Weekly Market Insights 01.13.25

A Change of Mood

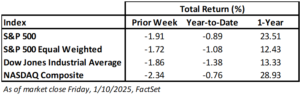

Financial Markets

United States equity markets had a difficult week, driven by stronger-than-expected economic data. Interestingly, under different circumstances, markets may have rallied. However, in the current state of the world, financial markets are dominated by inflation concerns and Federal Reserve decisions. Market participants analyze every new piece of information through the lens of how it will impact the Fed’s monetary policy decisions. The major market indexes declined on the news of a strengthening economy.

This strengthening of the U.S. economy comes as investors and analysts try to analyze President-Elect Trump’s economic plans, which many see as inflationary.

Economics

Since the beginning of the year, markets have reacted somewhat counterintuitively to economic indicators. To some degree, economic strength is bad, and weakness is good. Portfolio managers and analysts are concentrating on monetary policy and the Federal Reserve’s Open Market Committee more than the real economy. Of course, that’s a bit of an exaggeration, but not much.

On Friday, the employment report was released, and it was remarkably robust. Immediately, investors slashed their 2025 rate cut expectations down from two to just one. Perhaps some market reaction stems from concerns that the president-elect’s economic plans may add to inflationary pressures. An immediate reversal in the Fed’s easing trajectory is certainly not a guarantee and, perhaps, not even likely. Economic statistics, government-sourced or not, are not hard truths. It is common for the data to be revised after the fact, and it can often change velocity and even direction unpredictably.

Moving quickly from monetary policy to national income accounting. The growing budget deficit is undoubtedly a looming problem. It might not be quite the immediate problem that some believe, but work must be done soon. However, it seems unlikely that a combination of tariffs, tax cuts, and stricter limits on immigration will painlessly solve the problem. The most reasonable path will require a long-term solution. Under any circumstances, the United States remains the standout economy of the developed world.

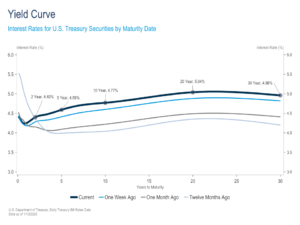

Yield Curve Update

Yields have been on the rise to start the new year, driven, in large part, by reduced expectations for Fed rate cuts and concerns over the inflationary effects of potential Trump policies. As it relates to the former, stickier inflation, firmer growth, and a resurgence in labor market strength have resulted in Fed officials dialing back their expectations for rate cuts in the future. Since the start of the year, 2-year and 10-year yields have increased by 14 and 20 basis points, respectively, while the 2-year/10-year spread has steepened by 5 basis points to 0.38%. Relative to one year ago, the 2-year yield is about flat, while the 10-year yield is higher by 73 basis points, steepening the 2/10 spread from -0.33% to +0.38%.

Last Monday morning, yields briefly declined when the Washington Post reported that Trump’s tariff plan could be dialed back by covering only critical imports. Trump quickly refuted the report, sending yields even higher than they were to begin the day. While tariffs alone won’t single-handedly reignite inflation, all of Trump’s signature campaign promises—sweeping tariffs, mass deportations, and tax cuts—are inflationary rather than deflationary. Notably, Fed officials are factoring in the potential impacts of Trump’s policies in their monetary policy decisions, with the minutes of the Federal Reserve’s December FOMC meeting confirming as much.

Somewhat counterintuitively, the 10-year yield bottomed before the Fed’s first rate cut in September and has risen by more than 100 basis points (1.0%) since. This has played out despite the Fed enacting three rate cuts totaling 100 basis points in rate reductions. While the election outcome, deficit concerns, and Treasury supply dynamics have certainly pressured rates higher, surprising strength in the U.S. economy and implications for Federal Reserve policy have also been dominant factors. In this past week alone, job openings increased, the ISM Manufacturing and Services PMIs came in ahead of consensus, unemployment claims fell to near 1-year lows, the unemployment rate unexpectedly declined, and employers added 100,000 more jobs last month than expected. Last week’s economic reports were broadly consistent with the trend since the Fed’s first rate cut in September. Ultimately, these economic surprises have fueled expectations for stickier inflation, firmer growth, and a stronger labor market. Considering the incoming data, Fed Chairman Powell has indicated that future rate cuts may not be as significant as investors had hoped. Recent comments from Fed officials have confirmed this less dovish policy stance, highlighting additional upside risks to inflation as reasons to proceed with a more cautious and gradual approach to rate cuts this year.

While a stronger labor market is favorable in that it will continue to support wage gains, consumption, and economic growth, the worry is that these factors could lead to another wave of inflation and a hawkish policy response from the Federal Reserve. Fed Funds futures have adjusted accordingly. A few weeks ago, the market was expecting four rate cuts this year but fell to two cuts after the December Fed meeting, and expectations now sit closer to just 1 cut after this week’s stronger economic reports.

Conclusion

If we were to pick a risk to the U.S. markets, it would be economic overheating—not the kind that would force the Fed to slam on the brakes but enough to back away from their easing stance. The rest of the developed world is stuck in an economic and political quagmire. Yes, we know about throwing stones, but the United States economy really is in quite decent shape, especially relative to the rest of the world. Vigilance, as always, is in order.

Read pdf here.