Weekly Market Insights 09.30.24

A Tidal Wave of Liquidity!

Financial Markets

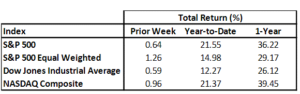

United States equity markets continued to advance this week. The Federal Reserve sent a powerful message two weeks ago when it lowered rates by 50 basis points. Investors interpreted the move to mean the Fed is on a clear easing path and will not hesitate to cut rates more significantly if needed. We will have more to say about global easing trends in the economics section.

Equity markets briefly reached all-time highs this past week but reversed course slightly on Friday.

An interesting thing for investors to watch for is a rotation out of tech-oriented stocks towards consumer-related companies in anticipation of liquidity-driven consumer spending.

Economics

Global markets are suddenly awash with liquidity. The Federal Reserve cut rates by 50 basis points, and, as has been widely publicized, China has ramped up its stimulus to escape the jaws of a severe economic downturn. The Bank of England, European Central Bank, and other central banks worldwide have enacted interest rate cuts. This liquidity injection should give global economies a significant economic boost—all except China. China’s problem is more profound than liquidity. It is structural and much more challenging to solve. We have written about China quite a lot and have not changed our opinion. China is not a quick fix, and it will take time. The solution will involve structural changes requiring political will, but is the political will there?

Most of China’s problems are structural and not monetary. It started after Mao’s death and his disastrous reign. China decided to enter the global economy but only did so halfway. They have built a model with weak household consumption and a strong dependence on debt-financed investment. Ultimately, China has had to sell below cost in many cases and undercut international competitors, but it can only do so for so long. Besides credit repair and monetary policy adjustments, China must stimulate domestic demand. Significant fiscal policy may not be in the cards because it would implicitly drain some power from the Chinese Communist Party. It may seem to some as if we are fixated on China, and in a way, we are. China is a vast country and an important participant in the global economy, for better or worse.

For some time, economists who follow the global economy have noticed an interesting phenomenon. Although productivity has increased from cycle to cycle, the rate of increase has steadily slowed. Although productivity gains are vital in any economy, this has not been a largely poleaxed fact. The International Monetary Fund (IMF) has taken up the cudgel. We thought we would discuss this topic in greater depth for the next few weeks. The reacceleration of productivity is vital for all—from the most backward-facing nations to the most advanced. One of the concepts we will focus on is Total Factor Productivity. We briefly touched on this topic a few weeks ago but will spend more time on it next week.

Conclusion

We wrote earlier that the developed economic world is awash with liquidity. This should keep all but China’s economies faring well. By this logic, financial markets should also continue to advance. Although global economies are improving , the U.S. still appears to be in the best position. Next week, we will discuss Total Factor Productivity and its potential opportunities.

Read pdf here.