Weekly Market Insights 07.01.24

Soft Market, Disappointing Debate

Financial Markets

Last week, investors lived through a lackluster market and a very disappointing presidential debate. Anyone looking for entertainment or fireworks was sorely disappointed. The potential TV audience must have recognized that in advance since the viewership was down significantly from previous debates.

Completing a rousing first half of 2024, the market has taken a break for the last two weeks. The Dow lost 0.08%, the S&P 500 lost 0.08%, while the NASDAQ gained 0.24%.

As investors consider what’s in store for the second half of the year, they must consider whether or not the Federal Reserve and AI enthusiasm will continue to drive the markets. The answer is that it is unlikely. The Fed has made it clear that they would like to bring the Federal Funds Rate down, but they are not going to risk another bout of inflation in order to do so. Concerning the other market driver, is the infatuation with AI over? Absolutely not! We believe generative AI is still in its early stages and has only just begun to work its way through the system. As engineers and other users start to work with it more and more, basic industries will find productivity-enhancing uses. Investors should remember that AI is a tool, not a product. Over time, it will facilitate many companies to become far more valuable than they are now.

The Economy

Last week, we wrote that we would provide a review of the Congressional Budget Office’s (CBO) Budget and Economic Outlook for the next 10 years. A few caveats—no one, including the authors, expects any degree of accuracy. These are just starting points, and they are frequently adjusted. These are not our projections, and any comments we provide in the future will be in hindsight. Why is this important? These forecasts will be the reference point for legislators when drafting economic policy.

Economic Growth: The CBO projects economic growth to slow from 3.1% in calendar year 2023 to 2% in 2024 with higher unemployment and slightly lower inflation. The CBO expects the Fed to respond by reducing interest rates starting in early 2025. Economic growth remains steady at 2% through 2025 then falls to 1.8 in 2026.

Inflation: The overall growth in prices is expected to slow slightly in 2024. The CBO sees the PCE (Personal Consumption Expenditures Index) falling from 2.7% in 2024 to a level closely in line with the Fed’s target of 2%, and then stabilizing.

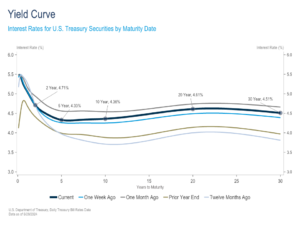

Interest Rates: Short-term interest rates change little in 2024. The rate begins to fall in 2025 followed by a fall in the ten-year in 2026.

Thanks to the CBO for all the hard work. Readers can obtain the entire copy by writing the Congressional Budget Office.

Readers must remember these are projections and are very fallible. It is interesting how closely the CBO’s forecast follows that of the International Monetary Fund (IMF). Interestingly, neither appears to look at the micro level such as industrial changes and how AI may improve productivity. In any case, we thought readers would enjoy seeing this.

Conclusion

We realize we may very well sound like a broken record, but our conclusion remains more or less the same. The U.S. equity market looks expensive, particularly when investors focus on the few stocks that are driving the market higher. So, what are investors looking for? On a very macro level, they would like to see lower interest rates, a more accommodative Fed, and earnings growth broaden beyond just a handful of companies. What are the odds? It certainly appears that the Fed would like to ease at least once before the end of the year. If this should occur, it may be the tide that raises all ships, and we could see an acceleration in earnings that drives the market higher. That could certainly be what plays out, but there are also scenarios that could lead to a market correction. For example, if earnings growth were to accelerate for the broader market, would this present a conflict for the Fed and extend their higher-for-longer stance?

Read pdf here.