Weekly Market Insights 07.29.24

A Dramatic Week

Financial Markets

Investors had much to ponder this past week. Developments in the presidential race, earnings announcements, and notable economic releases topped the list. While President Biden’s withdrawal from the race added another wrinkle in an already eventful election season, politics was not a major factor in the markets last week. The economic releases, which we will write about shortly, went about as well as could be expected. The fly in the ointment was disappointing earnings announcements.

While fixed income markets reacted favorably to last week’s news, equity markets were mixed and volatile. The Dow gained 0.75%, the S&P 500 dropped 0.83%, while the NASDAQ fell 2.08%. Some standout observations—for the week, small-caps outperformed large-caps, the equal-weighted S&P 500 outperformed the cap-weighted. We also saw an interesting reversal in sector performance, with Utilities and Health Care stocks leading the pack and Communication Services and Information Technology stocks lagging. Given last week’s moves, observers should not be surprised to hear more talk of a rotation.

Economics

Second quarter GDP was announced this past week. Although it was a report that should have pleased investors, it was overshadowed by several disappointing earnings announcements from some of the S&P 500’s largest companies, Alphabet and Tesla. Real (ex-inflation) GDP grew at a 2.8% quarter-over-quarter annual rate, handily beating forecasts and marking an acceleration from the first quarter’s pace. Overall, the report was quite positive, as were others released last week. Consumer spending rose more than expected, and since consumption makes up around 70% of the U.S economy, that number should be a confidence builder. Perhaps one of the most important data points for future prosperity is business investment in production-enhancing equipment. Encouragingly, non-residential investment grew at a 5.2% quarter-over-quarter annual rate, while investment in equipment grew 11.6%. Also of note, inflation cooled, as measured by the Fed’s preferred inflation gauge, the PCE Deflator Index.

Recent economic releases should provide both investors and consumers with confidence that the economy is healthy. These releases should also build the confidence of the Fed Open Market Committee (FOMC) that inflation is moving sustainably down towards their 2% target.

With the important provision that economic indicators can be revised or turn unexpectedly, it appears as if the economy is going the Fed’s way.

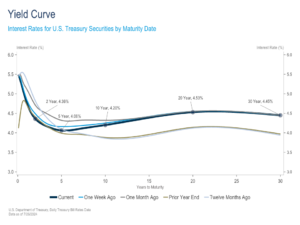

Yield Curve Update

Yields have been on a downward trajectory in recent weeks, as cooler inflation data has fueled optimism that the Fed will move forward with its first rate cut at their September meeting. Over the course of the week, the 2-year Treasury yield fell 13 basis points, while the 10-year yield fell 5. Relative to one month ago, the declines have been more significant, with 2-year and 10-year yields declining 37 basis points and 20 basis points, respectively. As a result of these movements, the yield curve inversion lessened to 19 basis points, down from 36 at the end of June.

At the Fed’s June meeting, Chairman Powell stressed that the Committee wants to gain further confidence that inflation is moving sustainably down towards their 2% target, and members are relying on the economic data for that confirmation. Since then, we have received several encouraging inflation reports, most notably a lower than expected Consumer Price Index (CPI) reading in early July. Friday’s in line PCE Deflator inflation report confirmed that reading, and the market is now pricing in a September Fed Funds rate cut with 100% certainty.

Fed members will meet again this week, where they will certainly shed more light on their policy plans. Of course, we will keep readers abreast of what develops.

Read pdf here.