Investment Review & Outlook - April 2026

Markets at a Crossroads: The Fog of War

Key Takeaways

The US war with Iran is overshadowing all other economic themes, as its effect on the price of oil has the potential to affect interest rates, GDP growth, and investor risk appetite.

- The longer the conflict drags on, the greater the strain on US and global economic growth. Higher oil prices act as a tax on consumers and businesses, which may override the benefits of the tax stimulus from recent legislation.

- Equity investors are hanging onto every news headline, resulting in heightened market volatility. Remarkably, the market decline has been relatively muted so far. Investors appear to fear missing out on a strong rebound if the conflict ends quickly, as happened last April after tariffs were announced and then abruptly put on hold. Corporate earnings are expected to grow in the low-to-mid teens, which should bolster stocks if the oil shock is short-lived.

- Fixed income markets are being pulled in opposite directions, putting the Federal Reserve in a difficult position for future monetary policy decisions. Traditionally, an unexpected geopolitical conflict would push yields lower as the demand for safe-haven bonds increases, but the spike in oil prices has the potential to exacerbate inflation, which would lead to lower bond prices and higher yields.

| QTD Return | YTD Return | Price/Value | |

|---|---|---|---|

| Dow Jones Industrial Average | -3.2% | -3.2% | 46,342 |

| S&P 500 | -4.3% | -4.3% | 6,529 |

| S&P 500 Equal-Weighted | 0.7% | 0.7% | 7,779 |

| Bloomberg US 2000 | 1.7% | 1.7% | 1,722 |

| MSCI EAFE | -1.1% | -1.1% | 2,839 |

| MSCI EM (Emerging Markets) | -0.1% | -0.1% | 1,397 |

| Bloomberg US Aggregate | 0.0% | 0.0% | 93 |

| Bloomberg Municipal Bond | -0.2% | -0.2% | 101 |

| Gold (NYM $/ozt) Continuous | 7.8% | 7.8% | $4,678.60 |

| Crude Oil WTI (NYM $/bbl) Continous | 76.6% | 76.6% | $101.38 |

The Economy

At the beginning of the year, the outlook for the US economy was positive due to a combination of a dovish Fed, fiscal stimulus, and corporate tax incentives. Consumer spending had been resilient, and unemployment was relatively low, both of which are good signs in the consumer-driven US economy. At the end of February, however, the focus quickly shifted to the US attack on Iran because of its potential to shape many parts of both the US and the global economy.

While geopolitical events often have transient economic effects, this conflict differs in that its influence on oil prices and supply could influence inflation, interest rates, and consumer behavior in a more sustained way.

There are two critical factors in determining the economic outcome: the duration of the conflict and the outcome that determines the end of the war. A short-lived disruption, with the Strait of Hormuz fully reopening, may result in only a temporary shock that the economy can absorb over several quarters. However, high oil prices for an extended period would become a structural, rather than cyclical, headwind to economic growth, placing sustained pressure on consumers and businesses. Similarly, an end to the conflict without a fully opened Strait of Hormuz also would keep prices elevated. We will leave aside, for now, the topic of a possible end to the war that leaves Iran controlling the Strait, an emboldened leadership, and an intact supply of enriched uranium, intensifying regional instability.

A slowing economy combined with higher inflation greatly increases the odds of a recession. While the price of oil has traded in the vicinity of $120 during the last month, looking one year out, oil futures are trading in the $70s, suggesting high confidence that the current conflict will be resolved quickly with minimal economic damage. It also, however, indicates that the markets could be caught off guard should this conclusion prove to be wrong.

Consumers: Resilient, but Increasingly Vulnerable

Consumer spending remained positive during the quarter, supported by wage growth and accumulated wealth, but the rate of increase has moderated. Recent retail sales data and consumer confidence surveys suggest that households are continuing to spend, but at a more cautious pace. Because consumer spending accounts for nearly two-thirds of US GDP, even modest shifts in sentiment can have an outsized effect on consumer behavior and, therefore, on economic growth.

Again, the key development this quarter has been the sharp rise in energy prices, but it is too soon to quantify the economic impact. Crude oil (WTI) increased approximately 77% over the past year, ending the quarter above $100 per barrel. Higher energy costs are particularly burdensome because they impact essential household and business budget items and are difficult to substitute. Higher gasoline, transportation, and home-energy costs function much like a tax on consumers, crowding out other discretionary spending while disproportionately affecting lower-income households.

While the US is less dependent on foreign oil than in prior decades, it remains a net importer of crude, particularly heavier grades required for domestic refining capacity. This structural mismatch, importing heavy crude while exporting light sweet crude from US shale production, means global energy prices still directly influence US consumers.

Importantly, the effects of higher oil prices radiate well beyond the consumer’s direct energy bill. Rising input costs for trucking, shipping, airlines, agriculture, and petrochemicals ultimately feed into broader goods and services inflation. As with tariffs and other input costs, businesses typically pass along a portion of these increases, reinforcing an inflationary backdrop that had already proven sticky prior to the recent geopolitical escalation. The combination of delayed purchases, a decline in discretionary spending, and deteriorating consumer sentiment may prove to be a headwind for economic growth.

Labor Market: Slowing, Not Contracting

Job creation has moderated, with monthly payroll gains averaging approximately 50,000 to 70,000 workers, well below the pace seen in prior years. The unemployment rate has drifted higher to the low-4% range, relatively tame but indicative of a softening trend that is unlikely to provide the same tailwind to consumption as in prior years. While the March employment report came in better than expected, it may have been influenced by seasonal factors and a shrinking of the labor force.

The labor market continues to operate in a “low-hire, low-fire” environment. Hiring activity has fallen to a six-year low, while layoffs remain subdued. Employers have become more selective, prioritizing productivity gains and cost control over workforce expansion. Consistent with a largely frozen labor market, average hourly earnings growth has been decelerating.

An additional layer of uncertainty stems from the accelerating adoption of artificial intelligence and automation. While the long-term productivity benefits are compelling, the near-term result may be a slower pace of hiring, particularly for entry-level and administrative roles. As observed in prior technological transitions, the timing mismatch between job displacement and job creation can create temporary labor-market friction.

Our Perspective

Throughout the remainder of 2026, the outlook for the US economy can best be described as stable but increasingly delicate. Growth persists, supported by consumer spending and targeted capital investment, but the underlying drivers are becoming less broad-based.

A notable feature of recent growth has been its composition. A significant portion has been driven by capital expenditures related to data centers, cloud infrastructure, and AI-related investment. While this spending has supported headline growth, it also introduces concentration risk, as a relatively narrow segment of the economy is contributing disproportionately to overall output.

Higher energy prices, a cooling labor market, and still-sticky inflation do not point to an imminent contraction, but they do suggest that the margin for continued expansion is narrowing. The trajectory of oil prices will be a key variable shaping the economic outlook. What begins as an energy shock can be a cyclical headwind that dissipates or can evolve into a more persistent force that puts upward pressure on inflation and interest rates while also dampening growth. The distinction between those outcomes will matter significantly for markets.

Equity Markets

Volatility Returns, but Drawdowns Remain Contained

Equity markets entered 2026 with a constructive backdrop, supported by expectations for above-average earnings growth, broader market participation beyond a narrow group of tech stocks, and continued economic expansion. Late in the quarter, however, geopolitical tensions and rising energy prices introduced new uncertainty, driving volatility higher along with a more cautious investor stance.

Market sentiment has become highly reactive to geopolitical headlines, with investors responding quickly to developments in the Middle East and their economic implications. This headline-driven environment has led to elevated day-to-day volatility, as investors weigh near-term risks against longer-term opportunities.

Despite this, the overall market decline has been relatively muted, with equities down roughly 7% at quarter-end from the all-time high reached in late January. A key factor has been investors’ reluctance to sell stocks too aggressively, for fear of missing out on a rapid reversal. Last year’s sharp but short-lived drawdown, triggered by tariff announcements that were quickly followed by a reversal and a strong recovery, remains fresh in investors’ minds. The fear of missing a similarly swift rebound has provided a degree of underlying support for equities, even amid policy unpredictability and rising uncertainty.

A Shift Toward Defensive Leadership

Early in the quarter, equity markets were modestly positive with investor focus centered around two primary concerns: the number of Fed rate cuts in 2026 and the magnitude of further AI infrastructure buildout alongside the pace of AI adoption. While these issues remain relevant, they have since taken a backseat to the war.

As geopolitical risks intensified and oil prices moved higher, equities declined for five consecutive weeks, and market leadership shifted meaningfully. Sector performance reflected the increasingly defensive tone.

Energy, materials, and consumer staples not only outperformed other sectors but also posted gains in a negative quarter, benefiting from their traditionally defensive characteristics and rising commodity prices. In contrast, growth-oriented sectors, including information technology, communication services, and consumer discretionary, declined during the quarter.

This rotation is consistent with prior periods of heightened uncertainty and inflation risk, during which investors favored sectors with more stable cash flows, pricing power, and less direct exposure to rising input costs. It also reflects a reassessment of risk as interest rates moved higher and the economic outlook became less certain.

Earnings Remain a Key Support, For Now

Consensus expectations for corporate earnings remain constructive, with forecasts calling for low-to-mid-teens growth in 2026. If realized, this trajectory should provide fundamental support for equity markets, particularly if there is a clear end in sight to the war. This earnings growth would help offset some of the headwinds from higher interest rates and elevated valuations.

However, the timing of earnings visibility is important. As we enter the upcoming reporting season, it will be too early to see the full impact of higher oil prices and geopolitical disruptions reflected in corporate results or management guidance. An extended period of higher oil prices may cut into margins and corporate profits.

Additionally, a significant portion of recent earnings growth has been driven by capital expenditures by large technology and hyperscale companies, particularly in AI and data center infrastructure. This concentration introduces an element of risk, as broader market performance remains partially dependent on ongoing massive cap-ex spending and execution by a relatively small group of companies.

Valuations and Interest Rates: A Delicate Balance

Equity valuations remain elevated by historical standards, although they have moderated somewhat following the recent pullback. Even with this adjustment, multiples continue to reflect a relatively optimistic outlook for growth and profitability.

A key risk to this valuation framework is the path of interest rates. As we have discussed in prior reports, there is a well-established inverse relationship between interest rates and equity valuations. Higher rates increase the discount rate applied to future earnings, which can compress price-to-earnings multiples.

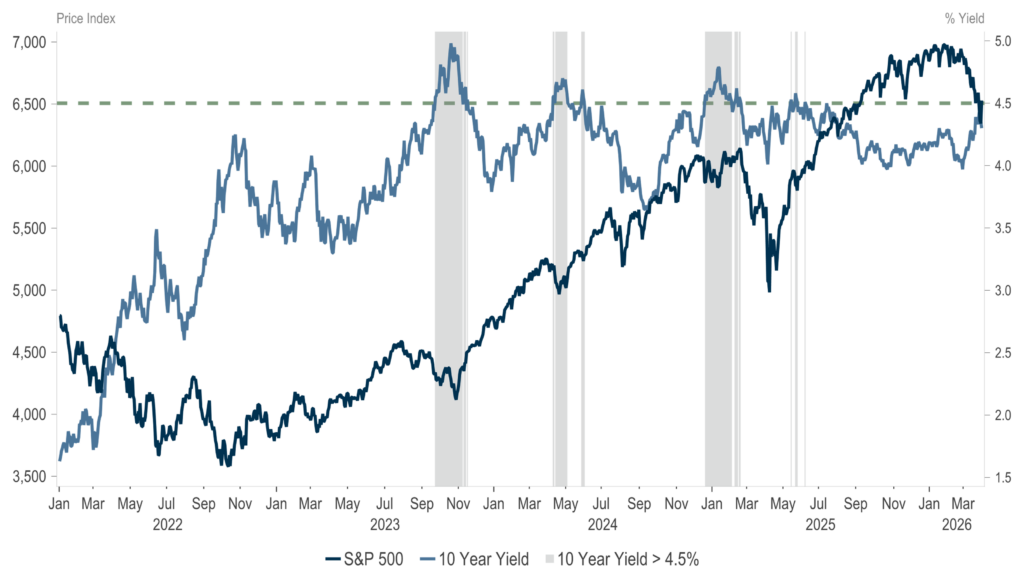

With the 10-year Treasury yield moving toward the 4.5% level, this dynamic becomes increasingly relevant. Rising yields not only challenge equity valuations directly but also increase competition for investor capital, if fixed income offers relatively attractive returns with lower volatility.

4.5% 10-Year Red Line for Risk

S&P 500 vs. 10 Year Yield > 4.5%

Source: Macrobond, S&P Global, Federal Reserve

Data: Daily as of 3/31/2026

The interaction between earnings growth and interest rates will be critical in determining market direction. Strong earnings can support equities, but sustained upward pressure on rates may limit multiple expansion and, in turn, overall returns.

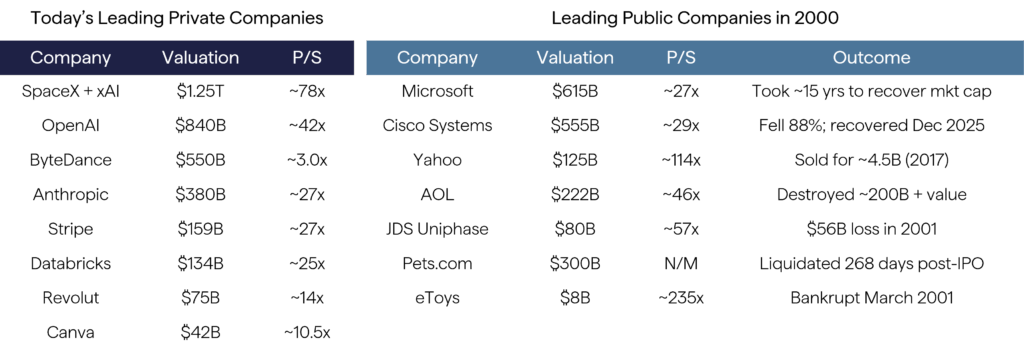

Adding another layer to the valuation discussion is the growing anticipation around AI-focused companies planning to go public. Wall Street enthusiasm regarding potential IPOs, starting with SpaceX, has intensified, with investors eager for exposure to the next generation of technology. This optimism echoes prior cycles where transformative technologies fueled lofty expectations well ahead of proven, durable cash flows. While some of these companies may ultimately justify premium valuations, it is unlikely all will live up to the hype. Below is a chart comparing price/sales (PS) valuations of today’s leading private companies to leading internet companies at the peak of the dot-com bubble. While fundamentals drive growth, valuation also matters.

Speculative Excesses Seen in the 2000 Bubble Have Returned, in the Private Markets

As capital becomes more selective, public market investors eventually will scrutinize the profitability, scalability, and capital intensity of the business models.

Fixed Income

Bond Investors Pulled in Opposing Directions

The combination of geopolitical risk, rising energy prices, and persistent inflation has created a uniquely challenging environment, one in which bond investors are being pulled in opposing directions.

Inflation remained above the Fed’s target entering the quarter, particularly in services and energy-related categories, and now faces additional upward pressure from rising oil prices. For fixed‑income markets, this dynamic matters less in isolation than in how it influences interest‑rate expectations across the yield curve.

Higher energy costs, combined with still‑elevated wage pressures, raise the possibility that inflation could reaccelerate modestly in the near term, complicating the outlook for policy and pressuring longer‑term yields. The risk is that inflation proves sticky enough to limit the traditional defensive role of longer-term bonds, even as growth shows signs of slowing.

Until there is greater clarity on whether higher energy prices fade or persist, yields are likely to remain range‑bound, with a bias towards higher, reflecting continued uncertainty about inflation. Additionally, the increase in defense spending is adding to the already large US fiscal deficit, another factor that has put upward pressure on longer-term yields. Massive US deficit spending is funded by increasing issuance of US Treasuries. Given an unsustainable path of fiscal policy, investors eventually may demand higher yields to buy the securities that underpin the spending.

The rise in yields during the quarter is particularly notable, given the broader context of a highly leveraged economy. Beyond the impact on US government deficits, higher yields increase borrowing costs for households and corporations, with implications for everything from mortgage rates to corporate investment decisions.

The Fed’s Dilemma

These opposing forces of inflationary pressures and slowing growth place the Fed in a difficult position, given its dual mandate of price stability and full employment.

As Chair Powell noted in his latest press conference, the Fed is in a position to “stand pat for now” as it assesses the evolving impact of geopolitical developments, inflation trends, and labor market conditions. This measured approach underscores the lack of clarity in the current environment and the risks of acting too quickly in either direction.

Complicating matters further is the upcoming transition in Fed leadership, with a new chair, presumably Kevin Warsh, expected to start later this year. Despite a distinguished career as a policy advisor to President George W. Bush and as a Fed governor, he is expected to face intense political pressure to lower rates. Concerns about Fed independence amid higher inflation, coupled with extraordinary levels of US debt and deficits, introduce significant uncertainty for bond investors.

Credit Markets: Stability with Emerging Risks in Private Credit

The demand for investment-grade bonds has remained relatively stable, supported by solid corporate balance sheets and continued investor demand for income. However, beneath the surface, areas of potential vulnerability are emerging, particularly within private credit and private equity markets.

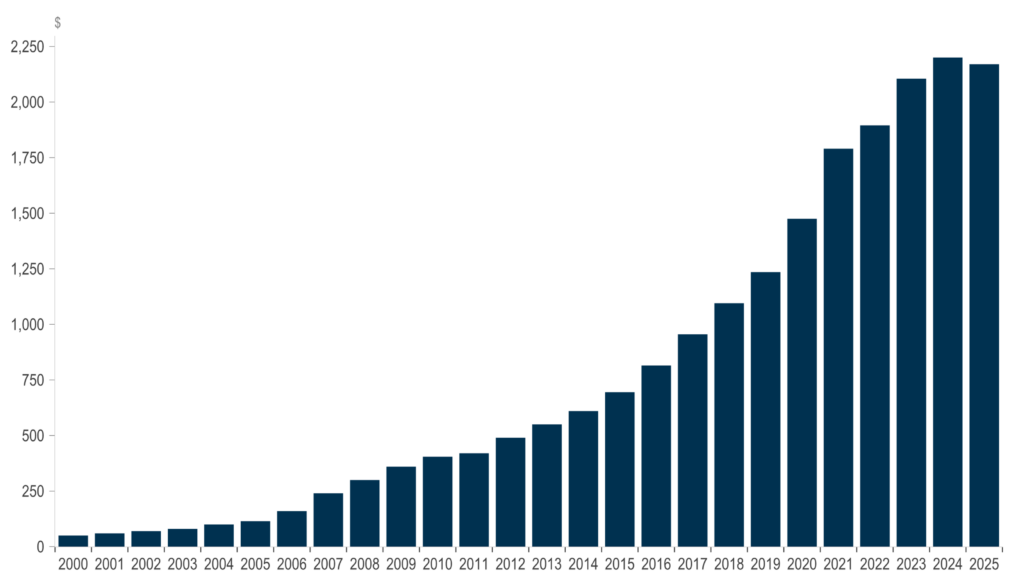

Following the Global Financial Crisis, regulatory changes reduced the role of traditional banks in corporate lending. Private equity and private credit firms stepped in to fill this gap, creating a rapidly expanding ecosystem of unregulated non-bank lending, in many instances to lower-quality borrowers. This market has grown to roughly $1.8 trillion today, representing approximately 1 to 2% of the total lending market. Now this market is poised to expand beyond institutional investors into the retail channel as demand from traditional sources of private capital, such as university endowments, has dried up. Recent legislation has been proposed to allow private investments to be held in individual retirement accounts and 401ks.

Global Private Credit AUM

USD billions, end of period total

Source: Federal Reserve, JPMorgan Asset Management

Data: Annual from 2000 – 2025

Private equity and private credit had been viewed as attractive portfolio diversifiers in part because they appear less volatile than publicly traded assets. However, private investments typically are marked-to-market less frequently than the daily requirement for public securities, often only quarterly. As a result, volatility is effectively smoothed over rather than eliminated, which can mask changes in fundamentals during periods of stress.

Recent moves by private funds to enforce strict redemption limits underscore the liquidity constraints associated with these investments. Such measures highlight the trade-off investors make between perceived stability and liquidity. Additionally, a significant portion of the private credit market is tied to private equity investors, with banks often originating loans that are subsequently distributed to private credit funds. While the funds serve as collateral for lenders, there is concern that the same collateral could be used for loans more than once.

While these developments do not yet represent systemic stress, the private credit markets have not yet been through a full economic cycle, including a major downturn. The combination of complexity, increased leverage, lack of transparency, and unknown credit quality of the underlying investments introduces an additional level of risk, especially at a time when the investor base may be expanding into retail.

Conclusion

At the end of the first quarter of 2026, geopolitical developments, most notably the US conflict with Iran, have moved to the forefront, introducing uncertainty that cuts across economic growth, inflation, interest rates, and both bond and equity markets. The resulting rise in oil prices has acted as a powerful shock, testing both the resilience of the expansion and the flexibility of monetary policy.

Ultimately, what will matter most is not the existence of this shock, but its duration and persistence. A brief disruption would likely register as a cyclical headwind, uncomfortable but manageable for the economy, consumers, and the corporate sector that began the year on a relatively solid footing. A more prolonged period of elevated energy prices, however, would represent a more meaningful structural challenge, acting as a sustained drag on consumer and corporate budgets while reinforcing inflationary pressures.

Importantly, this is not an unfamiliar environment for long‑term investors. Periods when markets are caught between growth concerns and inflation risk, and when headlines drive short-term volatility, have occurred many times across market cycles. While each episode has its own catalysts, the common thread has been the ability of having a disciplined investment strategy and a diversified portfolio to navigate these transitions more effectively than reactive strategies driven by near‑term headlines and emotions.

Today, both equities and fixed income reflect competing forces rather than a single dominant narrative. Our focus remains on maintaining appropriate risk exposure, emphasizing durable businesses and high‑quality income, and preserving the flexibility to adjust as conditions evolve.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2026, 1919 Investment Counsel, LLC. MM-00002382