Investment Review & Outlook - October 2025

Key Takeaways

- A relatively robust level of consumer spending bolstered US economic growth in the quarter, despite signs of a softening labor market.

- Equity market performance has been driven by a select group of AI-related mega-cap companies that have had an outsized impact on equity market movements.

- Despite its rate cut of 25 basis points resulting from concerns about the labor market, the Federal Reserve will continue to strive for a level of interest rates that balances reducing inflation towards the 2% target and conditions that support employment.

| QTD Return | YTD Return | Price/Value | |

|---|---|---|---|

| Dow Jones Industrial Average | 5.7% | 10.5% | 46,398 |

| S&P 500 | 8.1% | 14.8% | 6,688 |

| S&P 500 Equal-Weighted | 4.8% | 9.9% | 7,693 |

| Bloomberg US 2000 | 11.8% | 8.4% | 1,664 |

| MSCI EAFE | 4.8% | 25.7% | 2,767 |

| MSCI EM (Emerging Markets) | 10.9% | 28.2% | 1,346 |

| Bloomberg US Aggregate | 2.0% | 6.1% | 94 |

| Bloomberg Municipal Bond | 3.0% | 2.6% | 102 |

| Gold (NYM $/ozt) Continuous | 17.1% | 46.7% | $3,873.20 |

| Crude Oil WTI (NYM $/bbl) Continous | -4.2% | -13.0% | $62.37 |

Economic Outlook

Cautiously Optimistic

US economic growth remains positive, driven by the American consumer’s penchant to spend, as well as corporate spending related to the build out of artificial intelligence (AI), among other factors. Remarkably, AI-related capital expenditures contributed more to US economic growth than consumer spending in Q2.

At the same time, a softening labor market and its potentially negative impact on consumer spending, which represents two-thirds of GDP, have implications for the economy. Rising unemployment and weak demand for new hires will force consumers to tighten their budgets.

Currently, the US unemployment rate stands at 4.3%, up from 4% in January 2025 and the post-Covid low of 3.4% reached in 2023. This near-term increase has been driven mainly by younger workers, ages 20 to 24, who have persistent employment challenges and a higher-than-average unemployment rate of approximately 9.2%, increasing from 7.9% at the start of the year.

Finding new jobs has become more difficult and is taking longer for those who have been laid off. Rising labor costs and economic uncertainty regarding tariff policies have made employers hesitant to hire. Additionally, AI implementation has increased job market challenges for recent college graduates and entry-level roles, as employers evaluate how AI can boost productivity without the need to hire additional workers. The hiring rate, an indicator of how actively employers are adding new workers, was 3.8% before the pandemic but currently stands at 3.3%. While wage growth is rising, it is growing at only 4.7%, year-over-year, from August 2024 to August 2025, versus the long-term average of 6.2%. With inflation still high, real wage growth is relatively low.

The administration, however, appears intent on pulling as many levers as possible to strengthen the economy heading into the midterm elections, so fiscal policy should serve as a tailwind to growth. Corporate tax breaks in the One Big Beautiful Bill (OBBB), such as the provision for 100% expensing of capital investments, are intended to spur economic growth. In June, the Tax Foundation estimated that the overall stimulative effect of the OBBB would boost GDP by 0.9% in 2026. Additionally, current US dollar weakness is expected to boost export growth as US goods become cheaper for overseas buyers.

Similarly, legislation has been proposed in Congress to send tariff refund checks of at least $600 to every adult and dependent child, which would support consumer spending if enacted, especially among lower-income Americans. This speaks to the lengths Congress and the administration will go during an election year to garner votes. Unless the labor market deteriorates significantly in the next few months, fiscal stimulus should help forestall any recession for the time being.

Consumer Strength & Retail Sales

The landscape is bifurcated between higher- and lower-income consumers, forming a K-shaped economy where different segments of the economy experience widely different outlooks. Many younger consumers with lower incomes are struggling with student loans and credit card debt. Recent data from a Fed survey estimate that 36% of adults under 40 with at least a four-year college degree have outstanding student loan debt. Student loan delinquencies have risen significantly after the cessation of 5 years of loan forgiveness programs, reflecting the financial stress on this group. In addition, the administration is planning to garnish the wages of borrowers in default. As of April, there were 42.7 million student loan borrowers owing more than $1.6 trillion in student debt, of which only about one-third are current on loan repayments. The rise of “buy now, pay later” financing, which typically targets younger consumers, also indicates spending beyond current means, posing a risk if economic conditions worsen.

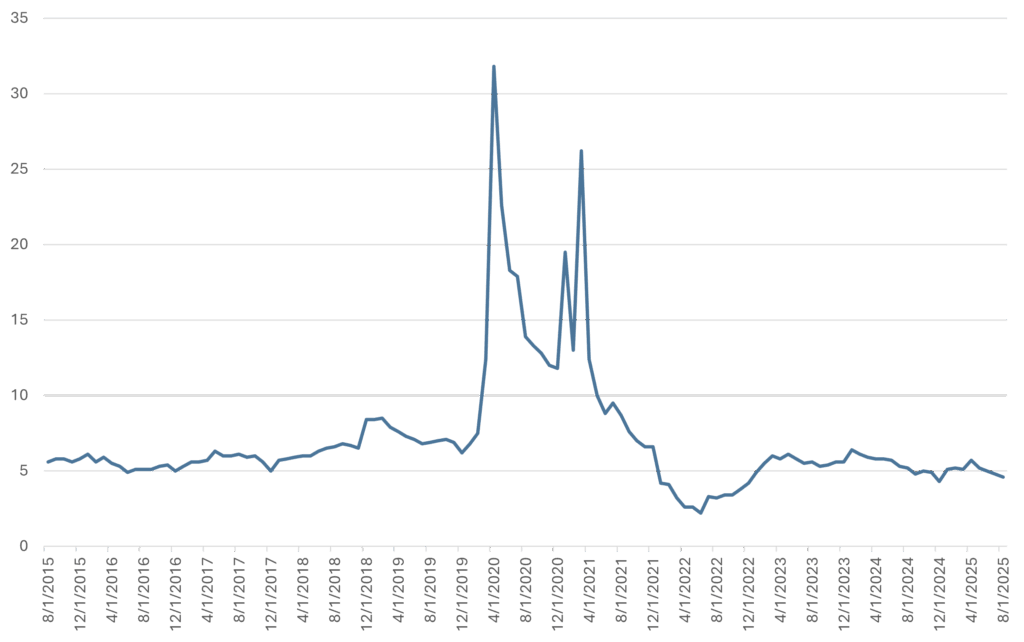

According to a recent Bloomberg report, the average consumer credit score in the US has declined the most in one year (from 2024 to 2025) since the aftermath of the global financial crisis in 2009, marking a second consecutive year-over-year decline. This drop is attributed to higher rates of credit utilization and delinquencies, including student loans. In addition, the US savings rate has dropped to pre-pandemic levels. 5% is not a big cushion in the event of an economic downturn, as constrained consumers may already lack adequate savings to meet their current expenses.

US Personal Savings Rate

Source: U.S. Bureau of Economic Analysis

On the other side of the K-shape are higher-income consumers who have helped drive the economy as beneficiaries of the ‘wealth effect’, resulting from a strong stock market that has supported solid spending by this group. Approximately 50% of all retail sales are made by consumers in the top 10% income bracket. However, should the equity market experience a sharp correction, the broader US economy may face pronounced disruptions as this group of consumers rethinks its spending patterns.

Inflation Remains Murky

Despite the Fed’s continued commitment to a 2% target, inflation has remained persistently higher. Although declining from the annualized rate of 9% reached in June 2022, inflation has plateaued at around 3% for the past year. It remains stubbornly high in certain areas, including food, housing, healthcare, energy, and services, leaving many consumers feeling financially strained.

The administration’s tariff and immigration policies have put upward pressure on inflation. While tariffs themselves may be more of a tax on consumers, which reduces spending on other items, the goal of tariffs to re-shore expensive manufacturing tends to be inflationary. In addition, ongoing global supply chain disruptions due to geopolitical tensions and increased protectionism contribute to volatility in the prices of raw materials and labor costs. Efforts to stack the Federal Open Market Committee (FOMC) with dovish participants in a push for significantly lower rates are fueling inflation concerns.

The Fed Dual Mandate Dilemma

The Fed faces a difficult choice between managing persistent inflation and supporting a labor market that is showing clear signs of cooling. To fight inflation, the Fed raised rates sharply starting in 2022, adopting a “higher for longer” stance. While savers benefit from higher rates on savings accounts and CDs, higher borrowing costs spill over into mortgages, car loans, and commercial loans for businesses looking to expand.

However, last month the Fed approved a quarter-point interest rate cut, the first reduction in nine months, with an expectation for two additional rate cuts later this year. Fed Chairman Jerome Powell and other FOMC officials likely will tread carefully with any rate cuts, aiming to avoid stoking inflation while also responding to the softening job market. The September rate cut appeared to indicate that a softening labor market is the greater concern.

An Independent Fed

The credibility and independence of the Fed in implementing monetary policy are crucial factors for US economic stability and for enabling the US to fund its massive debt at preferential interest rates. Growing political pressures on Fed policy decisions complicate an already challenging US economic environment. The importance of an independent Fed as a global financial institution is a significant consideration. A lack of trust in Fed independence will lead investors to demand higher yields on US Treasuries to compensate for the risk of higher inflation and concerns about long-term economic stability. US government debt has surpassed $37 trillion, increasing by $2.2 trillion in just this calendar year, and now stands at more than 120% of US GDP. These amounts are staggering, driving home the point that debt service will become a significant economic drag, if not a fiscal crisis, if investors demand higher rates.

The Strength of the Dollar

The absence of a clear plan to address debt levels has resulted in a roughly 20% decline in the US dollar over the last 12 months. Other reasons for the decline include uncertainty surrounding tariff policy, rising protectionism, concerns about Fed independence, and foreign investors’ efforts to hedge their exposure to US assets due to geopolitical concerns.

On the positive side, a weaker dollar can serve to make US exports more competitive to overseas buyers. At the same time, imports become more expensive for US consumers and businesses, which can prove to be inflationary. A weaker dollar also reduces the appeal of US assets to global investors, which goes back to the issue of higher financing costs for US debt if foreign demand wanes.

Equity Markets

Mega-Cap Driven

Equity market performance has been driven by a select group of AI-related mega-cap companies, which represents approximately 41% of the S&P 500 market capitalization. This concentration in the US market is similar to other periods when an abundance of optimism was focused on new technology or a particular group of very dominant companies. The following table compares the current conditions to other high points of market concentration and valuation.

| Period | Top 10 Stocks % of Mkt Cap | Top 10 Stocks % of Profits | Driver |

|---|---|---|---|

| Current | 41% | 32% | AI Enthusiasm |

| 1/3/2022 | 33% | 23% | COVID Tech Enthusiasm |

| 3/24/2000 | 28% | 22% | Internet Enthusiasm |

| 1973 | 27% | N/A | Nifty 50 |

It is important to remember that the investment landscape and investor sentiment can change rapidly. Currently, the enthusiasm for the potential of AI is driving the US economy and equity market, reflected in the market leadership of select mega-cap technology and communication services companies. When looking at the top 10 companies by market cap over decades using the following chart, many of the companies remain market leaders, but it should be clear that market leadership can be transitory.

| 1985-90 | 1990-2000 | 2000-10 | 2010-20 | 2020-25 |

|---|---|---|---|---|

| Exxon | Microsoft | Exxon | Apple | NVIDIA |

| GE | GE | Microsoft | Microsoft | Microsoft |

| IBM | Cisco | Walmart | Apple | |

| AT&T | AT&T | Amazon | ||

| Royal Dutch | Walmart | Apple | Amazon | |

| Philip Morris | Intel | Proctor & Gamble | Berkshire Hathaway | Meta |

| American Home Products (Wyeth) | Lucent | Johnson & Johnson | JPMorgan | Broadcom |

| Merck | Exxon | IBM | Visa | Tesla |

| Bristol-Myers | IBM | JPMorgan | Johnson & Johnson | Berkshire Hathaway |

| DuPont | Citigroup | AT&T | Walmart | Oracle |

Elevated Valuations

| S&P 500 | 30 Yr. Average | 3/24/2000 | 10/9/2007 | 1/3/2022 | 9/30/2025 |

|---|---|---|---|---|---|

| P/E NTM | 17.0x | 24.3x | 14.8x | 21.5x | 22.8x |

| EPS Growth LTM | 9% | 21% | 15% | 56% | 11% |

| Revenue Growth LTM | 6% | 13% | 8% | 13% | 5% |

| Dividend Yield LTM | 1.74% | 1.05% | 1.68% | 1.22% | 1.11% |

| 10 Yr Treasury Yield | 3.66% | 6.20% | 4.65% | 1.63% | 4.15% |

The data above show valuations at market peaks over the last 25 years. The chart clearly indicates that current equity valuations remain elevated, primarily fueled by the AI boom. Still, questions remain about the sustainability of the current surge in AI-related capital expenditures. This equity market dependence on massive AI investment creates significant market risks, particularly if AI implementation and commercialization fail to meet lofty expectations for growth and increased productivity.

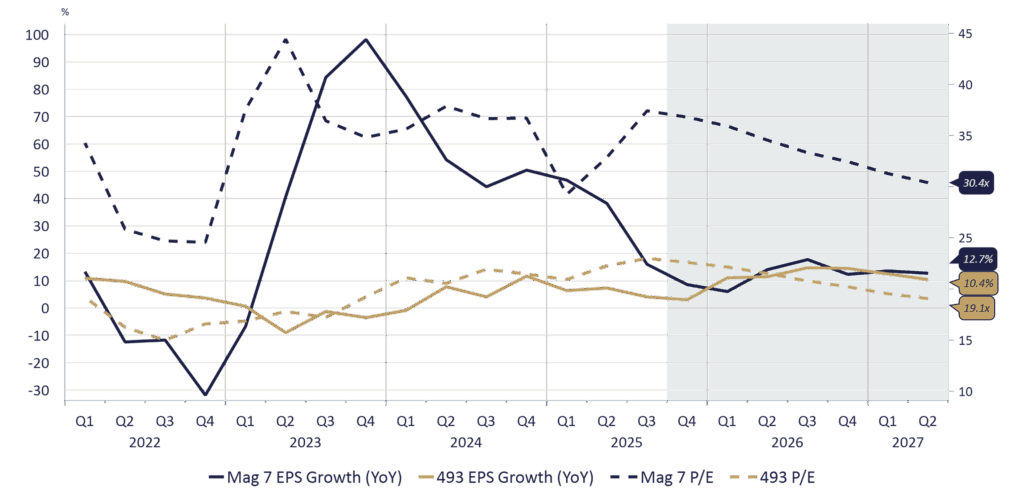

The “Magnificent 7,” which is comprised of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla, saw their valuations peak in mid-2023 and their earnings growth peak 6 months later. While valuations have come down, the “Magnificent 7” still trade at a sizeable premium to the other 493 stocks in the S&P 500. We expect earnings growth for the group of seven to slow next year and be more in line with the earnings growth of the other index constituents, which bodes well for a broadening of market returns.

Magnificent 7 vs. S&P 493

EPS Growth and P/E Ratios

Source: Bloomberg Estimated Headline EPS & Price to Earnings (BM7P, B500XM7P)

Uses Bloomberg 500 instead of S&P 500 for the Benchmark

Data: Quarterly from 2022 Q1 – 2027 Q2

Despite recent enthusiasm about the promises of AI, there are headwinds from inflation, trade policy, debt levels, and labor concerns, as well as risks to Fed independence, that can factor into investor confidence. Given current valuations and concentrations, we remain cautious, while recognizing that US equities remain an important contributor to long-term portfolio growth.

Fixed Income

A Complex Fixed Income Environment

Fixed-income investors also face a nuanced environment, with inflationary pressures likely to keep yields elevated, particularly on longer-maturity bonds, while short-term rates may fall if the Fed continues its rate cuts. Supply and demand shifts driven by global dollar demand and government debt issuance add further complexity. Maintaining vigilance on inflation trends, Fed policy signals, and US debt dynamics will be critical for managing fixed income portfolios.

We expect short-term interest rates to decline modestly, to the 3% area, unless economic conditions sharply deteriorate into recession territory, which would pressure rates lower. Conversely, longer-term rates, including yields on 10-year US Treasuries, are expected to remain near current levels or rise slightly, supported by persistent inflation and the ongoing issuance of longer-maturity debt by the government.

Inflationary pressures contribute to higher yields on longer-term bonds as investors demand compensation for the diminishing purchasing power of future interest payments. Any substantial increase in the supply of Treasury debt, resulting from a widening budget deficit, puts upward pressure on yields as investors demand higher returns for what they perceive as higher risk when buying these securities.

Demand & Issuance Dynamics

At this time, demand for US Treasuries remains sound, with recent Treasury auctions generating strong investor interest. Because US Treasuries have historically been considered a risk-free asset, global demand has generally been quite high.

Several factors, however, could reduce overseas demand for US debt, pushing yields higher and increasing the share of federal spending needed to service the more than $37 trillion in government debt. As of July, Japan, the UK, and China are the largest foreign holders, owning just under 10%, while total foreign ownership, now around 30%, is at a two-decade low.

As we have written, reduced international purchases of US Treasuries could place upward pressure on yields, particularly for longer maturities. Additionally, the size and mix of US debt issuance, balancing short-term versus long-term maturities, could significantly influence near-term bond market dynamics.

Yield Curve Trends

The shape of the yield curve depicts the relationship between bond yields and their maturity lengths, providing insight into investors’ expectations for economic growth, inflation, and future interest rates. Normally, the yield curve slopes upwards from short to long-term maturities. Conversely, an inverted yield curve occurs when short-term rates are higher than long-term rates, generally indicating that investors expect an economic slowdown will be coming.

The yield curve is starting to reflect the September Fed rate cut and the two additional cuts expected later this year, currently sloping upwards as short-term yields have fallen due to the recent rate cut, while long-term yields remain relatively high. The long end of the yield curve is driven more by inflation outlooks and debt issuance patterns and is less impacted by Fed policy changes. Inflationary pressures, as indicated by measures such as the Consumer Price Index (CPI) and the Producer Price Index (PPI), remain above target, supporting the view for steady to slightly higher yields on the long end.

Closing Thoughts

Against this complex economic backdrop, a highly concentrated equity market is vulnerable to correction, and fixed income markets face several challenges that may influence the direction of interest rates. With this in mind, we remain committed to investment objectives informed by long-term goals, near-term cash flow needs, and risk tolerance.

Staying true to an investment objective can help manage various levels of risk while allowing a portfolio to remain invested, but within long-term target allocations. Pairing a focus on asset allocation with sufficient cash reserves for upcoming liquidity needs can help prevent an overreaction to short-term market volatility.

As always, long-term planning amid short-term uncertainty remains essential. We remain focused on what matters most: preserving and growing your wealth through all market cycles.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2025, 1919 Investment Counsel, LLC. MM-00002076