Investment Review & Outlook - April 2025

Key Takeaways

- Sharply escalating tariffs and an all-out trade war have introduced significant uncertainty for investors, consumers, and businesses. The result has been heightened concerns about stagflation, a phenomenon in which US economic growth slows while inflationary pressures rise, increasing the likelihood of a recession.

- Equity markets remain highly sensitive to the unpredictability of these economic crosscurrents, with investors attempting to navigate the impact of a trade war on valuations, corporate earnings, and market stability.

- The Federal Reserve is in a difficult spot, trying to ascertain whether slowing growth presents a more significant risk to the economy than higher inflation from tariffs. While two rate cuts in 2025 already were priced into forecasts, the Fed is unlikely to move until it has some clarity that inflation is under control.

Total Returns and Values as of 3/31/25

| QTD Return | YTD Return | Price/Value | |

|---|---|---|---|

| Dow Jones Industrial Average | -0.9% | -0.9% | 42,002 |

| S&P 500 Index | -4.3% | -4.3% | 5,612 |

| Equal-Weighted S&P 500 Index | -0.6% | -0.6% | 7,024 |

| Bloomberg US 2000 | -10.1% | -10.1% | 1,389 |

| MSCI EAFE Index | 7.0% | 7.0% | 2.401 |

| MSCI EM (Emerging Markets) | 3.0% | 3.0% | 1,101 |

| Bloomberg US Aggregate | 2.8% | 2.8% | 92 |

| Bloomberg Municipal Bond | -0.2% | -0.2% | 100 |

| Gold (NYM $/ozt) Continuous | 19.3% | 19.3% | $3,150.30 |

| Crude Oil WTI (NYM $/bbl) Continous | -0.3% | -0.3% | $71.48 |

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

Economic Outlook

At the end of the first quarter, US economic fundamentals looked solid, with low employment, declining inflation, and expected corporate earnings growth of just under 10%. Only a few days later, the sweeping tariff announcement on Trump’s self-proclaimed Liberation Day, with a proposed tenfold increase in the effective US tariff rate, set the stage to impact the cost of almost every imported good and has the potential to upend the growth trajectory of the US economy.

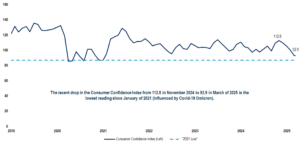

As we have written, the consumer is the biggest driver of economic growth in the US, responsible for about two-thirds of GDP, and tariffs act as a higher tax on consumers. Uncertainty around administration policies already had been weighing on consumers, as evidenced by declining spending and confidence levels. While initially concentrated among lower-income households, this spending caution has now spread to higher-income consumers who have contributed to recent economic growth due to the wealth effect of rising portfolios and home values. This trend may quickly reverse, given market declines.

Consumer Confidence Index

Source: FactSet

Additionally, corporations may find it difficult to move ahead with hiring or capital expenditure plans against such an uncertain policy backdrop. Supply chains built over decades face disruption, creating inefficiencies and additional costs that further pressure margins.

Likewise, the Elon Musk-led DOGE upheaval in the federal government and discontinued federal funding for universities, research organizations, and some non-profits has the potential for an increase in unemployment.

Recessions, a natural aspect of the business cycle, traditionally serve to correct some of the imbalances in excess production, investment, and spending that occur over time in a growing economy. Recessions also can be induced by government policy, as we expect will be the case in our forecast. In this environment, the forecasting challenge is the unpredictable nature and implementation of the Trump Administration’s tariff and DOGE policies. These uncertainties have damaged both consumer and business confidence, significant factors for economic growth.

Household financial stress indicators are flashing warning signals. Credit card and auto loan delinquencies have increased, particularly among lower-income consumers who tend to be most vulnerable to economic downturns. The scheduled resumption of student loan payments threatens to strain household finances further, potentially triggering additional delinquencies and reducing discretionary spending capacity. While the resilience of the US consumer is well-documented, we believe that the combination of uncertainty and accelerating headwinds significantly increases the likelihood of a recession.

The Fed’s Approach

While the Fed has ridden to the rescue in the past by lowering rates to stabilize markets or the economy, today it is navigating a complex economic landscape. Unlike in 2019, during the first Trump Administration, when the Fed lowered rates ahead of the trade war with China, inflation is higher now than it was then. At the March meeting, the Federal Open Market Committee maintained the Fed funds rate at 4.5%, while their latest projections for economic growth were lowered to reflect the reality of disruptive policies.

At the same time, the Fed revised its inflation forecast upward to 2.8%, acknowledging the persistence of inflationary pressures, although the forecasts were made before the magnitude of tariffs was known. While the baseline outlook includes two interest rate cuts before year-end, committee members remain divided on both the timing and magnitude of potential policy adjustments. Lower growth would necessitate lower interest rates, while higher inflation calls for rates to rise, as they did in 2022.

Late last week, after the tariff announcements, Powell said, “While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. The same is likely to be true of the economic effects, which will include higher inflation and lower growth. The size and duration of these effects remains uncertain.”

Tariffs & Trade Tensions

The president deeply believes that deficits mean that the US has been taken advantage of by its trading partners. Despite the fact that the service sector makes up over three-quarters of the US economy, Trump’s tariffs are an attempt to make up for decades of perceived injustice in the manufacturing sector where over the last several decades, jobs have shifted offshore, hollowing out industrial towns. Without years to prepare and a readily available pool of skilled labor, US manufacturers are in no position to replace imports within a reasonable timeframe, leaving consumers no choice but to pay the higher prices. Even when domestic production has ramped up enough to replace imports, the higher prices on those imports create cover for domestic producers to raise prices as well.

To offset the negative impact of tariffs on consumers and corporations, and therefore economic growth, Trump needs Congress to pass legislation to reduce individual and corporate taxes. At this point, the government is hoping for tax legislation to be passed by summer, which may be too late to forestall a recession. Ultimately, the economic impact of tariffs will depend on how high they stay and how long they remain in place. The more that tariffs cut into economic growth, the larger the tax bill will have to be in order to compensate, which could mean more government borrowing, and thus higher bond yields.

While certain domestic industries may benefit from reduced foreign competition, those that rely on imported components or materials, including the automotive, construction, and technology sectors, face significant headwinds. The potential for retaliatory measures, as has already been seen from China, further complicates the outlook, potentially escalating into broader trade conflicts.

Employment Market Dynamics

Labor market conditions, although still relatively strong by historical standards, may represent the calm before the storm. Businesses have become more cautious with hiring amid policy uncertainty, slowing the pace of job creation. Layoffs in sectors directly affected by federal spending changes, including government agencies and organizations dependent on federal funding, such as universities and non-profit organizations, are becoming a significant concern.

Lower-income workers disproportionately bear the brunt of economic slowdowns, experiencing both higher job insecurity and greater difficulty securing new employment, often living paycheck to paycheck. This demographic already has been significantly affected by the cumulative effects of inflation, with basic necessities consuming an ever-larger portion of household budgets. The record number of Americans working multiple jobs, the highest in history, underscores the financial pressure many households currently face.

Even without widespread layoffs, the perception of job insecurity can significantly impact consumer behavior. A fear of potential job loss often leads households to increase savings and reduce discretionary spending as a precautionary measure, creating a self-reinforcing cycle that can further slow economic momentum.

Recession Risk Assessment

While the US economy is not currently in recession, risk factors have intensified, particularly for US consumers who account for the largest percentage of growth. According to the National Bureau of Economic Research, a recession is defined as a significant decline in economic activity that is spread across the economy and lasts more than a few months. The most recent one, and one of the shortest on record, was during the early months of the 2020 COVID shutdown.

Over the last 75 years, the average duration of a recession has been approximately 11 months, varying due to the cause and the government’s response, with an average stock market decline of 31% from peak to trough. Since 1950, the average return of the market in the 12 months following a recession-market bottom was 40%.

The COVID recession is a great example. The initial market decline of 34% was sharp, quick, and unnerving. By the end of 2020, however, the market was up 18%. Even without a recession, administration policies that have been weighing on investors during the last month can be undone by the stroke of a pen, resulting in markets moving higher just as quickly as they declined.

The Specter of Stagflation

Alongside concerns about recession, the potential for stagflation has emerged as a serious consideration. Stagflation—the combination of stagnant economic growth, elevated unemployment, and persistent inflation—presents particular challenges for both policymakers and investors.

The 1970s provide the most notable historical example, when oil supply shocks and production constraints drove prices higher as economic growth stalled. This created a challenging environment in which consumers faced rising costs without corresponding wage increases or economic opportunities.

Current conditions exhibit some concerning parallels, with supply chain disruptions, rising inflation expectations, and uncertain economic policies potentially creating similar dynamics. If inflation remains elevated while growth decelerates, consumers may face the dual challenges of higher prices and limited income growth, which will further suppress spending and economic activity.

Silver Linings

Despite these challenges, several important strengths provide resilience to the US economy:

- Household balance sheets remain relatively healthy, with overall consumer debt-to-income ratios indicating that many families have sustainable financial positions.

- Corporate America took advantage of low interest-rate environments to strengthen balance sheets, extend debt maturities, and build cash reserves, thereby providing a greater ability to weather economic uncertainty.

- Potential policy developments, including tax cuts and regulatory reforms, could stimulate business investment and consumer spending, providing economic tailwinds.

- Technological innovation, particularly in artificial intelligence and related fields, continues to drive productivity improvements and create new growth opportunities across various industries.

Equity Markets

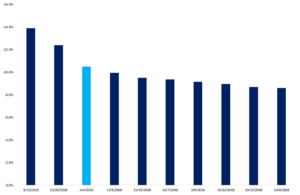

Recent market performance reflects the sensitivity of equities to the evolving economic narrative. After reaching an all-time high on February 19th, the S&P 500 dropped by as much as 21.4%, as investors processed the implications of the trade war, as well as concerns about inflation and slowing growth. Equities recovered some of the decline following a sharp rally on news of a 90-day pause in tariff implementation, leaving the market down 7.2% for the year (as of the close on Wednesday, April 9th). Adding to investors’ anxiety is the fact that the drop has been stunningly swift. From the 1950s to today, there have been only a handful of declines of this magnitude that have occurred this quickly. The most recent instance occurred at the onset of the COVID pandemic in 2020, when the federal and state governments essentially shut down the economy to mitigate the spread of the virus.

This correction highlighted vulnerabilities in a market characterized by concentrated leadership and elevated valuations, particularly among the largest companies by market capitalization. The sustainability of these valuations depends heavily on corporate earnings growth, which faces increasing pressure from both macroeconomic headwinds and rising input costs.

Largest 2 Day Declines in S&P 500 (since 2000)

Source: FactSet

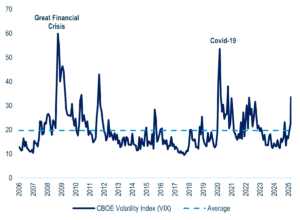

CBOE Volatility Index (VIX) Over Time

Source: FactSet

International Investment Opportunities

While challenges exist across global markets, international equities could present a compelling diversification opportunity. Many international markets trade at significant valuation discounts compared to US equities, creating potential for relative outperformance once economic conditions stabilize or improve.

External pressures from the trade war may accelerate necessary structural reforms in certain economies, potentially unlocking value for investors as margins expand, operational efficiencies improve, and earnings growth accelerates.

Fixed Income

Fixed-income investments offer important portfolio stabilization benefits amid equity market uncertainty, although bond investors must navigate their own set of challenges in the current environment.

The yield curve reflects two competing narratives: Fed policy anchoring short-term rates, while longer-term yields respond to inflation expectations and growth outlooks. The Fed has signaled potential rate cuts later this year, although rising inflation forecasts create uncertainty about the timing and magnitude of any policy adjustments.

Municipal Bond Dynamics

The municipal bond market presents interesting opportunities amid increased new issuance, with relative yields compared to Treasuries becoming more attractive than in the recent past. However, credit quality warrants careful consideration following the cessation of pandemic-era federal support programs. Focusing on higher-quality issuers remains prudent to mitigate potential downgrade risks in a challenging fiscal environment.

Corporate Credit Considerations

Corporate bond issuance has remained robust as companies continue to seek financing at still-favorable rates. However, as with municipals, credit quality deserves heightened attention given economic uncertainties and rising cost pressures. Companies may face challenges maintaining their financial health if economic growth slows further or input costs continue to increase.

Inflation expectations and fiscal policy uncertainty have increased risk premiums, prompting investors to demand higher yields for taking on credit risk. In this environment, emphasizing high-quality bonds—including select municipal and corporate issues—offers the potential for attractive yield while preserving capital.

Closing Thoughts

Periods of economic and market upheaval are very challenging for investors, who have been on pins and needles for much of 2025. We urge long-term investors not to overreact and jettison a well-considered investment strategy, especially one that takes into account market moves like investors have experience over the last week. Historically, the cost to a portfolio of attempting to get out of the market and then get back in again at opportune times is quite high. In the case of this tariff-induced market move, the situation remains quite unpredictable and can change on a dime.

At 1919 Investment Counsel, our mission is to guide clients through these complex environments with perspective, discipline, and personalized strategies designed to ensure long-term financial success.

All information herein is as of March 31, 2025 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2025, 1919 Investment Counsel, LLC. MM-00001717