2024 Tax Update

Tax Changes Could Be on the Horizon –

Managing Tax Risks in 2024’s Uncertain Environment

A Brief Summary

Many of the tax benefits enacted by the Tax Cuts and Jobs Act are scheduled to disappear on January 1, 2026. Anyone seeking to take advantage of the current tax rules should start speaking to their financial advisor, attorney, or accountant sooner rather than later. The upcoming federal elections present a pivotal moment from a tax standpoint as it will set the tone for what’s about to come next. As we saw 12 years ago with the “fiscal cliff” and the possible automatic reduction of the federal estate tax exemption from $5 million to $1 million, lawyers will be overwhelmed by clients seeking to make large gifts and execute other strategies before these favorable rules possibly sunset without renewal. While the rules could be extended, made permanent or otherwise modified, it is anyone’s guess what will happen. We think the prudent move is to plan now for what may come rather than scramble at the last minute. In the meantime, the current rules remain in effect. For 2024, various favorable tax adjustments have been implemented that are worth considering as you plan for 2024 and what is coming next.

The Current Tax Landscape

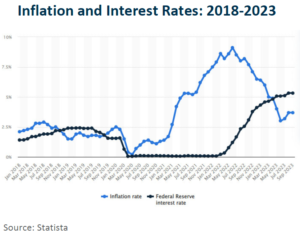

Each year, the IRS announces new income tax rate brackets and inflation adjustments. As we know, in 2022 and 2023 inflation crept higher and interest rates rose steadily to levels unseen in over 15 years. Both higher inflation and interest rates have resulted in greater than normal adjustments to various elements that affect federal taxes, such as tax brackets and the standard deduction, as well as the estate and gift tax exemption, all of which are keyed to inflation. In addition, higher interest rates affect certain estate planning strategies.

In this paper, we review some of the highlights of the most recent tax adjustments for 2024. We also consider the current tax landscape in light of the sunset provisions of the Tax Cuts and Jobs Act of 2017 (TCJA) and the potential effect of the 2024 election cycle on your taxes.

For wealthier taxpayers, the TCJA included several tax bonuses (such as a doubling of the estate and gift tax exemption) and a few detractors (such as the $10,000 cap on the state and local tax deduction). But the Act came with a big catch; many of its provisions expire on December 31, 2025. There is one more catch that occurs this year–the 2024 election. The election could result in a political shift that could trigger tax changes sooner than planned, i.e. before the sunset date. Moreover, the presidential election is not the only political race to watch. Many congressional seats are up for grabs too.

A shift in power in the U.S. House and/or Senate will affect what new Federal tax rules can be passed and how quickly. Once the 2024 election results are known, we will start to understand what could happen in 2025 and 2026 in terms of potential tax changes.

A wide range of tax changes could be enacted, some of which could be effective immediately, prospectively, or retroactively.1

Things to watch out for include:

- Increases of ordinary income tax rates

- Increases of long-term capital gains tax rates

- Expansion of what’s taxable by the Net Investment Income Tax (i.e., the 3.8% surtax)

- Curtailment of stepped-up basis rules

- Reduction of estate and gift tax exemptions

- Taxes on unrealized capital gains

The possibilities are endless!

Soon after taking office, President Biden offered an ambitious and controversial tax plan that included many new tax proposals such as severely limiting stepped-up basis and forcing a deemed realization of capital gains for gifts of appreciated property, and creating new “super brackets.” Senators Bernie Sanders and Elizabeth Warren proposed a federal wealth tax, which was derided by many as unconstitutional.2 What the divided Congress ended up passing was far less sweeping than what was proposed. But those novel ideas were up for serious discussion and caused a lot of angst. We are confident, though, that through Election Day (November 5, 2024) no major tax changes will be enacted that could upset the basic assumptions we are operating with today. After that, it’s anyone’s guess.

Based on past experience, we anticipate that individuals and their advisors will scramble at the last minute to take advantage of current tax rules before they change. The mad dash could start as soon as the next day (November 6, 2024), or even earlier. So, we advise that anyone seeking to take advantage of the current tax rules should do so sooner rather than later. That means talking to your advisors, especially your attorney or accountant as soon as possible.

Against that background, we discuss the current tax situation with tax brackets, interest rates and inflation adjustments and provide some advice on what you might want to consider doing this year.

Anyone seeking to take advantage of the current tax rules

should do so sooner rather than later.

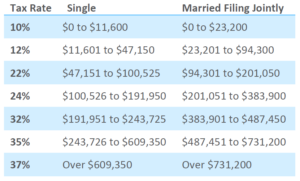

2024 Tax Rate Brackets Adjusted Upwards

In November 2023, the IRS announced the following new tax rate brackets for 2024 based on recent inflation data. They represent a favorable bump up of about 5.4% over 2023 brackets.

New Tax Rate Brackets for 2024 (Individuals)

These brackets are worth noting for anyone considering converting their traditional IRA to a Roth IRA. A conversion is generally a taxable event. It is often desirable to remain within a certain bracket when doing a Roth conversion; for example the 24% bracket which reaches taxable income as high as $383,900 for married couples.

Long-Term Capital Gains Tax Rates for 2024 (Individuals)

Long-term capital gains rates remain favorable in 2024. These rates also apply to “qualified dividends”. We believe these rates should remain in force through the end of 2025.

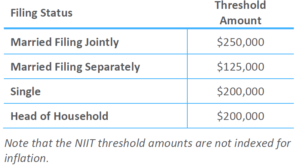

The Zinger: The Net Investment Income Tax

The 3.8% Net Investment Income Tax (NIIT) applies to investment income of individuals, estates and trusts having income above a certain threshold. In general, “investment income” includes interest, dividends, capital gains, rental and royalty income, non-qualified annuities, income from businesses involved in trading of financial instruments or commodities and businesses that are passive activities. The Biden Administration unsuccessfully proposed expanding the type of income subject to the NIIT to include pass-through business income from partnerships and increasing the tax rate to 5% for earnings over $400,000. An expansion of the NIIT in 2025 or 2026 is possible.

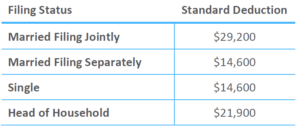

A Larger Standard Deduction: Today Fewer People Itemize

For 2024, the standard deduction increases for all taxpayers. The new figures are:

The relatively higher standard deduction was enacted as part of the TCJA. The standard deduction along with the $10,000 limitation on the deduction for State and Local Taxes (SALT) has greatly reduced the number of taxpayers who itemize their deductions. In 2019, the Tax Foundation reported that prior to the enactment of the TCJA, 31.1% of taxpayers’ itemized deductions, whereas, under current law, only 13.7% do so. The TCJA also further limited the deduction on home mortgage interest among other things. These rules will sunset at the end of 2025 unless they are extended or made permanent.

Estates and Trusts Pay Taxes at the Highest Rates

Estates and irrevocable non-grantor trusts are subject to compressed tax brackets. In 2024, they will owe federal tax at the rate of 37% on taxable income over $15,200. The 20% capital gains rate is applicable for estates and trusts with taxable income over $15,450. This rate also applies to qualified dividends. Estates and trusts are subject to the 3.8% NIIT if they have adjusted gross income over $15,450 in 2024.

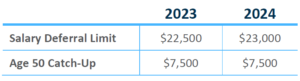

New Thresholds for Retirement Accounts

Inflation also affects the contribution limits to retirement accounts. Last year, the IRS announced that the amount individuals can contribute to their employer retirement plans (401(k), 403(b), and 457(b) plans) increases in 2024 as follows:

The limit for contributions to traditional and Roth IRAs increased to $7,000 in 2024, up from $6,500 in 2023. The catch‑up contribution limit for individuals who are age 50 and over was adjusted under the SECURE 2.0 Act of 2022 to allow an annual cost‑of‑living adjustment but remains $1,000 for 2024. The catch-up contribution limit for employees age 50 and over who participate in employer plans remains $7,500 for 2024.

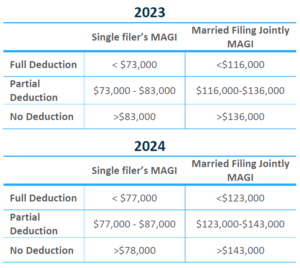

Traditional IRA Deductibility Enhanced in 2024

For 2024, the IRS increased the modified adjusted gross income (MAGI) phase-out ranges for the deductibility of contributions to traditional IRAs. They also adjusted the income thresholds for contributing to Roth IRAs.

Contributions to a traditional IRA are not deductible if you are covered by a 401(k) or similar plan at work. Contributions to a Roth IRA are never deductible. In addition, earned income is required to make a contribution to an IRA, thus making it hard for young people who are not yet working to contribute to an IRA.

SEP IRAs and Solo 401(k)s: Higher Limits for the Self-employed

If you are self-employed, your business may contribute on your behalf to a SEP IRA. SEPs have a much higher contribution limit than regular IRAs. For 2024, the contribution limit is the lesser of 25% of your self-employment income or $69,000 (but there are no catch-up provisions for those age 50 and up). However, if your company has employees, all eligible employees must participate in the SEP retirement plan. Contributions to a SEP IRA for the prior year can be made as late as October 15 if you file for an extension of time to file your tax return.

A solo 401(k) is another option if you are self-employed. The limits are similar to SEPs, but there are a few nuanced differences between the two types of plans.

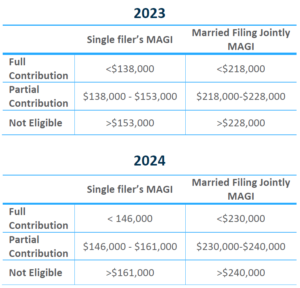

Roth IRA Eligibility Expanded in 2024

Similarly, the income limits for eligibility to make a contribution to a Roth IRA were bumped up in 2024 as follows:

Note that employees may make contributions to a Roth 401(k) regardless of their salary level up to the cap of $23,000 and may contribute an additional $7,500 if age 50 and older.

Backdoor Roth Contributions Remain Viable

A technique known as a “backdoor Roth” contribution allows someone whose income exceeds the eligibility threshold to make a contribution to a Roth IRA by way of a traditional IRA. It works like this: First, you make a nondeductible contribution to a traditional IRA and then convert it to a Roth. This “backdoor” technique has been widely reported in the popular press as a tax loophole. Like all loopholes, it comes with a few special rules. There is a 5-year bar on post-conversion withdrawals for people under age 59 ½, otherwise the entire withdrawal is subject to a 10% surtax. Further, a 10% surtax applies to earnings withdrawn within 5 years of the conversion even if you’re over age 59 ½. In addition, the IRS requires that all of your traditional IRAs to be taken into account on a pro-rata basis when determining the taxable amount at the time of conversion. Because IRA contribution limits are so low, the tax is not significant and may even be zero. The rules are a bit complex, though, and require additional tax reporting and documentation.

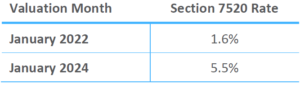

Interest Rates and Estate Planning (Pros and Cons)

Higher interest rates affect certain estate planning techniques, such as Grantor Retained Annuity Trusts (GRATs), Charitable Remainder Trusts (CRTs), Charitable Lead Annuity Trusts (CLATs), and Qualified Personal Residence Trusts (QPRTs). Since January of 2002, the IRS’s Section 7520 rate (aka the “hurdle rate”) has steadily increased. Compare the 7520 rate today and that of two years ago.

A prime objective of GRATs and CLATs is to pass on wealth tax-efficiently to the next generation. Higher interest rates make those strategies less attractive since a higher hurdle rate means that the trust’s investments must work that much harder to achieve a tax-efficient wealth transfer—i.e., to have something left over after the trusts term expires. Further, the annuity that must be paid out over the life of the trust must be higher in order to “zero-out” the taxable gift. The higher annuity also has the effect of reducing what’s available at the end.3 On the other hand, higher interest rates make QPRTs more attractive since the donor’s retained interest in the residence is deemed to be of greater value, thus making the amount of the taxable gift smaller.

Similarly, for CRTs, the donor would be entitled to a larger income tax deduction in a higher interest rate environment, making the CRT more attractive when rates are higher. Moreover, it’s easier to satisfy special tax rules that apply to CRTs when rates are higher.4

All of these planning strategies are basically “cookie-cutter” in the sense that they conform to tried-and-true formulas. However, they require careful planning and legal work and, almost more importantly, must be properly administered so that the desired tax effects are respected by the IRS.

Annual Gift Exclusion Climbs to $18,000

The annual gift exclusion increases to $18,000 for calendar year 2024, up from $17,000 in 2023. The annual exclusion allows donors to make gifts to anyone up to $18,000 per year without having to use any of their lifetime exemption. A married couple can give twice this amount (or $36,000). Further, by using a technique known as “gift-splitting,” one spouse can be the source of the funds. However, a federal gift tax return is required to elect gift-splitting.

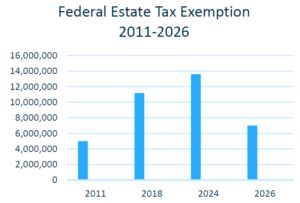

Lifetime Estate and Gift Tax Exemptions: Use It or Lose It

Under the TCJA, the federal lifetime estate and gift tax exemption was doubled over its then current level of $5,000,000 as adjusted for inflation. The TCJA provides that the doubling will expire on December 31, 2025. Unless Congress acts otherwise, the exemption will revert to half of its current level. Last November, the IRS announced that the exemption amount for 2024 is $13,610,000, which is up from $12,920,000 in 2023. This large exemption (the highest ever) presents a tremendous opportunity for those who can afford to make a gift of that amount (or twice that if married) and, thus, reduce their estate’s potential future tax burden. However, due to the way the exemption works, only those who can afford to use the entire exemption before December 31, 2025, can take meaningful advantage of it. A gift of less than $5 million will not make any difference provided the exemption doesn’t fall below that level.

SLATs – A Creative Way to Use Your Exemption

One of the common techniques estate planners use to take advantage of the current rules is a Spousal Lifetime Access Trust (or “SLAT”). A SLAT is an irrevocable trust designed to absorb (and thus lock in) one’s estate and gift tax exemption at current levels. What makes a SLAT attractive is that your spouse can be a current beneficiary of the trust. Although funding a SLAT is an irrevocable gift, the trustee will have the power to distribute assets to your spouse as long as he or she is alive and still married to you (or after your death). The trust also can continue on for the next generation and be protected from generation-skipping taxes. In addition, two spouses may create a SLAT for each other as long as certain basic rules are followed (trusts can’t be reciprocal, e.g.). However, caution should be exercised in such cases. Some planners advise that a minimum of 6 months should separate the creation of SLATs created by spouses, which further highlights the need to act sooner rather than later. In addition, you can set up a version of this type of plan for yourself in certain states that allow asset protection trusts, such as Delaware, South Dakota and Nevada.5

Planning for What’s Next

As we said the many of the tax changes enacted in the TCJA will automatically expire at the end of 2025 and the law will revert to pre-2018 rules unless Congress does something. The last time we had a situation like this was at the end of 2012 when we faced the “fiscal cliff.” In 2012, the federal estate tax exemption was $5.12 million but was scheduled to revert automatically to $1 million on January 1, 2013. A deal between the White House and Congress was ultimately reached at the last minute. The American Taxpayer Relief Act of 2012 was signed into law on January 2, 2013, thereby preventing drastic automatic changes to estate and gift tax exemptions and rates.

However, today, the world is different and perhaps more complex than it was in 2012–there is no telling what could happen after the 2024 election cycle or as 2025 winds down. Given all that, we advise that anyone who is able to make large gifts to use up their federal estate and gift tax exemption should consider doing so this year.

The last time we had a situation like this was at the end of 2012

when we faced the “fiscal cliff.”

Perhaps the only thing that is certain is that nothing is certain. Election Day (November 5, 2024) will be a pivotal date. Will it bring more of the same or something different? And, if something different is coming, what will it be?

At 1919 Investment Counsel, we continue to monitor Congress as well as the IRS and Supreme Court. In the meantime, we hope you will be in touch with your advisors, especially your estate planning attorney, before the year goes by. We look forward to catching up with you about these and other important topics that affect your estate plan.

Read pdf here.

1 The Supreme Court has held that tax laws may be enacted retroactively. So, changes in tax laws could take effect as soon as

January 1, 2025, even if passed later in the year. Moreover, the lame duck session that follows the 2024 election is something of a wild card.

2 Note that constitutional issues don’t exist at the state level. A number of states have started to entertain imposing a wealth tax—California and Vermont are two such examples.

3 See Planning in a Low-Interest Rate Environment https://1919ic.com/wp-content/uploads/2020/11/Planning-in-a-Low-Interest-Rate-Environment-2.pdf

4 For CRTs, the value of the remainder going to charity must meet a minimum threshold, which is 10% of the initial fair market value of the property placed in the trust. Other technical rules also apply.

5 See 2020: The Year of the SLAT (June 3, 2020) https://1919ic.com/library/2020-the-year-of-the-slat/