Healthcare Funding at a Crossroads: Policy Shifts Pressure Hospital Profitability and Investor Returns

Hospitals across the United States are entering a period of significant financial strain as shifts in Medicare, Medicaid, and federal research funding reshape how care is delivered and how capital is allocated. These pressures are emerging at a time when hospitals must invest heavily in modernization, from imaging systems to digital infrastructure, yet face rising costs and tightening margins. The impact is not uniform: academic medical centers and community hospitals are experiencing these headwinds differently, with important implications for patient care and for the companies that supply essential medical equipment.

Hospitals across the United States are entering a period of significant financial strain as shifts in Medicare, Medicaid, and federal research funding reshape how care is delivered and how capital is allocated. These pressures are emerging at a time when hospitals must invest heavily in modernization, from imaging systems to digital infrastructure, yet face rising costs and tightening margins. The impact is not uniform: academic medical centers and community hospitals are experiencing these headwinds differently, with important implications for patient care and for the companies that supply essential medical equipment.

For investors, understanding how funding changes affect hospital operations is increasingly important. Many of the companies that manufacture surgical robots, imaging systems, diagnostic tools, and other critical equipment depend heavily on hospital capital budgets. As policy shifts continue to influence the financial health of hospital systems, these downstream effects may shape both risks and opportunities across the healthcare sector.

The Rising Cost Burden Facing U.S. Hospitals

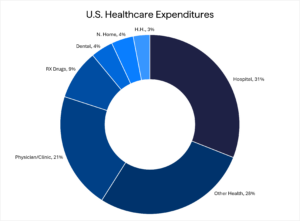

Against this backdrop, understanding the underlying cost structure of U.S. hospitals helps clarify why many systems are now under mounting financial strain. At 18%, Healthcare spending accounts for a significant share of U.S. GDP. Specifically, over $4.9 trillion is spent on healthcare per year, with hospitals’ expenditures accounting for a substantial portion. This is primarily a function of the infrastructure and capital needed not only to maintain a hospital, but to keep pace with medical innovation. These innovations are diverse and can range from sophisticated, such as robotic surgical systems, to mainstream, such as updated patient beds. On average, a hospital can spend over 10% of its operating expenses on non-durable medical supplies and devices (catheters, syringes, IV bags, etc.) and 25% of its annual capital budget on new equipment (imaging, robotic systems, beds, etc.) and renovations or expansion.

How Hospital Type and Patient Mix Shape Profitability

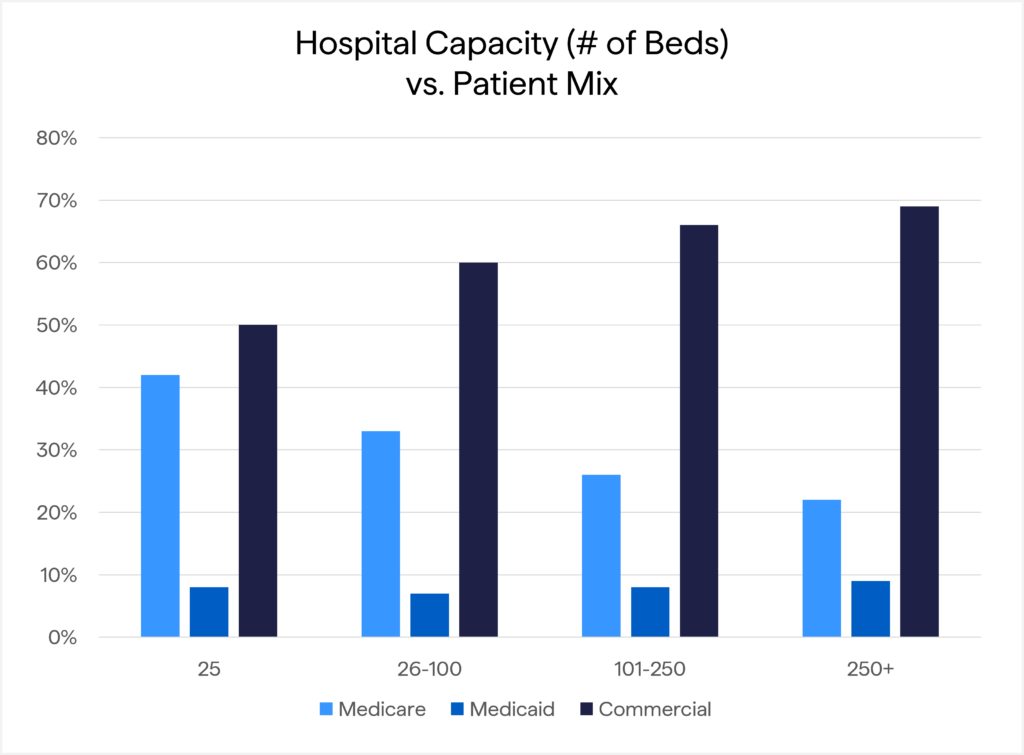

While cost pressures affect all hospitals, the financial impact varies significantly by hospital type and patient mix. Location (rural vs. urban vs. suburban), hospital type (academic and research vs. community), and payor mix (government vs. commercial) are each factors that can play a significant role in a hospital system’s profitability and its ability to keep up with technological and modernization changes. Community hospitals account for the vast majority (84%) of hospitals in the U.S. and, therefore, are responsible for the majority of inpatient care.

Academic and research hospitals may have enjoyed higher profitability for decades. Still, the 2025 cuts to National Institutes of Health (NIH) funding are also pressuring their margins and, in turn, their ability to maintain or upgrade their equipment and infrastructure. Unlike large academic and research hospital systems, the payor mix in the  community setting has a lower reimbursement rate, as their locations, often rural, are in communities with more Medicare and Medicaid-insured patients and fewer commercially-insured patients. This payor mix is challenging for community hospitals, as commercial rates are, on average, 100%-600% higher than the rates the hospital receives for Medicare and Medicaid patients. Therefore, given the higher reliance on Medicare and Medicaid, any changes to reimbursement or the patient base’s acuity levels (i.e. how sick the overall patient population is) could have a profound effect on the hospital system’s profitability. This, in turn, may affect its ability to purchase capital equipment, renovate or expand, and modernize its infrastructure and payment systems.

community setting has a lower reimbursement rate, as their locations, often rural, are in communities with more Medicare and Medicaid-insured patients and fewer commercially-insured patients. This payor mix is challenging for community hospitals, as commercial rates are, on average, 100%-600% higher than the rates the hospital receives for Medicare and Medicaid patients. Therefore, given the higher reliance on Medicare and Medicaid, any changes to reimbursement or the patient base’s acuity levels (i.e. how sick the overall patient population is) could have a profound effect on the hospital system’s profitability. This, in turn, may affect its ability to purchase capital equipment, renovate or expand, and modernize its infrastructure and payment systems.

Policy Headwinds: Medicaid Expansion Strains and Medicare Site Neutrality

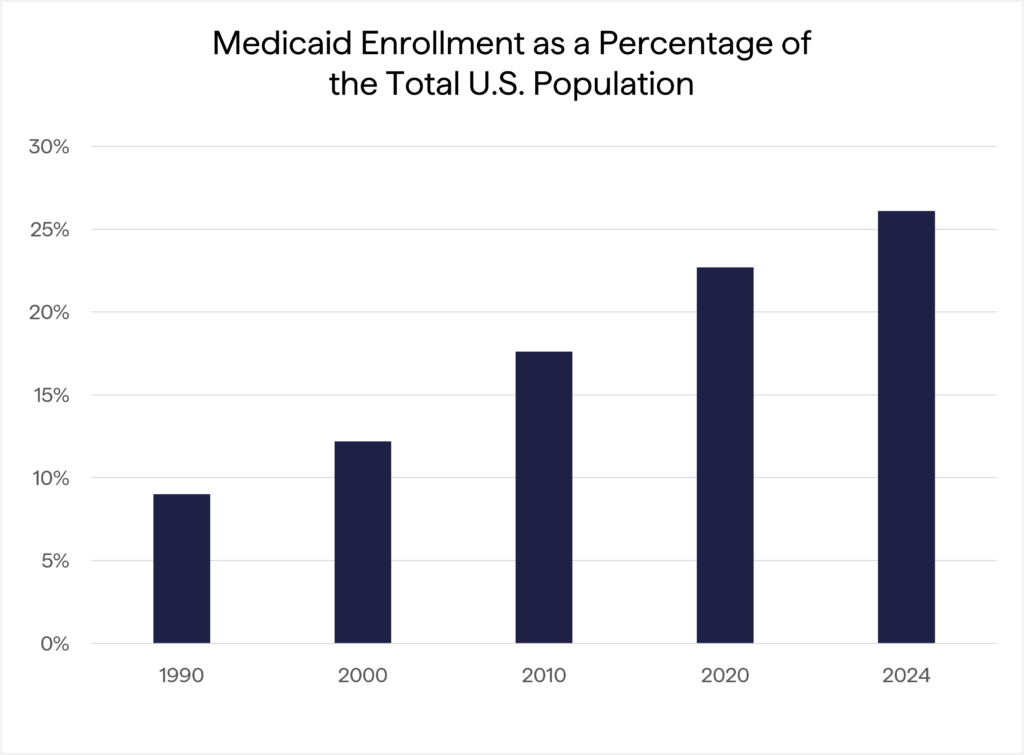

These structural differences are increasingly crucial as new policy developments add financial pressure, particularly for hospitals with greater government payor exposure. As part of the Affordable Care Act, passed in 2010, the Federal Government offered long-term funding to states that expanded their Medicaid programs. Specifically, the Federal Government would match 100% of the costs for newly enrolled Medicaid recipients, with the match decreasing over time after 2016. This led to substantial growth in Medicaid, with 26% of the U.S. population (approximately 89 million people) now covered by the program. Furthermore, Medicaid has increased its presence within a state’s budget, with annual spending now close to 30%, including the Federal match. This number could grow as medical inflation continues to accelerate, and most insurance companies that administer state plans lobby for higher rates, which the state pays per patient to the insurer. Given the increased Medicaid costs in states’ budgets, combined with a potential worsening of patient base acuity levels beginning in 2027 due to Medicaid-imposed work requirements, states may reduce their Medicaid roles as budgetary pressures increase.

As previously noted, Medicare is a significant funding source for community hospitals. One of the current issues facing Congress is the extension of Enhanced Premium support for adults with insurance through the Affordable Care Act exchanges. It is estimated that the cost of continuing enhanced support is $350 billion over 10 years, and the debate in Congress centers on funding sources. One proposal to close this funding gap is site neutrality for Medicare patients. In its basic form, site neutrality sets reimbursement rates at the same level regardless of where the procedure is performed (hospital, outpatient surgery center, or physician’s office). If this were to occur, the impact on hospitals would be negative, estimated at $150 billion, and could be larger if commercial insurers follow suit. However, site neutrality may improve patients’ access to care: outpatient treatment is often associated with a lower risk of infection or complications than inpatient treatment, and patient choice in where to access treatment may increase with the availability of closer-to-home procedures.

As previously noted, Medicare is a significant funding source for community hospitals. One of the current issues facing Congress is the extension of Enhanced Premium support for adults with insurance through the Affordable Care Act exchanges. It is estimated that the cost of continuing enhanced support is $350 billion over 10 years, and the debate in Congress centers on funding sources. One proposal to close this funding gap is site neutrality for Medicare patients. In its basic form, site neutrality sets reimbursement rates at the same level regardless of where the procedure is performed (hospital, outpatient surgery center, or physician’s office). If this were to occur, the impact on hospitals would be negative, estimated at $150 billion, and could be larger if commercial insurers follow suit. However, site neutrality may improve patients’ access to care: outpatient treatment is often associated with a lower risk of infection or complications than inpatient treatment, and patient choice in where to access treatment may increase with the availability of closer-to-home procedures.

Why These Shifts Matter for Investors

These policy shifts do not operate in a vacuum; they flow directly into hospital capital budgets and, ultimately, into the financial performance of the companies serving the healthcare ecosystem. If and when hospitals must put off spending to replace or upgrade equipment and infrastructure, patients’ care quality may suffer, but so too may healthcare sector investments. While an investment portfolio’s allocation to the Healthcare sector may not have assets directly invested in hospital systems, other companies will feel downstream financial effects of medical funding changes. Companies that manufacture durable equipment like MRI and other imaging systems, robotic surgical systems, ventilators, or other critical monitoring systems may be pressured and see their hospital sales slow. In alphabetical order, these companies may include Baxter International (BAX), GE Healthcare (GEHC), Intuitive Surgical (ISRG), Philips (PHG), Siemens (SIEGY), Smith & Nephew (SNN), Stryker Corp. (SYK), Zimmer Biomet (ZBH), among others.

Closing Thoughts

Taken together, these dynamics point to meaningful shifts for both hospital operations and the broader healthcare investment landscape. As policy changes reshape the economics of hospital systems, the resulting shifts in capital spending will be an essential driver of both risk and opportunity within healthcare. Our team continues to evaluate these developments and their potential impact on the companies serving this ecosystem. We welcome the opportunity to discuss what these dynamics may mean for your portfolio.

Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize. This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2026, 1919 Investment Counsel, LLC. MM-00002246

Published: February 2026