Weekly Market Insights 01.08.24

A Shaky Start

Financial Markets

U.S. equity markets opened the New Year on a decidedly weak note. The S&P 500 decreased by 1.52%, the Dow by 0.59%, and the NASDAQ by 3.25%. Not what investors were hoping to see after a remarkably strong 2023. Why the sudden pessimism? As was the case in 2023, it’s all about the Federal Reserve and interest rates. Investors were riding a wave of enthusiasm, trusting that the Fed was on a path to cutting interest rates six times in 2024. They were brought back to earth by an employment report that made them second guess the speed in which rate cuts would come to fruition. Given the magnitude of the 2023 gains, the selloff was not overwhelmingly large. With renewed interest rate uncertainty at the start of the New Year, investors decided to take some profits. Our comments on interest rates below dig a bit deeper.

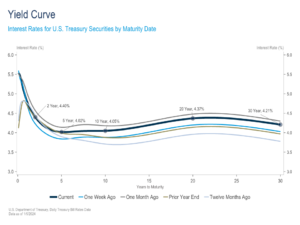

Yield Curve Update

After experiencing a significant decline into year-end, Treasury yields reversed slightly higher in the first week of 2024. Taking a step back, the 10-year yield peaked on 10/19 at nearly 5%, fell below 3.8% on 12/27, and now sits at around 4.0%. Shorter-term yields experienced similar volatility, but, at nearly 4.40% currently, the 2-year Treasury has fallen by a relatively smaller magnitude, resulting in a more inverted curve. Signaling from the Federal Reserve that they have likely ended their rate hiking campaign and economic data progressing in a manner supportive of the Fed’s goals were the primary drivers for the movement lower in yields into the end of the year. However, we have seen a modest reversal higher in the first week of the year, with the 2-year and 10-year Treasury yields rising 12 and 17 basis points, respectively, relative to the week prior. FOMC minutes suggesting that the Fed may be slower to cut rates than the market had priced in and incoming data showing continued economic resilience has led to growing skepticism around the timeline of the Fed’s rate cut path and concerns that recent yield declines were overdone.

Despite an adverse market reaction, one could argue that the economic data to start the year has continued to support the Fed’s goals. Friday’s employment report was the most notable economic release of the week, and while the headline numbers for payrolls, wage growth, and the unemployment rate came in hotter than expected, the details of the report reveal continued labor market cooling. Specifically, payrolls from the prior two months were revised lower by a combined 71,000, the U6 Unemployment Rate[1] ticked higher to 7.1%, the average workweek declined (which helps to offset wage growth), and the household employment survey indicated a 683,000 decline in the number of people employed. The U6 rate has seen a larger increase relative to the more commonly referenced U3 rate, up from an all-time low of 6.5% reached in December 2022 but remains below the 20-year median of 9.6%. Furthermore, lower job openings reported earlier in the week give further credence to the idea that the labor market is continuing to come into balance. All eyes will be on Thursday’s CPI report for more information on inflation, monetary policy, and the trajectory for interest rates.

The Economy

Upon closer inspection, the employment numbers do not, in our view, make us fear a strong reaction from the Fed. Actually, it implies more of the same. We recently wrote that we thought the Fed was on the correct path. We don’t think it would be a wise move for the Fed to aggressively lower interest rates at this time, but, instead believe they should wait a while to see how the economy evolves. Chairman Powell and the Fed have made it clear that they will avoid easing policy too soon in order to prevent a resurgence in inflation. Perhaps they will wait for mid-year to make a move.

Investors’ focus will soon shift to company earnings reports. Investors will be paying close attention not just to earnings, but to discussions about next quarter and beyond. We expect companies to report that they are seeing a slowing of demand but not to a degree that a recession is in the forecast. This should be a positive for investors.

The United States economy continues to lead relative to the rest of the world. The EU is lagging but moving forward. In Asia, China’s economy continues to falter, and the government is not taking the necessary steps to turn its economy around. The government, both national and local, is deeply in debt, while the ratio of consumer debt to GDP is also very high, making it almost counterproductive to try to stimulate the economy by issuing debt. A very interesting economic contest to watch going forward is between China and India.

Conclusion

Our view has not changed one week into the New Year. The United States remains the most desired destination for investors. As U.S. interest rates ease, the dollar should weaken but not substantially so.

Read pdf here.

[1] The U6 unemployment rate includes people who are unemployed, part-time workers who would prefer a full-time position (underemployed), and people who are unemployed but have given up looking for work (marginally attached).