Weekly Market Insights 08.05.24

Welcome to a Correction

Financial Markets

This past week was punishing for investors, and the market weakness has only intensified a few hours into the market open. Interestingly, last week began in good shape. Investors awaited the Federal Reserve’s rate decision and Chairman Powell’s post-meeting press conference, which went very much as expected. While the FOMC left rates unchanged, Chairman Powell indicated that the most likely path for rates is lower, with the first cut occurring as soon as September—certainly pleasing news to investors. Then came a flurry of disturbing economic reports and disappointing earnings announcements, and the market turned.

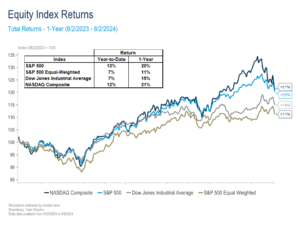

Last week’s equity index performance was lackluster, indeed. The Dow decreased by 2.10%, the S&P 500 by 2.06%, and the NASDAQ by 3.35%. The flipside of the decline in the equity markets was a remarkable rally (lower yields) in the Treasury market (explained in greater detail in the Yield Curve Update section of today’s paper). It is important to note that this activity did not happen in a vacuum. Next, we will highlight the drivers behind last week’s reversal.

The Economy

This past week’s economic releases were disappointing to say the least. After a reasonably encouraging conclusion to the Fed meeting on Wednesday, we received a barrage of economic data indicating that the economy may be considerably weaker than investors and economists had thought. Financial markets reacted as one would expect. Within equity markets, short-term traders protected profits by selling, some longer-term investors took profits, and short sellers had a field day. As we wrote earlier, fixed income investors took it as a buy signal.

Thursday’s release of the ISM Manufacturing PMI[1] and Friday’s employment report were the primary causes of concern that pushed equity markets lower. While the U.S. economy is dominated by service-oriented industries, the Manufacturing PMI is still viewed as a key indicator of overall economic health. Both of these announcements were disappointing, and making matters worse, previous reports of payroll growth were adjusted downward.

To add fuel to the equity short sellers’ fire, some earnings reports, particularly in the technology sector, underwhelmed lofty expectations. On the positive side, year-over-year earnings growth for the overall S&P 500 index the second quarter is still strong at around 11.5%.[2]

Lower interest rates make dividend-paying stocks more attractive. We have written in the past that the heavy investment in technology and the increased usage of AI will make industrials companies more profitable. While the disappointing economic releases are certainly disconcerting, it is important to remember that these numbers are often revised in future releases.

Conclusion

What does this mean for investors? It is a shot across the bow for those who may have grown complacent amid a long-term equity bull market. As it currently stands, with humility and a cloudy crystal ball, we do not expect a bear market or a recession to be imminent. However, we do expect a rate cut from the Fed next month.

Yield Curve Update

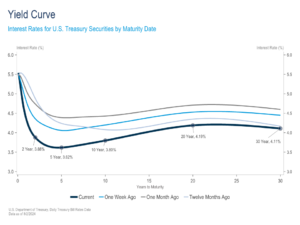

Yields declined sharply this past week, amid concerns that the Fed’s tight monetary policy stance has driven the U.S. economy into a downturn. Growth fears were stoked by a slew of surprisingly weak economic data that came in throughout the week. Most notably, unemployment claims rose to the highest level in nearly a year, U.S. manufacturing activity fell deeper into contraction territory,[3] job openings fell, employment growth slowed, and the unemployment rate unexpectedly increased. Relative to the prior week, the 2-year yield fell 50 basis points, the 10-year yield fell 40 basis points, and the yield curve inversion declined to 8 basis points—the least inverted it has been in more than two years. Since Friday’s close, the yield curve has continued to steepen and even briefly un-inverted earlier this morning.

While overshadowed by this week’s economic releases, we gained valuable insights into the Fed’s monetary policy plans with the conclusion of their July meeting on Wednesday. The Committee left rates unchanged, as expected, but set the stage for a rate cut at their next meeting in September. In Powell’s post-meeting press conference, he noted that recent data had added to policymakers’ confidence that inflation is falling sustainably towards their 2% target. Importantly, Chairman Powell stated that the risks to their inflation/full employment mandate have come into better balance and added that the Fed stands ready to respond should the labor market weaken unexpectedly. Given that Friday’s surprisingly weak employment numbers were reported after the Fed meeting had already concluded, one stands to wonder whether the weakness was significant enough to change their thinking. Fed Funds futures have certainly priced in this possibility, with the odds of a 50-basis point cut in September rising to more than 70%, up from 14% after Wednesday’s Fed rate decision.

Last week’s developments have quickly shifted market concerns from controlling inflation to avoiding recession. While the labor market is still strong by historical standards, and many indicators like consumer spending, wage growth, and GDP suggest the economy is in a healthy position, the recent trend bears watching.

Read pdf here.