Weekly Market Insights 03.25.24

Momentum Ruled the Week

Financial Markets

Momentum players ruled the roost this past week. That is, those stocks that have been the big gainers were again the star players. U.S. markets had their best week in three months. The S&P 500 gained 2.29%, the Dow gained 1.97%, while the NASDAQ gained 2.85%. A remarkable week indeed. Just last week, we wrote that a rotation was in the offing. The market continues to expand, but the top of the market had a strong week as well. There were a number of factors that encouraged investors, from Fed policy discussion, to company earnings, to the end of cycle “don’t want to miss the boat” dynamics. It is fascinating that all three motivations occurred at the same time. In the economics section, we look more closely at some seemingly contradictory market trends. One example is as investors pile into the equity markets, they have also invested in corporate bond funds in record numbers.

Economics

It was an interesting week in the world of economics. The United States economy remains in good condition. Employment appears strong, but inflation remains a bit higher than most would like. Despite the apparent strength of the economy, the Fed indicated that they continue to see three interest rate cuts this year. Cutting interest rates while the economy is strong may appear contradictory, but it is actually supported by number of factors, both domestic and global. The Fed, more than most, understands that monetary policy is a relatively slow moving tool and that indicators are often revised, making caution a positive virtue. Many investors, on the other hand, simply think of Fed activity in terms of interest rates and the immediate market reaction following Fed rate decisions. The difference is the Fed must also consider the real economy which reacts far more slowly and has a less definitive forecast for policy than the financial side. This difference in expectations explains the carefulness of the Fed and the frequent frustration investors have over their actions or apparent inactions.

Conclusion

Even with the apparent contradictions addressed above, our view remains the same. It seems likely that there is a rotation underway. The answer of when we will see a rotation in full force is hard to say, but no one really knows with certainty. Again, the sad state of U.S. politics doesn’t help anyone’s confidence. Where we do feel confident is in both the U.S. economy and financial markets. Europe is improving, while China is in the doldrums. The United States remains the preferred region for investors.

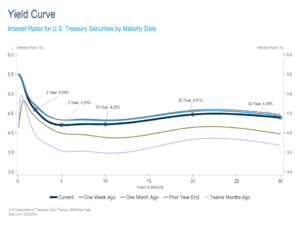

Yield Curve Update

Yields declined this past week after experiencing a notable rise the week prior. In the latest week, the 2-year Treasury yield declined 14 basis points, and the 10-year Treasury yield declined 11 basis points, but the declines were not enough to offset the prior week’s increases. Over the two week span, the 2-year yield increased 12 basis points, and the 10-year yield increased 12 basis points. Furthermore, while the yield curve inversion has lessened in recent weeks, it remains in an inverted state, as it has been since July of 2022.

Two weeks ago, stronger than expected CPI and PPI reports pressured interest rates higher and reminded investors that there may be some bumpiness along the disinflationary path to 2% inflation. While annualized CPI measures showed inflation is continuing to inch closer to the Fed’s 2% target, the month-over-month Core CPI reading increased more than forecasted, and the market pushed out their rate cut timelines as a result.[1] Specifically, following the CPI report, Fed Funds futures were pricing in around a 50% probability that the Fed’s first rate cut occurs in June, down from just under 70% the week before and 100% at the beginning of the year.

The Fed last provided an update to their Summary of Economic Projections (SEP)[2] in December of last year, and, despite calling for three 2024 rate cuts at the time, by January, the market had six to seven cuts priced in. By Wednesday’s Fed meeting, market expectations had converged to the Fed’s December projections, but there was still a fear that the Fed’s updated Dot Plot would reveal a hawkish pivot. Those fears were alleviated after the Fed held rates steady and indicated that recent inflation data had not changed their view on the broader disinflation trend. Importantly, Fed officials didn’t significantly alter their interest rate outlook and continue to see three cuts in 2024—the same forecast that they had in December. The updated projections did incorporate some changes, however. While the median 2024 interest rate outlook was unchanged, the Committee penciled in a modestly slower pace of rate cuts in 2025 and 2026, removing one cut in each year. Furthermore, officials revised their economic growth and inflation outlooks slightly higher.

Fed Funds futures are back to where they were before the hot inflation readings, and now indicate around a 70% probability that the first rate cut comes in June. However, as the last two weeks have illustrated, the future path of inflation and interest rates is far from certain and expectations are constantly in flux. As always, we will keep readers abreast of how the situation develops.

Read pdf here.

[1] Headline CPI increased 0.4% MoM, in line with consensus, but higher than 0.3% in the prior month. Headline CPI increased 3.2% YoY, higher than 3.1% consensus and 3.1% prior. Core CPI increased 0.4% MoM, higher than 0.3% consensus, but in line with 0.4% in prior month. Core CPI increased 3.8% YoY, higher than 3.7% consensus, but lower than 3.9% prior month.

[2] The Summary of Economic Projections (SEP) offers insights on each participant’s assessment of the appropriate path for monetary policy given their respective economic outlooks.