Weekly Market Insights 02.10.25

Confusion

Financial Markets

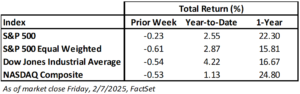

All the major equity market indices lost ground last week. Two driving factors were economic releases and tariffs. On Friday, we received another strong employment report, giving Federal Reserve officials more reason to hold off on further rate cuts. Regarding the second factor, the President announced 25% tariffs on Mexico and Canada but then delayed them in anticipation of negotiations. Investors are concerned that the administration will be inconsistent with its decisions.

We have written many times that uncertainty is the great enemy of markets. For now, uncertainty may be the rule rather than the exception. If the administration continues to operate this way, investors should be expected to maintain a lower risk profile, which would create a headwind to valuations.

Economics

The United States economy remains the leading and strongest on the globe. There is little doubt about that. Although Federal Reserve officials have some level of concern about the economy, their focus is on its strength, not its weakness. Another area of interest for the Fed is the implementation of tariffs, and their potential short- and long-term effects on the consumer, which are directly related to the economy’s growth. One of the problems with tariffs is that there are poor substitutes for innovation and investment. If we want to grow the economy in a non-inflationary way, which the president surely does, there are better ways to do it. One way is to boost productivity through various means. Interestingly, in his first campaign, the president put forth an excellent proposal to achieve just that. His proposal was, and perhaps still is, to get many of our excellent industrial companies to partner with U.S. colleges to create a fertile breeding ground for a highly efficient and adaptable workforce. This plan has the potential to be very valuable. U.S. companies have invested heavily in the most advanced technologies and production facilities and will need highly qualified and adaptable workers.

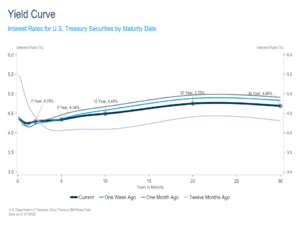

The United States is an economic powerhouse and is improving its position relative to the rest of the world. We wrote earlier about interest rates and the Fed. The Federal Reserve can often be at odds with a president, regardless of who the president is. Elected officials will almost always want low interest rates and easier monetary policy because it will mean happier voters. The Federal Reserve is not an elected body and shouldn’t be. The Fed has a dual mandate to promote price stability and full employment. So, when inflation is running above the target as it is at present, they have a duty to use higher interest rates to temper demand and stabilize price increases. This inevitably makes the party in power unhappy.

The Fed has done a very good job bringing inflation closer to its 2% target without leading the economy into a recession. Despite higher interest rates, the U.S. economy has remained strong, so the Fed proceeding cautiously seems to be the correct decision. Unfortunately, this will likely put the Fed at odds with President Trump. Investors should be prepared to see this conflict escalate.

Europe continues to trail the United States economically, and, consequently, continues to follow an easier monetary policy path. This is to be expected. All else equal, the currency of a country with an easier monetary policy and associated declining rates will fall relative to the other. There is often a misconception that the strengthening or weakening of a country’s currency is positive or negative. It is usually just the market regaining equilibrium.

China continues to be “a horse of a different color.” When working from an underdeveloped economy to a developed economy, China became very dependent on exports. The country has wound up being export-rich while financially pressed domestically. It will likely take quite a while for China to reach equilibrium.

Conclusion

Typically, this long after an election, we would have a better feel for the incoming administration’s plans, especially when the President, Senate, and House are of the same party. That has not been the case this time around. We do not have clarity on the details of the president’s plans, but we do have a decent picture of the economy.

As we have said repeatedly, the economy is in quite good shape. What economists look for are imbalances. If implemented, widespread tariffs could trigger imbalances. However, we have yet to see how that will play out. We are more concerned about the potential economic ramifications of President Trump’s plans when it comes to immigration, particularly the potential for mass deportations.

Aside from political uncertainty, things look good. The Fed appears up to the job, employment is healthy, and inflation, although not quite where we want it to be, is not out of hand.

Read pdf here.