Investment Review & Outlook – January 2025

Key Takeaways

- The consumer-driven US economy has remained resilient, despite inflation above the Federal Reserve’s target of 2%, driven by low unemployment, modest wage growth, and an uptick in consumer confidence during much of 2024. Attention now turns to the economic impact of the incoming Trump administration, key priorities being higher tariffs, lower taxes, and stricter immigration policies.

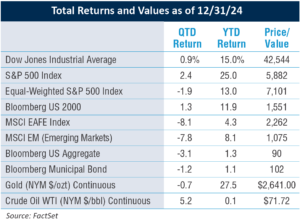

. - In the equity market, 2024 was the second consecutive year of 20+% returns, a milestone not seen since the dot-com boom of the late 1990s, driven by ongoing excitement surrounding artificial intelligence (AI), as was the case in 2023. Investors also cheered a quick resolution to the US presidential election along with the belief that the outcome signifies a more friendly regulatory environment and an increase in merger and acquisition activity. While corporate fundamentals look solid for 2025, rich stock valuations do not seem to be discounting any policy missteps or a resurgence of inflation.

. - Following two years of tight monetary policy, the Fed initiated the first of three rate cuts in September. However, hawkish comments by Fed Chair Powell in December indicated that future rate cuts may not be as deep as investors had hoped. During the quarter, the bond market began pricing in the inflationary effects of Trump administration policies and a higher-for-longer rate environment, as evidenced by an increase in the yield of the 10-year US Treasury. Risks to the bond market in 2025 include sticky inflation and expanding budget deficits.

.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

Economic Outlook

The US economy remains resilient heading into 2025, supported by robust consumer spending and a resurgence in business confidence, and driven by onshoring initiatives that aim to strengthen domestic production capabilities. At the same time, it is just weeks until a new Trump administration takes office, bringing with it a policy agenda that potentially can disrupt the US economy in various ways.

The labor market remains the cornerstone of US economic resilience, characterized by low unemployment rates and an ongoing expectation of job growth, particularly in the service sector. A strong labor market and wage growth drive consumer spending, which is critical as it constitutes approximately two-thirds of the US gross domestic product (GDP).

Depending on the extent to which the new administration is able to carry out its plan to deport millions of immigrants, the consequences will be felt throughout the economy. According to recent US census data, non-US citizens make up about 10% of the workforce. As seen in the following employment chart, most of the growth in the labor force since the pandemic is attributed to foreign-born workers. In a tight labor market, as is the case now, reducing the number of available workers for each job contributes to higher wages, which reduces profitability and can be inflationary. Sectors of the economy that may be particularly hard hit are agriculture, construction, and leisure/hospitality, some of which show job openings still exceeding the number of people unemployed.

For example, nearly half of all agriculture workers in the US are immigrants. Mass deportation in this industry most likely will result in a shortage of available workers leading to higher food costs for everyone. While there seems to be bipartisan agreement that the US needs a stronger and more coherent immigration policy, the upcoming crackdown comes at a time of an aging US demographic, which may not bode well for labor market resilience and consequently economic growth in the coming years.

A Bifurcated Consumer

Consumer spending strength has been notable over the past year, driven by several factors, including a strong labor market. Robust equity markets and rising home prices have elevated the consumption of higher-income households. This segment’s spending on luxury items and experiences contributes positively to the travel, dining, and high-end retail sectors. Their financial stability allows them to maintain or increase their spending despite broader economic challenges.

However, there is a significant gap between the stability of lower-income and higher-income households. The cumulative effects of inflation impact lower-income consumers more as price increases cut into spending on necessities such as food and energy. The wealth effect of rising home values and equity portfolios does not materially bolster this demographic.

These consumers increasingly prioritize essential goods and services at budget-friendly retailers like Walmart. Rising prices constrain their spending power, which affects their overall consumption and economic contribution to GDP growth. While the overall economy may show resilience, if lower-income consumers reduce spending significantly, it could dampen economic growth, as their consumption is vital for many businesses, particularly in the retail and service sectors.

A second focus of the incoming administration is the implementation of sweeping tariffs across a range of goods imported into the US from many countries. A president has broad latitude to modify tariffs without congressional approval, including for reasons of threats to national security, a war, an emergency, or to combat unfair trade practices by a foreign country. It is fair to expect tariffs to be implemented or expanded on day one. Trump has argued that tariffs will earn billions in revenue for the US government, but tariffs are paid for by the importer of a good who typically passes on the cost to the end consumer. There is some ability for the original producer to identify efficiencies that may reduce the impact on the ultimate consumer, but this is unlikely to offset the proposed tariffs completely. Currently, tariffs make up only about 2% of US government receipts.

Depending on the magnitude and breadth, tariffs can be inflationary. It will take time for manufacturers to ramp up enough domestic production of goods that will be subject to tariffs to satisfying consumer demand, so prices tend to rise in the meantime.

Tariff policy can result in concessions by countries reliant on trade with the US. It also can result in retaliation by other countries through reciprocal tariffs, currency wars, and the potential cost of US jobs. Because the COVID-19 pandemic happened not long after tariffs were imposed during the first Trump administration, it has been challenging to quantify the negative impact on GDP and consumer price inflation.

Tariff policy can result in concessions by countries reliant on trade with the US. It also can result in retaliation by other countries through reciprocal tariffs, currency wars, and the potential cost of US jobs. Because the COVID-19 pandemic happened not long after tariffs were imposed during the first Trump administration, it has been challenging to quantify the negative impact on GDP and consumer price inflation.

Trump was elected with a promise to tackle post-pandemic inflation, a key issue for voters. The challenge for the administration is that his signature campaign initiatives, tax cuts, tariffs, and mass deportation will likely fuel inflation, not mitigate it.

The Strength Of The US Dollar

The strength of the US dollar is another significant theme in 2025. The US dollar is the world’s reserve currency, dominating transactions in the global economy. Its strength makes it relatively inexpensive for US consumers to buy goods from other countries or travel outside of the US. However, it also means that the goods exported by US companies are more expensive to buyers in different countries. Further, higher inflation with rising interest rates diminishes the benefits of a higher dollar to American consumers.

The Trump administration wants a weaker dollar to make US exports more competitive in the world economy. However, the policy initiatives we have written about are likelier to strengthen the dollar than weaken it. Sweeping tariffs and tax cuts will likely keep monetary policy tighter than in other countries. Higher US interest rates attract investors, which makes the dollar stronger.

Equity Markets

A Favorable Market Environment

Strong economic indicators, positive corporate earnings, and stable interest rates contributed to a favorable equity market environment, generating consecutive 20+% returns over the past two years. Expectations for earnings growth remain positive, with a broadening beyond select mega-cap stocks, indicating a healthy corporate profit outlook. Two additional rate cuts in 2025 are expected, and if implemented, they also should support stocks if the economy continues to expand.

Strong economic indicators, positive corporate earnings, and stable interest rates contributed to a favorable equity market environment, generating consecutive 20+% returns over the past two years. Expectations for earnings growth remain positive, with a broadening beyond select mega-cap stocks, indicating a healthy corporate profit outlook. Two additional rate cuts in 2025 are expected, and if implemented, they also should support stocks if the economy continues to expand.

Small- and mid-cap stocks, in particular, offer attractive valuations but do better in a lower interest rate environment. This segment may present opportunities for investors seeking growth and diversification away from reliance solely on the larger, more established companies, for which the strong US dollar can be a headwind. International stocks remain relatively inexpensive, although corporate and country growth fundamentals appear weaker than in the US.

The Risk Of High Valuations

There is a common investor refrain that “political gridlock is good” as it reduces the possibility of legislative disruption to markets. A Republican sweep, although narrow, combined with the political uncertainty of the new administration at a time when valuations are high, leaves the equity market vulnerable to increased volatility.

The S&P 500 is trading at approximately 22 times the next twelve months (NTM) earnings, significantly above its 15-year average of 16.6 times. This elevated valuation suggests that the equity market is not pricing in much risk. While valuation is a poor indicator of short-term performance, as high valuations can persist for some time, inflated valuations are associated with lower-than-average longer-horizon returns.

High valuations can increase the vulnerability of equities to potentially higher bond yields, as we saw in 2022 when investors reallocated capital from equities to bonds. If the new administration’s policies drive inflation and interest rates higher, investors will likely do so again. Investors have favored equities for years, given that historically low levels of interest rates, in place since the Great Financial Crisis, have not offered much competition for investor capital. Should bond yields rise higher than the market expects, that will present a challenging backdrop for stocks.

AI Implementation And Proof Of Profitability

In addition, following two years of exuberance surrounding AI that drove much of the equity market momentum in 2024, the focus will shift toward the actual returns generated by this capital investment. Investors will search for tangible returns on investment and the means for companies across various sectors, beyond the major tech companies, to leverage AI into revenue effectively.

Fixed Income

After a few years of tight monetary policy to rein in inflation, the Fed finally took its foot off the brake and cut rates three times in the last few months of the year, for a total reduction of 100 basis points (1.0%). Nevertheless, the future path of longer-term interest rates, influenced by inflation, economic growth, and Fed policy appears likely to remain higher. Not only is inflation still above the target rate, but also the extension of tax cuts, expanded tariffs, and a new deportation policy have the potential to push inflation higher. This concern was evident in the rise of the benchmark 10-year US Treasury yield that ended the year higher by almost a full point more than when the Fed started to cut rates.

Inflation Dynamics And Fed Policy

As the following chart shows, the rate of inflation, currently 2.7%, remains stuck above the Fed’s 2% target. The Fed’s monetary policy approach remains highly data-dependent, with indications that the long-term neutral rate, historically about 2.75%, may settle in at a higher level than anticipated.

A “neutral” interest rate is considered to be neither restrictive nor stimulative. Current projections call for only two 25 bps (0.25%) Fed funds rate cuts in 2025.

In 2025, the Fed’s response to further inflationary pressures will be gradual as it monitors the impact of the incoming administration’s policy changes that are designed to be dramatic. Meanwhile, as Powell’s comments following the December Fed meeting indicated, the Fed reduced its projected cuts for 2025 from four to two based on stronger economic forecasts than anticipated. While this is good news for inflation hawks, stock investors have been counting on lower short-term rates to fuel gains.

“The slower pace of cuts for next year reflects the

higher inflation readings we’ve had this year.”

-Fed Chairman Powell

Another variable to consider is the potential politicization of the Federal Reserve and its impact on interest rates, which would create market volatility. If the Fed’s actions are perceived as clearly influenced by political pressures, investor confidence would be critically eroded, and equity valuations would follow.

Credit Strength And Increased Issuance

Solid credit fundamentals exist in the fixed-income market, with investment-grade corporate spreads over Treasuries remaining exceptionally tight, indicating investors do not see any significant risks or possible recession in the near term. Treasury yields are anticipated to stay above 4%, with intermediate to long-term corporate yields above 5%. Intermediate-maturity bonds offer some inflation protection and a reasonable real return. High-quality 5-year corporate bonds currently yield in the 4.75% to 5.0% range, providing an attractive real return if inflation remains tame. Investment-grade corporate supply has been strong and likely will increase if a rise in mergers and acquisitions materializes. In 2024, $1.5 trillion in corporate bonds were issued, not far below the record $1.75 trillion in issuance in 2020.

There was a welcomed increase in the issuance of municipal bonds before the election, due to uncertainty regarding outcomes and potential policy changes that could negatively impact state and local government issuers. Demand from high-income buyers seeking tax-free income has remained firm against a backdrop of limited supply. Municipal bond issuance had been lower than usual in recent years as state and local governments enjoyed ample stimulus-related and income-tax-related cash reserves and did not have to rely on the bond market for much of their funding needs.

US Government Debt

While US government debt levels continue to grow, the demand for US government securities, both domestically and internationally, remains robust, keeping the cost of servicing the debt relatively low. At some point, investors may reconsider whether they are adequately compensated for the risk associated with financing this level of debt and eventually demand a much higher return. It is too early to quantify the impact on the fiscal deficit of the new administration’s policies. One consequence might be the return of “bond vigilantes,” a term first used in the 1980s to describe investors who dump government debt because of imprudent fiscal policies, causing a spike in bond yields that forces a more disciplined fiscal policy.

Part of the reason that the US is able to finance its debt as inexpensively as it does is that there is a great deal of faith in the independence of the Fed. Investors believe that the Fed will act as the grown-up in the room and take the necessary actions to combat inflation. If administrative policies cause inflation to reaccelerate, the Fed will have to raise rates, which is never a politically popular move. Powell’s term runs until May 2026 and he has said he will not resign beforehand. Trump has said Powell will not be reappointed. The markets are not likely to take kindly to politicizing the Fed or interference by the administration, setting the stage for an interesting next two years of monetary policy.

Part of the reason that the US is able to finance its debt as inexpensively as it does is that there is a great deal of faith in the independence of the Fed. Investors believe that the Fed will act as the grown-up in the room and take the necessary actions to combat inflation. If administrative policies cause inflation to reaccelerate, the Fed will have to raise rates, which is never a politically popular move. Powell’s term runs until May 2026 and he has said he will not resign beforehand. Trump has said Powell will not be reappointed. The markets are not likely to take kindly to politicizing the Fed or interference by the administration, setting the stage for an interesting next two years of monetary policy.

Closing Thoughts

As our 39th President, Jimmy Carter, is laid to rest, he should be given credit for having appointed Paul Volcker as chairman of the Federal Reserve in the summer of 1979. Despite Volcker’s strong advocation for a fiercely independent Fed, and the misgivings of Carter’s advisers for the same reason, Carter gave Volcker the job, believing it to be in the country’s best interests.

The US was plagued by high inflation then, climbing over 13% that year. Volcker raised the Fed funds rate considerably over the next two years, to a high of 22.4%, a politically unpopular decision that resulted in a US recession and a spike in unemployment. While this aggressive stance ultimately broke the back of inflation in the US, which declined to 1.2% in 1986, shortly before Volcker stepped down, the economic consequences were a significant factor in Carter losing the 1980 election.

The US economy is at a critical juncture, marked by both promising fundamentals and uncertainty related to the new administration’s intended policies, which could have a significant impact on both inflation and economic growth. Investors, who do not like uncertainty, have not priced in these risks as evidenced by rich valuations in the capital markets.

While we have provided our economic and market forecasts in this Q4 Investment Review and Outlook, the best recipe for growing wealth is a high-quality, diversified portfolio consistent with your time horizon and long-term investment goals, with an allocation set aside for near-term cash flow needs. We wish you and your loved ones a happy, healthy, and prosperous 2025.

Read pdf here.

All information herein is as of December 31, 2024 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202. ©2025, 1919 Investment Counsel, LLC. MM-00001519