Investment Review & Outlook – July 2024

Key Takeaways

- While the US economy has remained resilient in 2024 due to a strong labor market and moderating inflation, there are several indications that growth is beginning to slow, although not enough to bring about a recession.

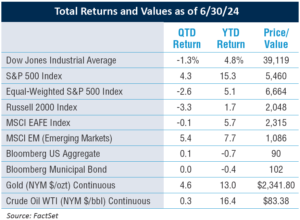

- Despite rich valuations and concentrated performance, the equity market reached new highs propelled by select AI-related stocks and the expectation that interest rates will decline.

- Encouraging data regarding inflation came in just as the quarter ended, which should give the Federal Reserve room to initiate a cut in interest rates, possibly as early as September.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

Economic Review

The consumer-dependent US economy remains strong, bolstered by a healthy labor market that drives higher personal income growth. It has been two years since the Fed started to increase rates, a policy change that traditionally slows an economy. However, during this period, consumers continued to work and spend, and employment levels did not deteriorate.

Under the surface, there are several signs that a slowdown has begun, and we expect it will continue over the next year due to the economic lag of tight monetary policy. Retail sales have softened, and the manufacturing sector, as measured by the PMI (Purchasing Managers’ Index), fell below the key level of 50, indicating a contraction.

In addition, wage growth has moderated, as has the demand for labor. Unemployment rose from a half-century low of 3.4% a year ago to 4% more recently, while the job-vacancy rate has declined, from a high of 7.4% in March 2022 to 4.8% in April, 2024. The Fed believes that unemployment could begin to move up more significantly if the job-vacancy rate falls below 4.5%.

Against this backdrop of slowing growth there is still no clear signal that a recession is imminent. Economic growth and employment are holding up reasonably well as inflation moderates.

Inflation’s Cumulative Impact

The rate of inflation, as measured by the Consumer Price Index, was 3.3% for the 12 months ending May 31, which is still well above the Fed’s target of 2%. However, the quarter-end release of the personal consumption expenditures index (PCE), the Fed’s preferred inflation gauge, increased only by 2.6%, the smallest increase in 3 years. This is down sharply from the peak of 7.1% reached in 2022.

“We’ll need to see more good data to bolster our confidence that

inflation is moving sustainably toward 2%.”

– Fed Chairman Jerome Powell.

Confidence in the Fed and its ability and willingness to rein in inflation continues to be critical for US standing in the global economy and for investors’ willingness to purchase Treasuries without compensation for the risk of a volatile inflation rate. Recent data shows Fed policy to be working.

While inflation may be moderating, its cumulative effects continue to be felt by consumers, particularly those living from paycheck to paycheck. Inflation has a much bigger impact on them and they have no offsetting benefit from rising asset values. Meanwhile, annual wage growth remains positive, underscoring the labor market’s resilience. Across many industries, employers still face challenges in finding workers to fill open positions.

Rising Delinquencies

US consumers are markedly bifurcated between higher-income earners enjoying the wealth effect of increased home and investment values and lower-income earners who, buffeted by inflation and with dwindling savings, are challenged to pay for necessities. Many consumers are changing their spending patterns, spending less on discretionary items, and moving away from brand name items for consumer staples.

Against this backdrop, credit card delinquencies are rising. Unpaid credit card debt overdue by over 90 days rose to 10.7%, the highest level in over a decade, as more consumers struggle to pay their bills. This does not bode well, especially for lower-income consumers, if unemployment spikes as the economy slows, tightening finances further.

A Word About Risk

The depth and breadth of geopolitical risks today are significant and concerning. From the conflicts in the Middle East and Ukraine and the tensions surrounding China and Taiwan, there are many rapidly-changing global dynamics to consider, all of which have the potential to roil markets. On top of this, the upcoming US election and its outcome only adds to the uncertainty.

Equity Market Highlights

A Story of Concentration

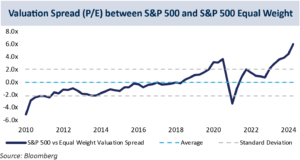

Equity investors disregarded high valuations, sticky inflation keeping rates high, and dashed hopes for six rates cuts, driving the S&P 500 higher by 15.3% year-to-date and 4.3% for the second quarter. The story of the equity markets in 2024 continues to be one of remarkable concentration, and the still-significant valuation gap between a handful of technology and communication services stocks and the broader equity market. While we did experience a brief period when the market performance broadened beyond just these few companies, it since has reverted, propelled by the enthusiasm surrounding almost anything AI-related. The significant divergence between this concentrated group and the rest of the market continues. For example, the Magnificent Seven stocks represent 32% of the value of the S&P 500 Index but have contributed 59% of the 2024 return, half of which was from NVIDIA.

Compare this to the equal-weighted S&P 500 Index which removes the impact of size and values all 500 index constituents equally. This index gives quite a different view of the equity market, up only 5.1%, further illustrating the divergence in performance between the select few stocks and the broader market.

AI-Related Equity Market Growth

The equity market rally began in late October of 2023, when this current valuation expansion was triggered by dovish comments from the Fed and fueled by the growing enthusiasm surrounding AI. Since then, while corporate profits are expected to grow by 11% in 2024 and 14.4% in 2025, the S&P 500 Index is up 33% over the roughly eight-month period. Investor optimism, fed by hopes for lower interest rates and an eventual lift to economic productivity from AI, has resulted in significant valuation expansion without a commensurate increase in expected profits. Positive sentiment shifts are common in the market’s history, but it is important to remember that optimism can erode quite quickly as well, and ultimately earnings and cash flows drive long-term market returns.

The question regarding AI-related stocks is whether their revenue growth and wide profit margins are sustainable at these levels. The outperformance of NVIDIA, the poster child for AI enthusiasm, has been supported by a rapid increase in the company’s earnings, sales, profit margins, and its notable competitive advantage as a leader in building chips to train large language models.

Comparisons to the Tech Bubble of 2000

The strength in fundamentals of these AI-related companies is markedly different from many of the companies with ballooning stock prices in the tech bubble of 2000, wherein the strength of underlying cash flows and earnings did not exist. Equity market valuations, while well above long-term averages, are not quite as elevated as they were during the tech bubble of 2000.

Currently, the market-cap-weighted S&P 500 Index is trading at about 21x 1-year forward earnings. During the tech bubble of 2000 the index traded closer to 25x 1-year forward earnings.

However, it is important to note that while the potential long-term growth opportunities for the use of AI are significant, investors may be overly caught up in AI fervor in the short run. We are in the early stages of rapid AI development and adoption; many companies have not yet determined how to apply or monetize the evolving revolutionary technology. This can lead to near term disappointments as quarter-to-quarter growth will vary and not always meet lofty expectations.

At the same time, equity market volatility has been subdued for some time, suggesting a perceived low-risk environment where investors are somewhat complacent. Notably, it has been almost 16 months since the market had a 2% decline in one day.

Fixed Income Highlights

The Fed Holds Firm

Investors with expectations in early 2024 for a substantial number of rate cuts have been disappointed. At its most-recent meeting in June, the data-driven Fed kept the fed-funds rate unchanged, awaiting confirmation that inflation is edging closer to the 2% target. This is the longest period ever between the onset of rate tightening and the first rate cut. The Fed has held the fed-funds rate steady at 5.25% – 5.50% for almost a year now, and it has been over 2 years since its aggressive monetary policy tightening began.

The Fed’s forecast for interest rates now implies only one quarter-point (25 basis points) cut by the end of 2024, a significant shift from earlier this year, when in March the Fed forecast a total of three quarter-point cuts. Also, the Fed now forecasts that inflation will end the year higher than initially predicted, and Chairman Jerome Powell remarked that it is a “balancing act” to lower inflation, manage the “very strong” labor market, and keep the economy growing.

Longest Inverted Yield Curve

The US yield curve has been inverted since July 2022, the longest inversion in history. This means that the yields on long-term bonds are lower than those offered on short-term bonds. Typically an inverted yield curve has preceded a recession, but this time the likelihood of a recession is still in question. Excess consumer savings boosted by pandemic-related stimulus has buffered consumers to some extent from tighter credit conditions, and a strong and growing economy with low unemployment has belied the certainty of recession.

Rate Cuts on the Horizon

As we factor in the slowing of the economy, gradually-falling inflation and the fact that monetary policy works with a time lag, we think the Fed has enough room to start cutting rates, possibly as early as the September meeting. As we have written previously, we do not foresee a scenario where rates will come down as quickly or sharply as investors had been expecting in late 2023. Of course, as we saw during the pandemic, there always exists the possibility of sharp rate cuts resulting from the Fed having to provide significant liquidity to the economy due to events that are out of its control: a geopolitical surprise, terrorism, a financial blow-up of some kind, or something not previously on the radar screen.

Higher for Longer

From the 3.95% level at the beginning of 2024, 10-year Treasury yields ended the quarter at 4.36%, rising as a response to stubbornly high inflation data, the same reason the Fed has remained on the sidelines. However, during the most recent quarter, the yield rose to a high of 4.70% on April 25, reflecting investor concern about strong economic data keeping tight monetary policy in place for longer. As inflation expectations have moderated, so have yields.

Overseas central banks have started to cut rates, which makes US yields more attractive globally and increases demand for US Treasuries. However, rates at the longer end of the yield curve will not decline meaningfully for the foreseeable future despite favorable interest rate differentials. Heavy Treasury supply to fund fiscal deficits will continue to keep interest rates elevated, particularly with the economy already at full employment and little labor slack. Neither Presidential candidate is running on a platform of austerity, so deficits will continue, creating a challenge for the Fed.

Pockets of softness in the economy should cap any meaningful rise in yields, which already reside at the highest levels we have seen in years, providing opportunities for attractive income generation in both the taxable and tax-free bond markets. Additionally, after more than a decade, bond investors now benefit from positive real rates (adjusted for inflation), which preserve purchasing power and provide a return above inflation. The 10-year Treasury currently offers a real rate of 2% more than expected inflation, which is a level not reached since 2007 according to data from the Federal Reserve Bank of Cleveland.

Closing Thoughts

A gradually-slowing economy should provide the Fed room to begin easing monetary policy with a rate cut. Equity investors are likely to continue to chase the beneficiaries of rapid AI development. However, a market dominated by a very slim number of companies, combined with rich valuations and recent levels of low volatility, leaves us expecting a pullback in the near future. Meanwhile, fixed income investors should continue to enjoy today’s higher income opportunities.

As always, we stand ready to help you move forward and consider meeting your investment goals our greatest priority.

Read pdf here.

All information herein is as of June 30, 2024 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2024, 1919 Investment Counsel, LLC. MM-00001161