2019 Year-End Tax Planning

Recent changes to estate and gift taxes

The Tax Cuts and Jobs Act (“TCJA”) made major changes to the estate and gift tax. The Act doubled the lifetime exemption from $5 million to $10 million (plus adjustments for inflation) and, in so doing, exempted 99.9% of the U.S. population from federal estate and gift taxation. While this is welcome news for many Americans, this does not mean that you can relax if you live in a state with its own estate tax. States such as Connecticut, Maryland and New York have their own estate tax rules with different exemption levels that must be taken into account when doing estate planning. In all, twelve states and the District of Columbia levy an estate tax. Six impose an inheritance tax. Maryland has both.

Don’t forget about state taxes.

People with estates over the federal exemption amount continue to plan their estates using tried-and-true techniques like valuation discounting. The real differences, however, exist in the space between $5 and $11.4 million where old estate plans employ a testamentary scheme that may not properly reflect the testator’s wishes in a post TCJA world. Do you really want all of your money going to your kids instead of your spouse? That’s what could happen under many old documents that have not been updated for the new exemption levels. To make matters worse, those higher exemptions are scheduled to revert to the pre-2018 levels as of January 1, 2026, unless Congress acts otherwise. One bill floated recently would push up the effective date of the reversion by three years to January 1, 2023. So, for individuals under $11.4 million and married couples under $22.8 million, we advise contacting your estate planning attorney and having your plans reviewed or updated. As the tax law can change quickly, our advice for all clients is to have a conversation with us or your other advisors at least once a year.

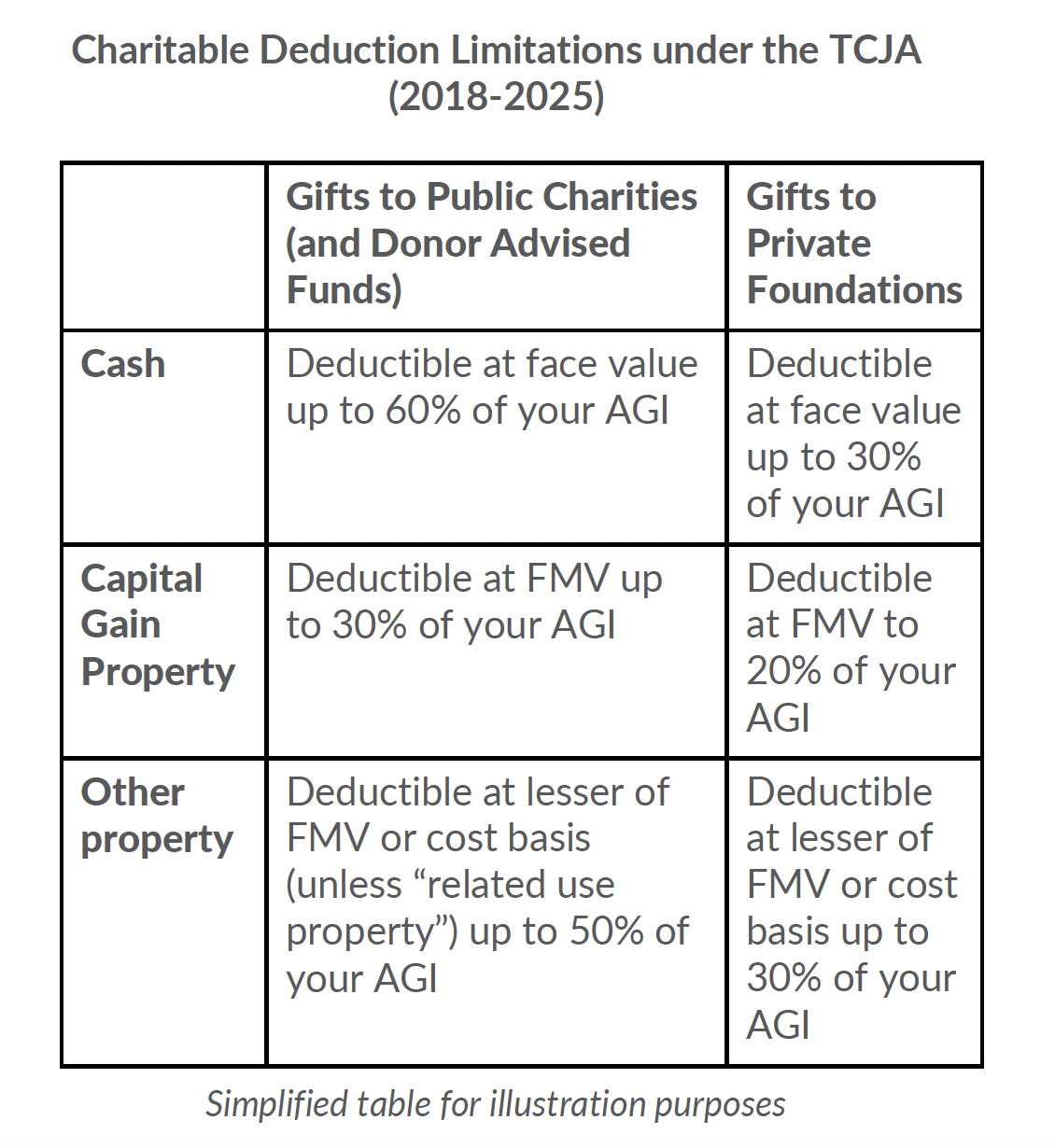

Limits on the charitable contribution deduction

Generally, you can deduct charitable contributions up to 60% of your adjusted gross income (AGI), depending on the nature of the gift and tax-exempt status of the charity to which you’re giving. You can deduct contributions of appreciated property and may claim a deduction for the fair market value of the assets up to 30% of your AGI, depending on the type of charity. The percentage limits are lower for gifts to private foundations. Note that Donor Advised Funds are treated as public charities and are eligible for the higher deduction limits.

Prior to 2018, the maximum AGI threshold for cash donations was 50% of AGI, but under the TCJA this was temporarily increased to 60% through 2025. You can carry over the deduction to subsequent tax years if your gifts exceed these thresholds. Excess contributions can be carried over for a maximum of five years. If you are thinking of leaving a large portion of your estate to charity when you die, we advise starting your philanthropy now and taking full advantage of the charitable income tax deduction.

Planning in a low interest rate environment

Estate planning ideas that should remain viable through 2020 include making tax-efficient gifts via Grantor Retained Annuity Trusts (GRATs) and Charitable Lead Annuity Trusts (CLATs). Both of these techniques work well in a low interest rate environment. If the trust’s assets outperform the IRS’s pre-established rate of return known as the Section 7520 rate (or “hurdle rate”), the appreciation in excess of that rate can pass tax-free to your children. In the case of the GRAT, the donor gets back the value of what was contributed to the trust plus a rate of return at the IRS’s deemed rate. With a CLAT, most of the assets go to charity with an offsetting charitable deduction. So, both offer minimal risk to the grantor. However, there is mortality risk associated with both strategies such that their tax benefits are recaptured if you die before the trust terminates. Also, any invested assets are subject to market risk. Nonetheless, we like both the GRAT and CLAT in times of low interest rates because outperforming the hurdle rate, which is only 2.0% as of December 2019, is achievable as long we have a rising stock market.

Low interest rates offer estate planning opportunities.

Intra-family loans are also a useful technique when interest rates are low. The IRS uses the Applicable Federal Rate (or “AFR”) for these loans, which is even less than the hurdle rate discussed above for GRATs and CLATs. As long as the formalities of the loan are observed (i.e., there is a valid promissory note and actual payments are made in accordance with the note), a child can borrow from a parent at a low rate to buy a home, start a business, or pursue other worthwhile activities. The loan also has the effect of freezing the value of the loaned assets in the parent’s estate at the present value of the note (which, in a low rate environment, will be very close to the loaned principal), while shifting the benefit of any appreciation above these low rates to the child. This excess appreciation can have the effect of transferring value from the parent’s level to the next generation without having to use any of the parent’s lifetime gift exemption.

Opportunity Zones

Under the TCJA, a new type of tax-favored investment fund was created to encourage investment in businesses and real estate located in designated Opportunity Zones. Based on data from the 2010 census, states identified various distressed areas in need of a cash infusion. The idea is to inject private capital into such areas and rebuild them. To achieve this goal, the TCJA included a provision allowing investors to defer paying taxes on capital gains rolled into projects in an Opportunity Zone. The law taxes the deferred gain as of December 31, 2026, but also allows partial basis step-ups along the way after 5 and 7 years to reduce the overall tax. The new law eliminates tax on post-investment gains if you hold onto the investment for 10 years or more. Other tax benefits, such as accelerated depreciation deductions and section 199A deductions, can be used in combination with OZ tax benefits for optimal effect. While Opportunity Zones have a good curb appeal, they still need careful vetting as all deals are not alike. Professional advice is essential.

Retirement reform bill pending

Since the enactment of the TCJA in December 2017, no significant federal tax legislation has been enacted. However, a retirement reform bill is pending in Congress. In May 2019, the House of Representatives overwhelmingly passed the Setting Every Community Up for Retirement Enhancement Act, also known as the SECURE Act (H.R. 1994).

The bill is still pending in the Senate because one Senator wants to expand the use of college savings 529 plans to allow for home schooling expenses. As you can see, the littlest things can cause gridlock in Washington (not that you don’t already know that). Nonetheless, when passed, the SECURE Act would affect IRAs and 401(k) plans as follows:

• 401(k) plans will be allowed to offer a greater array of annuities to participants and plan sponsors would be relieved of certain fiduciary obligations to participants if they comply with a new “safe harbor” rule

• IRA owners would be required to take minimum withdrawals from their IRAs at age 72 instead of age 70½

• IRAs (and 401(k)’s) inherited by anyone other than a surviving spouse would have to be drawn down over 10 (or 5) years instead of over the beneficiary’s life expectancy, thus eliminating the much-loved “stretch IRA”

Passage of the SECURE Act is expected before the end of 2020, if not this year. If the bill passes, we advise that you review your 401(k) and IRA beneficiary designations. Many estate plans include “conduit trust” language so that retirement assets could be left in trust for children. In a post-SECURE Act world, that could lead to an unintended acceleration of distributions to trust beneficiaries.

Tax planning ideas for 2019 and beyond:

Many of the tax planning ideas that we discussed in last year’s year-end update still hold true this year:

• Bunching charitable gifts to allow itemization of all deductions

• Using Donor Advised Funds for charitable giving

• Making charitable gifts from an IRA (up to $100,000 per year)

• Making large taxable gifts in 2019 to lock in the federal gift tax exemption of $11.4 million

• Using the $15,000 annual gift tax exclusion to make gifts to children and grandchildren

What Congress can give with one hand, it can take away with the other.

Thoughts on the upcoming election year

No one knows what the outcome of the 2020 election cycle will be. However, we feel comfortable saying that until December 31, 2020, federal income and estate taxes will remain stable. The good news is this means that we have an environment in which one can plan with relative certainty, at least in the short term. Depending on the outcome of the 2020 election, we could see high net-worth families and their attorneys scrambling to take advantage of the high federal exemption and other tax benefits under the TCJA that may be curtailed under a new Congress or presidential administration.

Here is a summary of a few of the tax increases that have been proposed by various presidential candidates:

• Increase capital gains tax rates

• Eliminate stepped-up basis at death

• Deemed realization of capital gains at death

• Annual “mark-to-market” taxation of unrealized capital gains

• Annual 2% wealth tax on persons with over $50 million

• Reduction of the unified estate, gift and GST tax exemption

• Increase estate and gift tax rates up to 77%

• Automatic GST tax after 50 years for “Dynasty trusts”

• Minimum 10-year term for GRATs

• Estate tax inclusion of “grantor trusts”

• Eliminate Crummey Powers (to prevent use of annual exclusion gifts to trusts)

• Eliminate valuation discounts

• Add a new financial transactions tax

• Increase corporate income tax rates

These are just ideas but all are real proposals. However, until January 2021, we believe that future federal tax changes will be modest at best. A technical corrections bill is also in the works.

Review your estate plan

This is a good time to review your estate plan. The increased estate, gift and GST tax exemptions, as well as planning opportunities afforded by low interest rates provides ample opportunity for those seeking to lower their tax bills. The upcoming election also could change the tax landscape radically. We welcome a conversation about these and other planning topics and invite you to contact your Portfolio Manager or Client Advisor.

WARWICK M. CARTER, JR

Principal, Senior Wealth Advisor

Warwick M. Carter, Jr. is a Principal at 1919 Investment Counsel based in New York. As a Senior Wealth Advisor, his primary focus is generational wealth planning for high net worth individuals and families. He also advises on philanthropic planning. When giving advice, Warwick takes a comprehensive approach to assessing all aspects of a client’s tax, financial and family situation. Warwick works closely with Portfolio Managers and Client Advisors in all of our offices to integrate wealth strategies with a client’s investments. He regularly meets with outside advisors to devise appropriate solutions that will help grow wealth in a tax-aware way over the long term.

Warwick is a graduate of Denison University and the Columbus School of Law at The Catholic University of America. He also holds a master’s in taxation from Georgetown University. He is admitted to the bar in New York and the District of Columbia. Warwick is also a member of the New York State Bar Association and the Society of Trust and Estate Practitioners (STEP).

Email address: wcarter@1919ic.com