Iran Escalation Jolts Energy Markets as Equity Leadership Continues to Rotate

March 2, 2026

The Iranian Conflict

What Happened

Over the weekend, the United States and Israel initiated coordinated strikes on Iran, marking a significant escalation in a conflict that had been simmering for weeks. The strikes targeted leadership compounds in Tehran, key military infrastructure across multiple cities, Islamic Revolutionary Guard Corps (IRGC) command centers, missile launch facilities, nuclear-related sites, and naval assets. Iranian Supreme Leader Ayatollah Ali Khamenei and numerous senior officials were reported killed, representing a profound disruption to Iran’s command structure.

President Trump stated that U.S. military operations could continue for four to five weeks if necessary but emphasized that the objective is not open-ended conflict. He indicated openness to lifting sanctions should the new Iranian leadership demonstrate pragmatism. Iranian officials, however, have publicly rejected near-term negotiations, despite earlier reports of indirect outreach through Omani mediators.

International reaction has been measured but consequential. Several Western allies signaled support for U.S. action, while Gulf states condemned Iranian strikes on their territory and expressed concern about broader regional destabilization. Lebanon and Hezbollah have indicated a desire to avoid direct involvement, though rhetoric remains elevated.

Market Response

Oil prices reached seven-month highs on Friday ahead of the strikes in anticipation of an escalation. Following the attacks, crude oil extended gains amid concerns about potential disruption to supply through the Strait of Hormuz, a critical chokepoint for global energy flows. Estimates suggest that roughly one-fifth of global LNG exports transit the region, raising the possibility of material energy market disruption if conflict broadens.

Energy prices rose across the complex, including natural gas, as safe-haven flows intensified. The U.S. dollar, gold, the Japanese yen, and the Swiss franc all attracted inflows. Global equities have traded lower in early reaction, though the decline has thus far been measured.

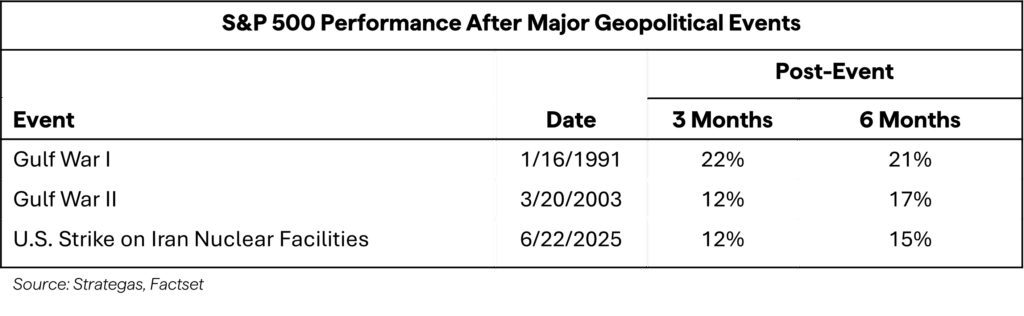

Notably, market reaction has been restrained relative to the scale of the event. Given recent geopolitical episodes, investors have grown more accustomed to episodic shocks that ultimately prove contained. At present, markets appear to be pricing a risk-off phase rather than a structural economic break.

Our Expectations

The facts surrounding the conflict will evolve and change over time. In the near term, a defensive tone is likely to persist. Energy volatility and headline sensitivity will remain elevated as investors assess the scope and duration of military operations.

History suggests that markets often absorb geopolitical shocks unless they materially alter global growth or financial conditions. If the conflict proves contained and energy supply remains intact, the economic impact may be limited to a temporary inflationary impulse. However, a prolonged disruption, particularly one that meaningfully impairs oil flows, would present a more serious risk. Sustained energy price spikes could weigh on global GDP growth and reintroduce inflationary pressures at an inopportune time for central banks.

Over the longer term, the foundational drivers of markets – economic growth, corporate profit expansion, and gradual disinflation – remain intact. Geopolitical volatility can influence timing and sentiment, but structural fundamentals ultimately dominate multi-year outcomes.

Financial Markets

Against this geopolitical backdrop, U.S. equity markets finished the week mixed. AI disruption concerns and hotter-than-expected inflation data earlier in the week weighed on sentiment, while rotation beneath the surface accelerated. Notably, the equal-weighted S&P 500 outperformed the market-cap-weighted S&P 500, continuing a year-to-date trend of improving breadth. This divergence reflects reduced reliance on mega-cap leadership and a gradual redistribution of returns across sectors and market capitalizations.

| Index | Prior Week | Year-to-Date | 1-Year |

|---|---|---|---|

| S&P 500 | -0.42% | 0.68% | 18.86% |

| S&P 500 Equal Weighted | 0.44% | 7.06% | 17.27% |

| Dow Jones Industrial Avg. | -1.31% | 2.12% | 13.27% |

| NASDAQ Composite | -0.94% | -2.39% | 23.02% |

| Small Cap S&P 600 | -1.46% | 7.90% | 18.96% |

| MSCI EAFE | 1.24% | 10.11% | 35.31% |

| MSCI Emerging Markets | 2.83% | 14.86% | 50.83% |

February proved volatile. The S&P 500 posted a monthly loss amid concerns that the AI trade may be exhibiting bubble-like characteristics and that the technology itself could prove disruptive to existing business models. Treasury markets, meanwhile, delivered strong monthly performance, underscoring the continued role of fixed income as a stabilizer despite ongoing fiscal concerns.

Early-week weakness was partly attributed to a research note outlining a hypothetical “Global Intelligence Crisis,” suggesting that rapid AI-driven productivity gains could disrupt employment across delivery, payments, and software industries. Software shares initially came under pressure but rebounded after commentary indicated that emerging AI platforms may partner with, rather than displace, incumbent enterprise software providers.

Nvidia once again delivered a significant earnings beat and raised forward guidance, reinforcing its leadership position in AI infrastructure. Revenue growth remained robust, and free cash flow generation is extraordinary. Yet the stock declined following the report, reflecting elevated expectations and growing investor scrutiny regarding the sustainability of AI capital spending. Concerns persist about the financial durability of large AI infrastructure customers and the broader economic implications of automation-driven labor displacement.

This pattern of strong fundamentals met with muted or adverse price reaction signals a market increasingly sensitive to valuation and positioning rather than simply headline growth.

Economics

Recent economic data delivered a nuanced message. Consumer confidence rebounded modestly, though improvement was concentrated in expectations rather than present conditions. The labor market differential – respondents saying jobs are plentiful versus those saying jobs are hard to get – continues to trend weaker, suggesting a gradual softening in employment conditions.

Weekly jobless claims remain historically contained, reinforcing the “low-hire, low-fire” characterization of the labor market. While hiring has cooled, layoffs have not accelerated meaningfully.

Inflation, however, surprised to the upside at the producer level. January core PPI posted its most substantial monthly increase in nearly four years, signaling renewed upstream pricing pressures. Services inflation accelerated, raising the possibility that some cost pressures could filter into consumer prices or the Fed’s preferred PCE measure.

Taken together, the economy appears to be slowing modestly but not contracting. Profitability and capital spending remain supportive. However, persistent upstream inflation complicates the Federal Reserve’s policy path.

Policy

Trade policy remains fluid. Following the Supreme Court ruling limiting tariff authority under IEEPA, the administration announced replacement tariffs under alternative statutory authorities, including Section 122 and Section 232. While legal clarity improved on one front, trade uncertainty persists. The European Union has pushed back against cumulative tariff levels, and China has indicated it may adjust its countermeasures. Legal challenges to tariff implementation are ongoing, and refund mechanisms remain unresolved, with at least one major U.S. corporation filing suit seeking reimbursement.

In his State of the Union address, President Trump emphasized economic accomplishments and outlined proposals including retirement savings incentives, housing market interventions, and healthcare subsidy reforms. While details remain sparse, the broader fiscal stance appears oriented toward sustaining growth into the midterm cycle.

Geopolitical developments in Iran now add another layer of complexity. Energy-driven inflation shocks could delay Federal Reserve easing, if sustained.

Conclusion

This week encapsulated the current market environment: a tug-of-war between resilient fundamentals and escalating headline risks. Geopolitical escalation in the Middle East has introduced near-term volatility and renewed energy price uncertainty. Inflation data remain uneven, complicating the Federal Reserve’s policy trajectory. Meanwhile, equity leadership continues to rotate as investors reassess valuations, AI sustainability, and economic durability.

Encouragingly, economic growth remains positive, corporate earnings are expanding, and market breadth is improving. International markets have shown relative resilience, and fixed income has continued to provide ballast amid equity volatility.

The most significant risk in the near term lies in policy, both geopolitical and trade-related. Should energy disruptions prove temporary and inflation remain contained, the underlying expansion can continue. If escalation broadens materially, growth and inflation dynamics could shift more meaningfully.

In this environment, disciplined diversification, quality exposure, and a long-term perspective remain essential. Volatility is rising, but the broader economic foundation has not fractured. Markets may fluctuate in response to headlines, yet fundamentals continue to provide a constructive, if increasingly selective, backdrop for patient investors.

I. Front End Disclosure

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all clients and each client should consider their ability to invest for the long term, especially during periods of downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown.

All investments carry a degree of risk and there is no guarantee that investment objectives will be achieved.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

There is no guarantee that employees named herein will remain employed by 1919 for the duration of any investment advisory services arrangement.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2026, 1919 Investment Counsel, LLC. MM-00002319

II. Investment Analysis

The information shown herein is for illustrative purposes. 1919 may consider additional factors not listed here or consider some, but not all, of the factors listed here as appropriate for the strategy’s objectives.

There is no guarantee that desired objectives will be achieved. 1919 has a reasonable belief that any third party information used for investment analyses purposes is reliable but does not represent to the complete accuracy of such information by any third party.

III. Portfolio Composition

For illustrative purposes. There is no guarantee that the portfolio composition for the strategy discussed herein will be comparable to the portfolio shown here.