Investing in Fixed Income: Let’s Be Careful Out There

With the Fed cutting interest rates to zero and pledging to leave them there for an extended period of time, we believe that fixed income investors must be mindful in their investing strategy. In this report, we take a deep dive into the current fixed income landscape, and our response to the low rate environment. We review the Fed’s new policy framework, the role of fixed income in portfolios, and the implications for investing in fixed income in an extended period of very low rates.

We readily admit that we are dating ourselves by referencing a 1980s TV cop drama in the title of this report. For those too young to remember the hit Stephen Bochco show “Hill Street Blues,” the plotline followed a single police precinct in an unnamed city. In each episode, Sgt. Phil Esterhaus gathered the cops and detectives for a daily roll call and discussion of cases. Following the briefing, the Sergeant always concluded the meeting with exactly the same phrase: “Let’s be careful out there.” Right now, this phrase comes to mind as we take a look at the current environment in fixed income.

The Math is the Math

For clients focused on generating income, the math is clear. A bond bought at a 2% yield will return close to 2% for the life of the bond if held to maturity: no more and no less, assuming that it does not default. Therefore, returns for fixed income will, by definition, be lower in the future given the current starting point for yields, unless the Fed embraces a negative interest rate policy, which we do not expect.

In light of this, we believe clients should view their fixed income allocation as a way to preserve wealth, while understanding that the income generated by a portfolio of high-quality investment grade corporate and muni bonds is very likely to be lower going forward. We also note that high yield and emerging market bond returns have historically been positively correlated with equity returns, so we believe that a reach for yield beyond Treasuries and investment grade corporate and municipal bonds is mostly adding more risk, without meaningfully diversifying the return profile.

- U.S. Treasuries are the safest investment, and used to offer both portfolio stability and income

- In light of the Fed’s revised monetary policy framework, we expect to be in a world of very low Treasury yields for an extended period of time, meaning that the income portion from Treasuries is no longer attractive

- We are focused on investment grade corporate and municipal bonds of intermediate maturities, in order to gain some incremental income while not adding material risk

- We are generally cautious in reaching for yield beyond U.S. Treasuries and investment grade bonds, as these asset classes have historically shown a positive correlation with equities

- Corporate “fallen angels,” which are companies originally rated investment grade that are now in high yield, may make sense for clients willing to take on incremental risk

- An allocation to fixed income can still act as a stabilizer to client portfolios

- While risks exist in the current low interest rate environment, we plan to stay the course by maintaining fixed income allocations and credit discipline

The takeaway message is that fixed income can still provide stability for investors, but the income stream generated by fixed income will be reduced going forward, so we are adopting a cautious approach for client fixed income allocations.

Record Lows for U.S. Treasury Yields

It’s worth starting our in-depth discussion with a review of how we got here. Beginning in March, the Fed’s response to the pandemic has been dramatic. The Fed cut rates in two emergency meetings, and the target range for the Fed funds rate is now zero to 0.25%, compared to 2.25% to 2.50% as recently as July 2019 (and 1.25% to 1.5% at year-end 2019). The 10-year U.S. Treasury yield dipped below 1% for the first time in early 2020, and sits at just 0.76% as of this writing. The 30-year U.S. Treasury yield is also near record lows, falling from 2.39% of as year-end 2019 to 1.55% as of this writing.

Source: Bloomberg. As of October 2, 2020.

The Fed also revived many financial crisis era programs to support market functioning, as well as created new ones. Perhaps even more important than the Fed’s real-time response to the crisis is its adoption of a new monetary policy framework, introduced in August 2020 at its annual Jackson Hole (this year, held virtually) retreat.

The Fed’s Twist of FAIT

At this retreat, the Fed formally introduced a new monetary policy regime known as “Flexible Average Inflation Targeting,” or FAIT. This announcement marked the most significant shift in monetary policy since 2012, when the Fed first adopted a formal 2% inflation target. With the adoption of FAIT, the Fed amended its language on both inflation and employment. In regards to maximum employment, the FOMC emphasized that maximum employment is a broad-based and inclusive goal and that policy decisions will be informed by an assessment of “shortfalls” in maximum employment, whereas previously the policy was driven by “deviations” from its maximum level. On price stability, the FOMC adjusted its strategy for achieving its longer-run inflation goal of 2% by noting that “following periods when inflation has been running persistently below 2%, appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time.”

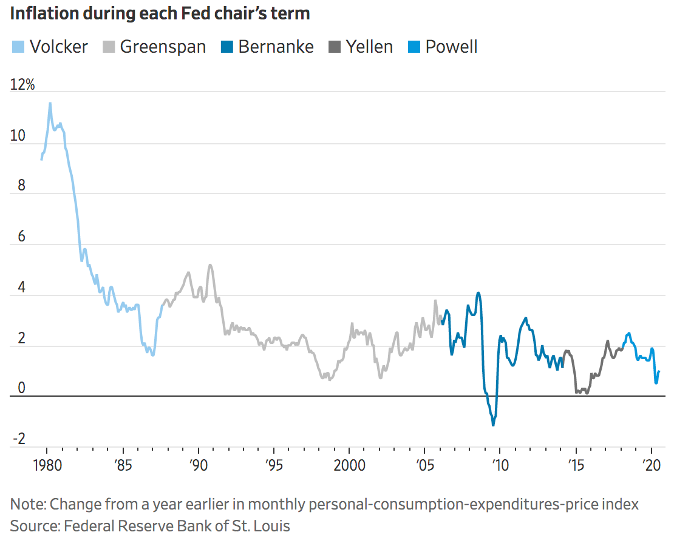

The new FAIT regime shifts the Fed’s 2% inflation bogey from a “point in time” measure to an “average” metric, with a clear bias to holding interest rates lower for longer, even if inflation overshoots 2% for a period of time after a period of low inflation. As shown in the chart below, inflation has been in a steady downward shift for decades.

Source: Makintosh, James. “A Flexible Fed Means Higher Inflation.” The Wall Street Journal, August 30, 2020. https://www.wsj.com/articles/a-flexible-fed-means-higher-inflation-11598796001

Further, the pandemic acts as a disinflationary shock on the U.S. economy, hampering economic activity and driving higher unemployment. Fed Chair Powell has deliberately declined to specify over what period of time the average inflation will be measured, and the starting point for measuring the average matters greatly. As well, the Fed has declined to specify by how much over 2% it will tolerate inflation before beginning to tighten monetary policy. In our view, the Fed has been deliberately vague about these parameters, in order to preserve some optionality in its future policy moves. Nevertheless, the intent of the policy is clear: The Fed will remain on hold for an extended period of time.

As seen in the chart below, the twin conditions of inflation over 2% and unemployment rate below 4.1% have occurred infrequently since 1960 (when monthly inflation statistics are available). Even before the pandemic, the Fed has been unsuccessful in driving core inflation above its 2% goal. Now, the Fed’s 2% inflation goal may be even harder to reach as the pandemic is a disinflationary shock. Furthermore, with the new FAIT framework, the Fed has pledged to keep rates low for some time even after inflation rises above 2%.

Source: Authers, John. “Powell’s Great War Tactics Catch Markets off Guard.” September 17, 2020, Bloomberg Opinion.

We acknowledge that the Fed directly controls only the short-end of the Treasury curve, so there is a possibility that long-end rates could rise, leading to a steeper yield curve. However, we have not yet seen any material pressure on the long-end of the curve, and we believe that the Fed would likely engage in another “Operation Twist” or embrace a policy of targeted yield caps, if long-end rates rose materially enough to lead to tighter financial conditions. Overall, we believe that clients must be prepared for an extended period of historically low rates across the Treasury yield curve, even as we continue to invest a portion of client assets in fixed income.

Focus on Intermediate Corporates and Longer Duration Munis

While of course U.S. Treasuries remain the safest asset class, earning less than 1% on a 10Y Treasury bond does not generate an attractive income stream for investors. We note as well that given the low level rates across the yield curve, Treasuries have a negative “real” yield, below even the modest level of current inflation. Given our expectations for an extended period of low rates, we are adopting a tactical response to invest in investment grade corporate and muni bonds in order to generate incremental yield. In corporate bonds, we believe that investment grade corporate bonds of intermediate duration make the most sense.

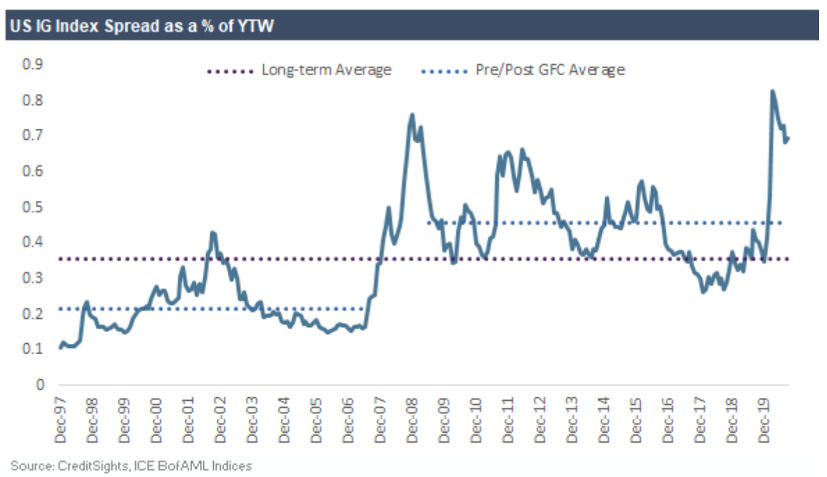

As a reminder, the yield on a corporate bond can be split into two constituent parts: the yield on a Treasury of the same duration, and a “spread” over the benchmark yield. Right now, given the very low rates on U.S. Treasuries, the contribution of spread to the total yield is high on a historical basis, as seen in the chart below.

Source: Khasin, Jeff. US IG Chart of the Day: US IG as a % of YTW. September 24, 2020. CreditSights, https://www.creditsights.com/articles/343780

In essence, this means that investors are getting a much higher contribution from the credit risk of owning a corporate bond within the total yield than is typical historically, and with Treasury yields so very low, investors are being compensated more than ever to take on corporate credit risk.

Are BBBs the new AAAs?

Within the corporate bond universe, we have focused recent purchases on BBB-rated securities in the 7-10 year, or intermediate, part of the curve. We note that historical default rates for BBB-rated corporate bonds are relatively low. Since 1920, the median annual default rate for Baa-rated securities according to Moody’s is 0%. This means that in most years, there are no defaults for BBB-rated issuers. The average default rate for BBBs, which takes into account periods of stress, is only 0.26%. We emphasize that these default statistics reflect all BBB-rated securities, whereas we typically avoid the lowest category of BBBs, which are BBB- or Baa3 ratings.

Finally, we note that the Fed has implemented two corporate credit facilities as a “backstop” program for all issuers that were rated investment grade as of March 22, 2020, at the beginning of the pandemic. These facilities are currently in place through the end of 2020, and we do not rule out that they may be extended in order to ensure smooth functioning of the corporate credit markets and access to capital. The Fed remains supportive of corporate credit, and investment-grade rated companies should continue to be able to issue bonds given the Fed backstop in place. Meanwhile, the average yield on a 7-10Y BBB bonds is still around 2%, as seen below.

Source: Khasin, Jeff. US IG Chart of the Day: YTW by Rating, Tenor. October 1, 2020. https://www.creditsights.com/articles/344569

For buy and hold investors, owning solid BBB-rated bonds in the 7 to 10 year maturity still makes sense. A good example of what we are buying now is a recently issued 10Y bond from Johnson Controls (JCI). Johnson Controls offers air systems, building management, HVAC, fire safety, and security systems worldwide. The company has a $30 billion market capitalization and solid investment grade ratings of Baa2 by Moody’s and BBB+ by Standard & Poor’s. We recently participated in JCI’s first Green bond, buying a 10Y bond with a 1.75% coupon at new issue.

Municipal Bonds: Comfortable with High Quality Duration

We also are selectively adding municipal bonds in the 10+ years of the curve, using both traditional and taxable municipal bonds. Munis remain attractive as they have even lower default rates than corporate bonds, especially for the strongest issuers. We acknowledge there are headwinds in state and local governments due to the impacts of the pandemic, but overall we expect government authorities to manage through. Most municipalities must balance their budget annually, and while cuts to local services are never welcomed, these actions are positive for muni bondholders. As well, owning munis should be even more beneficial if personal tax rates rise going forward, which is expected in case of a Democratic win in the Presidential election.

We continue to focus on highly rated municipal issuers, and avoid high yield or non-rated munis. For example, we recently bought a new issue general obligation (GO) from the state of Pennsylvania due in 2034, with ratings of Aa3 at Moody’s and A+ at S&P. We bought the bond at a 1.55% yield-to-call in 2030, which is a taxable equivalent yield of roughly 2.5% (using an assumed Federal tax rate of 37%). If the bond is not called in 2030, the taxable equivalent yield is over 3.5% to its 2034 maturity.

High Yield Also Means Higher Risk

Of course, the next natural extension for investors is to consider going “down in quality” to purchase high yield securities to gain incremental income. As a reminder, investment grade (IG) bonds are rated BBB-/Baa3 and higher, while high yield (HY) is anything rated BB+/Ba1 and lower.

As the yield for investment grade securities has declined, there has been a “reach for yield” into high yield securities. For example, in August 2020, Ball Corp. issued a new bond with the lowest coupon on record for a high yield new issue of 5+ years maturity at just 2.875%. The average yield on securities rated in the highest quality tier of high yield, Ba1, is approximately 4.1%. On an aggregate basis, the yield for the HY index is now well below 6%, compared to its long-term average of nearly 9%.

Despite the lower yields for HY, we note that high yield default rates are now above long-term averages and anticipated to rise further over the next year or so. Based on Moody’s statistics, the trailing 12-month U.S. HY default rate was 8.7% at the end of August compared to a pre-pandemic level of 4.5%. Looking forward, Moody’s baseline forecast is for the U.S. high yield default rate to finish 2020 at 11.0% and peak at 11.4% in the first quarter of 2021.

No matter what the actual high yield default rate ultimately turns out to be, the absolute figure is less important than the overall picture: high yield default rates are multiples of investment grade default rates, while the incremental yield is not. Given this dynamic, we advocate a cautious approach to high yield.

Fallen Angels May Outperform

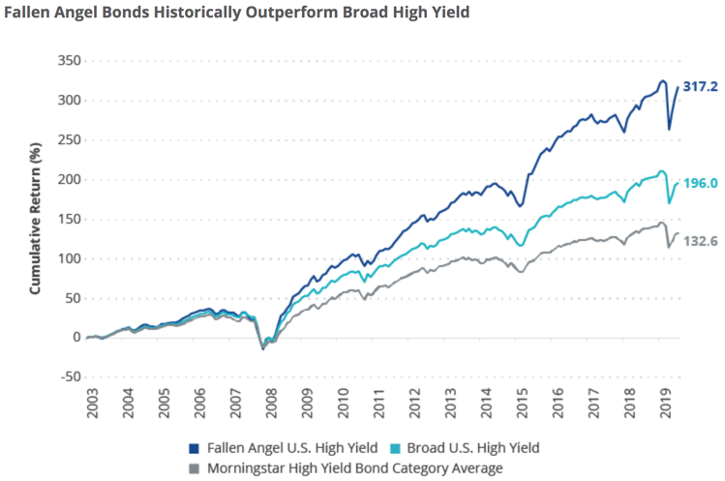

Nevertheless, for those investors willing to take on incremental credit risk for more yield, we believe that the class of high yield known as “fallen angels” may make the most sense. Fallen angels are defined as securities that were once rated in investment grade, but have since been downgraded into high yield due to credit challenges. Fallen angels historically perform better than original issue high yield, as show below.

Source: VanEck, https://www.vaneck.com/insights/blogs/income-investing/fallen-angel-bonds-qa-what-to-watch/?country=US&audience=fa

*Although at 1919 Investment Counsel we do not recommend individual bond allocations to high yield or fallen angels, we have a Third Party Committee process to review outside funds. A group of senior analysts and portfolio managers reviews “best in class” funds and ETFs from external managers. Our process includes initial due diligence on fund management companies, as well as ongoing surveillance of the fund’s performance, management team, portfolio guidelines, positioning, tracking error, and external ratings.

There are several reasons for this dynamic. By definition, fallen angels were once stronger investment grade companies, which typically have better business profile, larger market capitalization, and lower leverage than bonds which were “original issue” high yield.

As well, rating agencies usually downgrade companies by no more than 1-2 notches, and therefore fallen angels tend to be in the upper echelons of the high yield universe (BB category). A research report by BNY Mellon found that because the Fallen Angel Index was comprised of BB-rated issuers, they have experienced a lower default rate over time, stating that “Since the index’s inception in 2005, fallen angels have experienced a lower average default rate of 0.39% versus 0.99% for the high yield index.” (Source: Hayes, Manuel and Benson, Paul. Fallen Angels: The Last Free Lunch, BNY Mellon Investment Management, July 2019).

Because many institutional investors with specific investment grade mandates are limited in their holdings of high yield securities, there can be technical selling pressure when a bond crosses over to HY. This often drives bond valuations to overshoot on the down side before regaining their footing. As well, some of the fallen angels are able to regain their investment grade rating over time, providing a technical boost on the way back up the ratings ladder. For individual investors, we believe a well-diversified investment makes the most sense to gain exposure to Fallen Angels, rather than attempt specific security selection for this class of high yield. For investors willing to take on this incremental credit risk, there are several ETFs that track the Bloomberg Barclays Fallen Angel Index, allowing investors to gain diversified exposure to this specialized asset class.

Although at 1919 Investment Counsel we do not recommend individual bond allocations to high yield or fallen angels, we have a Third Party Committee process to reviews outside funds. A group of senior analysts and portfolio managers reviews “best in class” funds and ETFs from external managers. Our process includes initial due diligence on fund management companies, as well as ongoing surveillance of the fund’s performance, portfolio guidelines, positioning, tracking error, and external ratings.

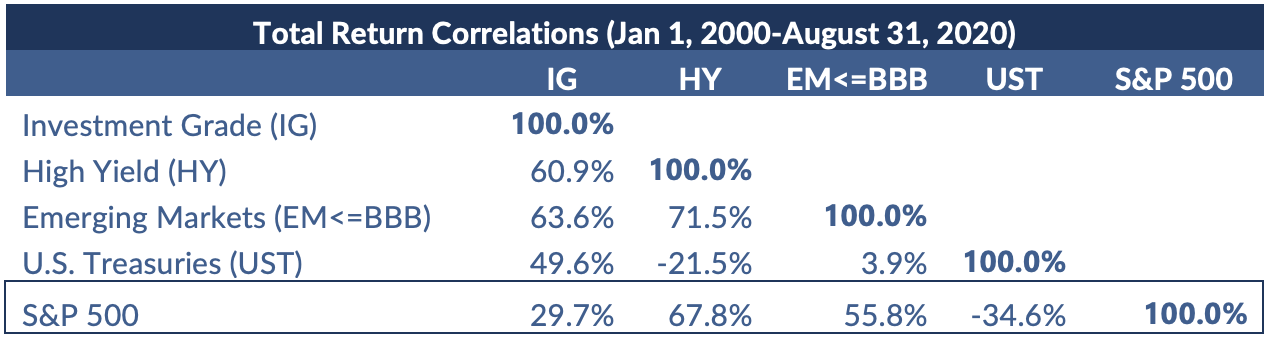

Consider the Correlations

As investors consider whether it is appropriate to add incremental yield to their fixed income portfolios, we want to emphasize that there is no free lunch. Aside from higher risk of default and higher volatility, the riskier classes of fixed income such as high yield, emerging markets, and preferred stock have historically been positively correlated with equity returns. Before adding more yield to a fixed income portfolio, investor should recognize and understand these correlations. So although treasuries and investment grade corporates and muni bonds can post losses in the case of higher interest rates or higher credit spreads, they have typically acted as an important stabilizer for balanced portfolios.

Source: CreditSights

The table above shows the weekly total return correlations between various asset classes, including U.S. Treasuries (UST), investment grade corporate bonds (IG), high yield corporate bonds (HY), emerging markets bonds (EM) and the S&P 500 since 2000. Focusing on the bottom row of the chart, the takeaway is that U.S. Treasuries have been negatively correlated with the S&P 500, while investment grade bonds have a relatively low positive correlation. In contrast, high yield and emerging markets bond returns have much higher positive correlations with the equity markets. We believe this shows that a balanced portfolio with exposure to Treasuries and investment grade fixed income should act as a counterbalance to the volatility of equities, while also providing positive returns.

As shown on the Total Return Correlations chart on the previous page, U.S. Treasuries have historically been one of the most effective hedges for equities, with Treasury returns inversely correlated with returns on the S&P 500. Now, however, the low level of Treasury yields means that their effectiveness as a hedge against equities may not hold as well going forward. With the yield on the 10Y Treasury under 70 bps, there is simply not much room for further price appreciation, unless we believe that rates will go negative. The Fed has been clear that it does not think negative interest rates are right for the U.S., so we consider this outcome to be unlikely. Therefore, we believe that investment grade corporate and municipal bonds make the most sense as a source of stability in a balanced portfolio going forward.

In Closing: Bonds Still Make Sense, but Let’s Be Careful Out There

As we wrap up our discussion of investing in fixed income in an era of very low interest rates, we think it is helpful to remember the primary purpose of a fixed income allocation in a diversified portfolio. In our view, the fixed income portion of a portfolio is primarily for greater stability of overall returns than can be achieved from a portfolio allocated only to equities. Although interest rates are likely to remain very low for an extended period of time, we believe that Treasuries and investment grade corporate bonds should continue to provide this stability for client portfolios given that they show relatively low historical correlation with equity returns. So while we acknowledge the risks presented by the current low interest rate environment, we are maintaining fixed income allocations for most clients.

We are currently adding intermediate and long duration in high quality corporate and muni bonds. We have maintained our credit discipline, with a focus on investment grade bonds, although in some cases recommending an allocation to higher-quality high yield bonds such as fallen angels for clients’ with a higher risk tolerance. We continue to view fixed income as a crucial stabilizer for balanced portfolios, even if yields are at historic lows. Overall, we consider ourselves to be like cops walking the beat, charged with protecting our clients’ portfolios while always remembering the Hill Street Sergeant’s mantra: “Hey, let’s be careful out there.”

BAYLOR LANCASTER-SAMUEL

Vice President, Credit Analyst

Baylor is a Vice President at 1919 Investment Counsel, LLC. Her primary responsibility is to conduct research on all taxable credit for the fixed income strategies. In addition to publishing commentaries on her coverage universe, Baylor is a member of the Fixed Income Committee and Third Party Committee. Baylor has an extensive background in credit research, with prior experience in institutional, family office, independent research, and rating agency roles. Baylor is a member of 100 Women in Finance and the Fixed Income Analysts Society, Inc. (FIASI).

Baylor earned a B.A. from New York University, College of Arts and Science. She earned an M.B.A in Finance from New York University, Stern School of Business. She also earned an M.A. from the University of Miami.

Email address: blsamuel@1919ic.com