Weekly Market Insights 03.04.24

All Appears Fine, Except Doubts Remain

Financial Markets

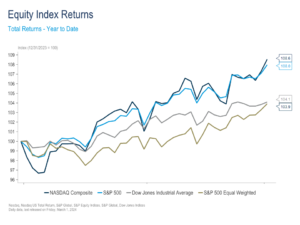

Having just returned from two weeks of vacation, it was a pleasant surprise to see how well the markets did. Over the past two weeks, the Dow rose 1.19%, the S&P gained 2.63%, and the NASDAQ gained 3.16%. Despite the much publicized consumer pessimism, United States equity markets have shown remarkable strength. Adding to our normal listing of the prior week’s equity market performance, this week, we are adding a year to date performance chart.

Some analysts argue that the equity market is in bubble territory. If we look at the year to date performance, you can understand their concern—remarkable, indeed. But, it is important to look at the structure of the performance and the economics behind it. There is really no single accepted definition of a market bubble, so we will point out a number of factors consistent with historical bubbles to see how this market stands up. Many would argue that a bubble is when investors have little or no regard for current or future earnings, and are instead entranced by the rapid rise of the markets. They want in at any price, believing some other investor (or speculator) will bail them out by paying an even higher price. In finance, this is called the Greater Fool Theory. This market has demonstrated a very powerful surge in price and valuation, so it is important to investigate.

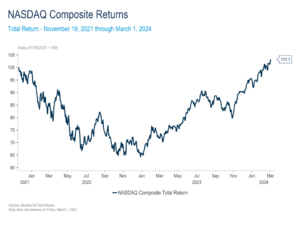

History tells us that markets are inclined to make rapid gains after dramatic falls. Given the current market environment, it may be easy to forget that the NASDAQ fell 36% from its November 2021 peak to its eventual trough in December 2022. The index has returned almost 60% since, but has only just surpassed its prior November 2021 high.

Under the surface of the strong index returns, all has not been equal. Instead, the recent strong performance has really been centered on a relatively small number of stocks in select industry groups as evidenced by the gap between the headline S&P 500 that is weighted by the size of a company and its equal weighted equivalent. In 2023, the size weighted index returned 26.3%, while the equal weighted returned 13.9%. And, so far in 2024, the size weighted index is up 8.0% vs. 3.9% for the equal weighted. One very important issue that defines a bubble is the excessive use of leverage. This we watch carefully and is not at frightening levels yet. This data is released monthly, and, as of the end of January 2024, the level was well below relative previous peaks seen in 2021, 2018, 2007 and 2000. Finally, the earlier mentioned bubble pessimism among some analysts may actually be a good thing by helping to moderate risk taking. This, of course, does not eliminate the chance of high volatility. In fact, volatility is likely to continue.

Economics

The global economy, with a few notable exceptions, appears to be in good shape. The exceptions are the United Kingdom, Germany, and China. After a contested referendum, the United Kingdom left the European Union and has not recovered economically or politically since. Often, a country’s politics and economics can be separated, but not in this case. Neither appears to be near a solution.

Germany is a much larger problem. Since the European Union’s inception, Germany has been the E.U.’s economic leader because of its industrial might. We have written extensively about the problems the European Union faces by having a single currency, with some members being heavily industrial and others heavily agricultural. This problem is compounded by each country having control of its own budget. Additionally, the weakness in China reduces demand for German exports.

China’s economic problems are large and complicated. A lot has been written about China’s woes, although its economic problems have not seriously hurt the rest of the world—at least not yet.

Finally, while doing well, the United States has important economic problems that must be solved, including budget deficits and mounting debt. None seem unsolvable, but we must see the political will to cooperate and find solutions.

Conclusion

Over the past two weeks, not much has happened, except, of course, the equity markets continued to move higher. Other than a bit of political mayhem, the United States appears to be in fine shape at the moment. As far as global monetary policy goes, the European Union will likely ease in order to counter weak economic growth. So far, we have been in favor of the Fed holding rates steady, but if inflation continues on its current path, we expect a rate cut later this year. The FOMC will have to be well in its comfort zone to move.

Although we are not political analysts, we, as almost everyone, are carefully following the political landscape. Here is an interesting suggestion. Readers should be following the national legislative campaigns closely, for they may be far more consequential than the presidential election.

Read pdf here.