Weekly Market Insights 02.05.25

Equity Markets Rally, Bonds Slump

Financial Markets

Equity markets rallied while bond markets slumped on essentially the same news—just as the textbooks would tell us. The Dow Industrials increased by 1.43%, the S&P 500 by 1.38%, and the NASDAQ by 1.12%. The big differentiator between those indexes was, of course, their exposure, or lack thereof, to the tech sector.

Chairman Powell and the Fed Open Market Committee tempered rate cut expectations this past Wednesday, and economic releases throughout the week came in stronger than anticipated. This, of course, led to quite different reactions by the equity and fixed income markets. At first glance, these reactions are justified by the economics behind them. Additionally, in an interview on 60 Minutes that aired this past Sunday, Chairman Powell reiterated and expanded upon some of these issues. We will get more into how last week’s events impacted yields and fixed income markets in particular in the next section.

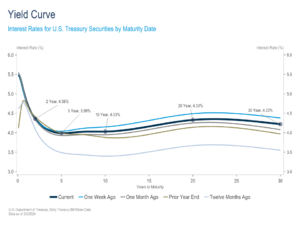

Yield Curve Update

Short-term yields rose and long-term yields declined in what was a volatile week for interest rates. There were both monetary and fiscal policy-related catalysts, including the release of the Treasury’s 1st quarter borrowing estimates, the Treasury’s quarterly refunding announcement, the Federal Reserve’s rate decision, and January’s employment report. Relative to the prior week, the yield on the 2-year Treasury increased 2 basis points and the yield on the 10-year Treasury fell 12 basis points, increasing the yield curve inversion to 30 basis points.

Yields moved lower to start the week when the Treasury reported that they expect to borrow less this quarter than they did in the final quarter of 2023. Later in the week, they announced their plans for Treasury security issuance, opting again to issue more shorter-dated bills and notes rather than longer-dated bonds. Together, these announcements helped to alleviate upward pressure on long-term yields by placating concerns over the government’s rising debt load and the increasing supply of long-term Treasury bonds.

Wednesday brought the conclusion of the Fed’s Open Market Committee meeting and Chairman Powell’s post-meeting press conference. While the Committee’s decision to leave rates unchanged was widely anticipated, Chairman Powell’s comments were not. Most notably, Powell pushed back against March rate cuts by saying he doesn’t see the Fed reaching the level of confidence needed on inflation by their next meeting. In a more dovish tone, he also noted that the Fed isn’t necessarily looking for labor market weakness before cutting rates. In other words, the focus is on inflation eventually returning to their 2% target in a sustainable manor. While the overall takeaways leaned hawkish, yields did not follow suit and declined in the aftermath of the meeting. The day after the meeting, the 10-year fell as low as 3.82%, over 30 basis points lower than it started the week.

Yields reversed course sharply on Friday after a better than expected employment report added to concerns that continued labor market tightness could push out the Fed’s rate cut timeline. Nonfarm payrolls rose by 353,000, the most since January of last year, the unemployment rate remained steady at 3.7%, and wage growth accelerated. However, it’s worth noting that the details of the report indicate a softer employment situation than the headline numbers would suggest. For one, there has been a large divergence between the more often-cited Payroll Survey (survey of businesses) and the Household Survey (survey of individuals). Specifically, while nonfarm payrolls have increased by a cumulative 1.28 million over the past 5 months, the Household measure has declined by 350,000. Furthermore, the average workweek has declined in recent months and made another significant leg lower in the latest report. This means that, despite a month-over-month increase in the number of employed, total hours worked actually fell.

It was an eventful week with a multitude of factors influencing yields. Of course, there were countless other drivers that go far beyond those listed in our recap, but we aimed to highlight some of the major few.

Economics

After reading last week’s headlines, one would likely argue that the economy is gaining momentum, and the Federal Reserve is making a hawkish pivot due to concerns about reemerging inflation. We would push back against that case. Investors should remember that many economic data points are quite volatile, so it is far more important to follow trends rather than isolated releases.

Evidenced by recent price performance, investors are clearly enthusiastic about the technology sector. We have written quite a bit about the potential for a technology-driven third industrial revolution. New technological innovations and discoveries are vital, but something that interests us is new technology going from the realm of scientists into the realm of engineers. In other words, technology is transitioning from what is possible to reality. These types of evolutions tend to have long lead times and may often move in fits and starts. This transition may also have contradictory effects on economic indicators. An interesting example may be a scenario where we see increased production but lower employment and falling inflation. At first glance, that may seem nonsensical, but it is actually quite logical. New technology has the potential to dramatically increase labor productivity, which would then lead to higher production, a substitution of capital for labor, and lower prices. While this transition will be an overall positive for the economy in the long-term, it will also result in some disruptions and related tensions in the short- to intermediate-term.

Conclusion

While investors were disappointed, we think the Fed made the correct decision. There is no need to rush into cutting rates. The economy is neither running away nor plunging, and the same can be said for inflation. Sometimes caution should replace valor. By this, we mean that we are not overly concerned about the direction of the economy or inflation at the moment and think a “wait and see” approach makes abundant sense. Nonetheless, complacency is not a good attitude for investors at any time, and we certainly don’t suggest it now.

Read pdf here.