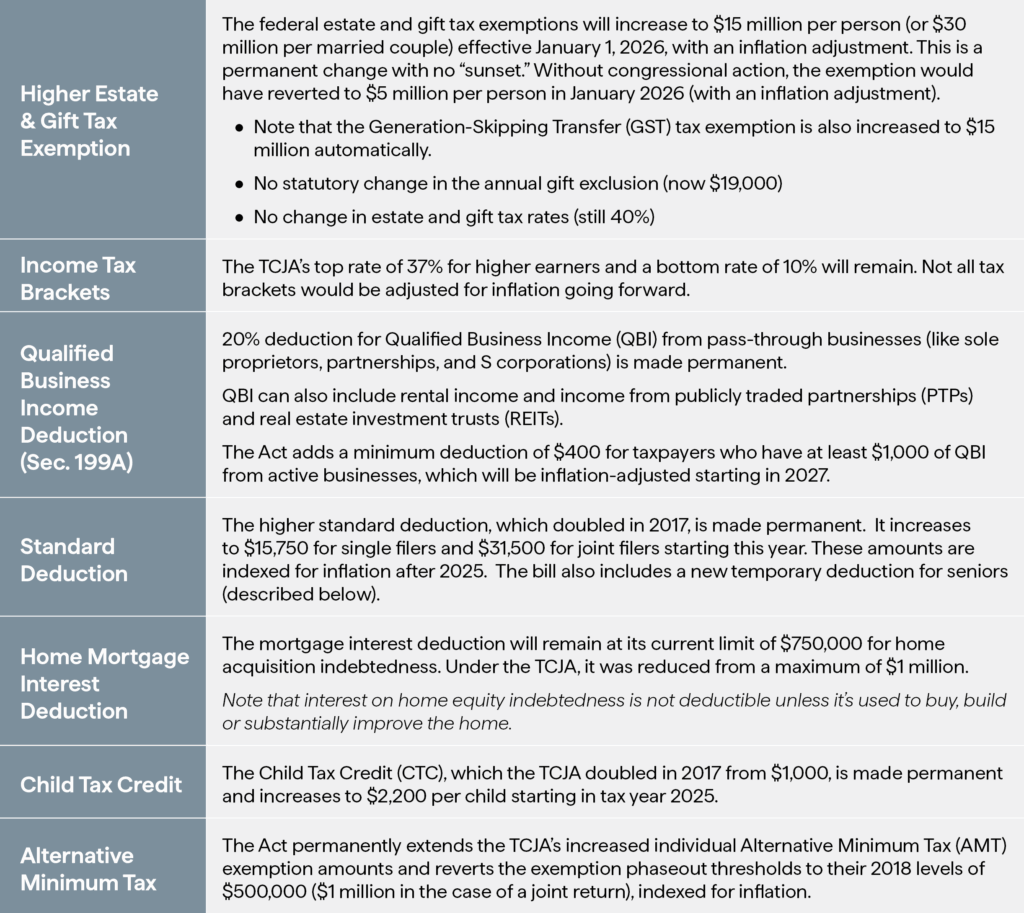

What Was Made Permanent

The Act makes permanent the following provisions enacted in the TCJA that were set to expire at the end of 2025.

What Changed

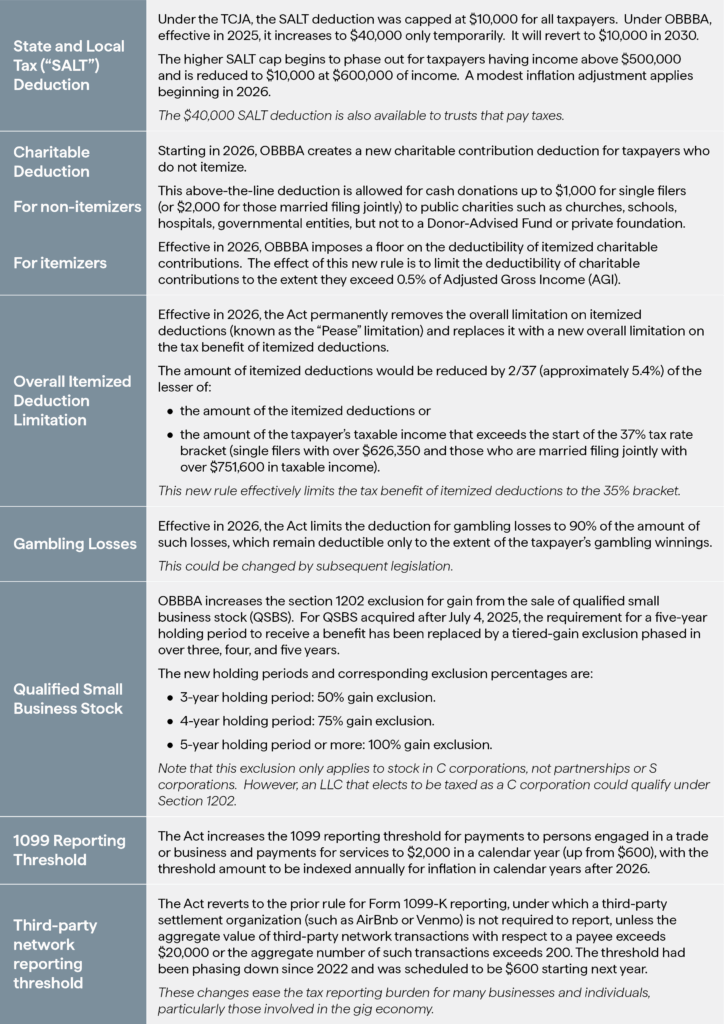

The OBBBA modifies several laws now in effect, the major one being the “SALT” (or state and local tax) deduction, which was capped by the TCJA at just $10,000 per taxpayer. Politicians in states that impose higher state and local taxes clamored for an increase in this deduction and got it, but it has some strings attached. Effective this year, the SALT deduction was quadrupled to $40,000 but is subject to a phase-out to $10,000 once income reaches $600,000. The $40,000 deduction cap will expire at the end of 2029 and revert back to $10,000 unless Congress changes it.

Another change is the reintroduction of the above-the-line charitable deduction for non-itemizers. This time, the deduction is $1,000 (instead of $300) per person. The Act also added a new 0.5% floor on charitable donations for itemizers. In addition, the value of any itemized deduction will be limited to the 35% bracket.

The Act also includes a new 90% limit on the deduction of gambling losses, which has become a hot topic lately. This rule could be repealed soon.

Planning Opportunities

SALT Deduction Limit and Pass-Through Entities

After the TCJA was enacted, many states enacted workarounds for people who are partners in partnerships or shareholders in S corporations (i.e., pass-through entities) to enable them to claim a full SALT deduction. While each state’s law is different, these workarounds provide a mechanism that allows a pass-through entity to elect to pay an entity-level state income tax (which would be deductible for federal purposes) and pass the resulting tax benefit along to its partners and/or shareholders as a state tax credit. This workaround was even approved by the IRS. The version of OBBBA that passed the House in May included provisions to limit taxpayers’ ability to circumvent the SALT cap through state pass-through entity taxes (or PTETs). The final version of the bill does not limit PTET workarounds, so they are still available.

Charitable Giving

The new 0.5% floor encourages taxpayers who itemize deductions to increase their charitable giving to overcome the floor and claim a deduction. Donors can concentrate their giving into a single year so as to exceed the threshold and receive a deduction. Taxpayers can also make donations of appreciated stock and claim a fair-market value deduction. Donor-Advised Funds (DAFs) remain an attractive vehicle for donors seeking a charitable tax deduction while retaining flexibility over grant recommendations. Donors in higher tax brackets who are considering a significant philanthropic gift may want to think about accelerating their charitable gifts in 2025 to maximize their deduction under the current rules before the new limits go into effect.

Example: If your AGI is $400,000 and you itemize, you will be able to deduct charitable contributions only to the extent they exceed $2,000 (i.e., 0.5% of $400,000). All other deduction limitations remain in place. Carryovers of excess charitable deductions are permitted up to 5 years.

What’s New

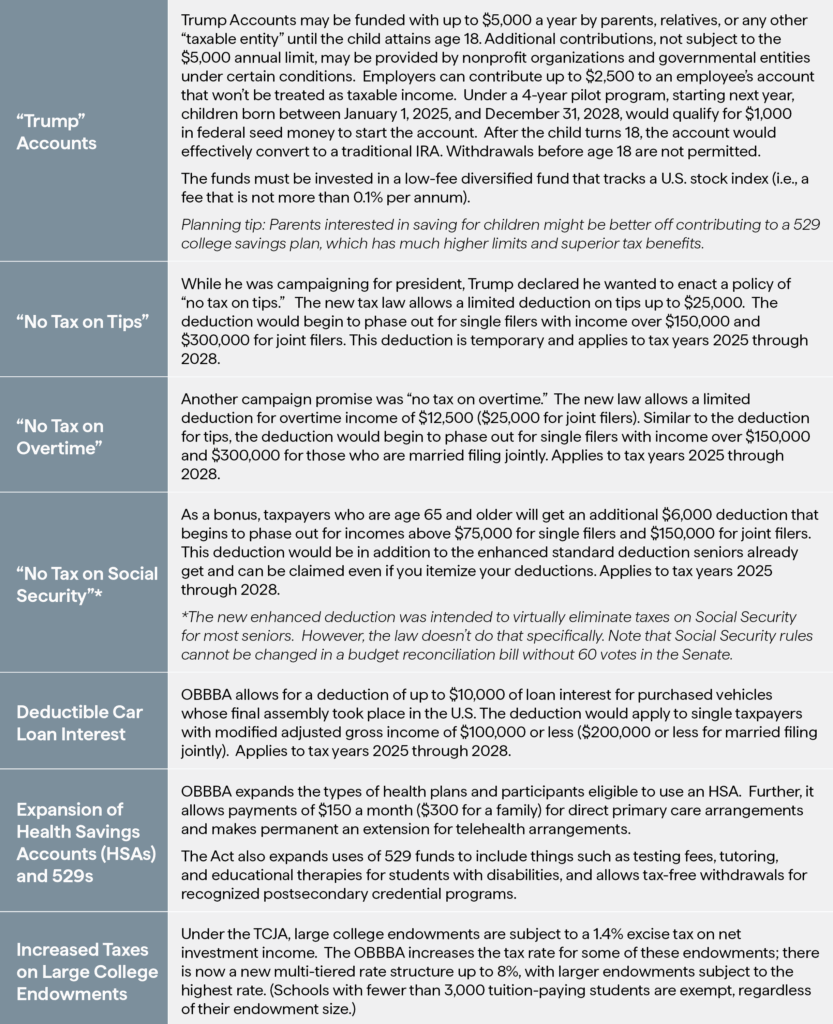

The OBBBA introduces a new savings vehicle called “Trump accounts,” which are a type of IRA for U.S. citizens under age 18.

What Was Eliminated

The OBBBA eliminates many clean energy tax incentives, including:

- Previously owned clean vehicle credit (terminates after Sept. 30, 2025)

- Clean vehicle credit (terminates for vehicles acquired after Sept. 30, 2025)

- Energy-efficient home improvement credit (terminates after Dec. 31, 2025)

- Residential clean energy credit (terminates for expenditures made after Dec. 31, 2025)

- New energy-efficient home credit (terminates after June 30, 2026)

Planning Tip: For those interested in buying an electric vehicle, the tax credit is still available until September 30, 2025. The credit is up $7,500 for a new vehicle and $4,000 for a used one if your modified adjusted gross income for either the current year or prior year not more than $150,000 (joint filers) or $75,000 (single filers) in addition to other conditions.

What Wasn’t Enacted

- A proposal to increase the tax on net investment income of large private foundations, akin to that for large college endowments, was included in the House bill but it was removed by the Senate and not enacted.

- There was also a proposal for something called the “Revenge Tax,” but it was rejected. That tax would have levied a retaliatory tax on entities from countries that impose taxes such as a Digital Services Tax and the global minimum tax. Wall Street analysts and Congress’s own official tax scorekeeper said the provision would create a disincentive for foreign investors in the U.S.

- A bill was proposed that would have allowed U.S. citizens living abroad who meet certain conditions to elect to be treated as nonresidents for income tax purposes without having to renounce their U.S. citizenship. As a result, they would not owe U.S. income tax except on U.S. source income. This provision didn’t make it into the OBBBA and has not advanced.

- Note that, under current law, the “foreign earned income exclusion” allows a U.S. citizen residing abroad to exclude up to $130,000 of foreign earned income

The One Big Beautiful Bill Act is a continuation of Donald Trump’s tax policies as enacted in the 2017 Tax Cuts and Jobs Act. It also represents a rejection of many Biden-era policies (such as tax preferences for clean energy). The OBBBA also makes good (albeit in a limited way) on a number of Trump’s campaign promises. It also delivers some sought-after modifications to the tax law, namely the permanent increase in the estate tax exemption and the enhanced SALT deduction. There are also a number of business-friendly provisions in the bill, such as bonus depreciation, research and development expensing, equipment expensing, and making permanent tax preferences for Opportunity Zones.

At 1919 Investment Counsel, we are available to answer your questions about the new tax bill and invite you to contact your Portfolio Manager or Client Advisor about these and planning matters. As with any tax-related issues, it’s crucial to stay up to date on the latest IRS guidelines and consult with a tax professional for specific advice.

FOOTNOTE

¹The exemption is indexed for inflation.

About 1919 Investment Counsel

1919 Investment Counsel is a registered investment advisor. Its mission for more than 100 years has been to provide investment counsel and insight that helps families, individuals, and institutions achieve their financial goals. The firm is headquartered in Baltimore and has offices across the country in Birmingham, Cincinnati, New York, Philadelphia, San Francisco and Vero Beach. 1919 Investment Counsel seeks to consistently deliver an extraordinary client experience through its independent thinking, expertise and personalized service. To learn more, please visit our website at 1919ic.com.

Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize. This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

Additional fees apply if a trust company acts as trustee; third-party fees (such as tax prep) may apply. Stifel Trust Company, N.A. and Stifel Trust Company Delaware, N.A. are affiliates of 1919. You are under no obligation to choose an affiliated trust company. Trust and fiduciary services are provided by Stifel Trust Company, N.A. and Stifel Trust Company Delaware, N.A. (collectively Stifel Trust Companies), wholly owned subsidiaries of Stifel Financial Corp. and affiliates of Stifel, Nicolaus & Company, Incorporated, Member SIPC & NYSE. Unless otherwise specified, products purchased from or held by Stifel Trust Companies are not insured by the FDIC or any other government agency, are not deposits or other obligations of Stifel Trust Companies, are not guaranteed by Stifel Trust Companies, and are subject to investment risks, including possible loss of the principal invested. Neither Stifel Trust Companies nor affiliated companies provide legal or tax advice. There is no guarantee that employees named herein will remain employed by 1919 for the duration of any investment advisory services agreement.

There is no guarantee that employees named herein will remain employed by 1919 for the duration of any investment advisory services agreement.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2025, 1919 Investment Counsel, LLC. MM-00001909

Published: July 2025