Weekly Market Insights 12.11.23

Six Weeks of Gains!

Financial Markets

United States equity markets registered their sixth straight week of gains. The Dow increased by 0.01%, the S&P 500 by 0.21%, and the NASDAQ by 0.69%. All three indexes closed at their highest levels of the year. If this continues, sugar plums will dance in investors’ heads this Christmas. As we will see in the economics section, there remain significant concerns, but the investment skies appear to be clearing. Most of the optimism generated in the markets last week stemmed from the growing assumption that the Federal Reserve will be cutting interest rates next year, perhaps as early as March. This assumption may be a bit Herculean, but it is in the right direction. The second reason is that traders, being notoriously superstitious, know markets tend to rally toward the end of the year.

Economics

A lot is happening in both the domestic and global economies. As we wrote earlier, investors have placed a lot of bullish sentiment on the Fed reversing course and easing as early as March. That seems a bit unlikely, but we suspect the Fed governors are happy or at least satisfied in the direction the economy is going. One thing they want to avoid is easing too early and risk inflation reversing higher. If the economy is on a slow glide path to lower inflation, time is on their side. This is not in any way a negative. It is the wise thing to do and it should not hinder the market’s progress.

Investors appear to be ignoring the domestic political issues that lie ahead. One can hardly blame them. The House has brought the country to the brink several times, only to make a last minute temporary fix.

The U.S. dollar has been weakening. The Wall Street Journal ran a headline about investors dumping the dollar. That is true and the dollar is giving up ground. This, of course, is occurring after a long stretch of gains. The ups and downs of the dollar are interesting, but most often not particularly consequential. Currencies are often in motion, and the reason it was on such a strong run before was Fed tightening. Likewise, the reason for the recent weakening is the belief that the Fed is winning the battle against inflation and will cease tightening, or, perhaps, ease policy. This is positive. Not only does the weakening dollar indicate an easing of inflation, but it helps U.S. exporters gain sales, thereby reducing the trade balance. Currency movements are both fascinating and complicated.

There has been talk of the demise in the role of U.S. dollar as the dominant global currency due to changed structure of the global economy, particularly as it relates to China. The U.S. dollar remains the largest reserve currency at 60% of global foreign reserves, followed by the Euro at 20%. China remains very low at 3%.[1] The rumors of the decline of the U.S. Dollar have been greatly exaggerated. Thank you, Samuel Clemens.

We can’t conclude this letter without providing something for readers to ponder. This is unlikely to affect anyone reading this directly, but it is a problem nonetheless. The number of American families without any or very little pension provisions is concerning. Researchers show that only about 60% of American families have retirement accounts, either defined benefit or defined contribution, although there is some overlap. This is a huge financial and humanitarian problem facing the country. It can be handled but not if we don’t face it now. The unfortunate thing is that this economic problem is unlikely to be solved by economics. Instead, it will call for a serious political solution which lately has not been easy.

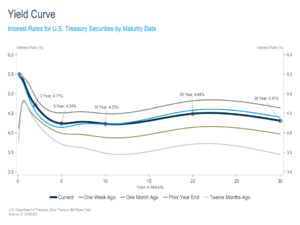

Yield Curve Update

Treasury yields declined significantly over the past month, driven, in large part, by increased investor confidence that the U.S. economy will continue on a disinflationary path, increasing the likelihood of Fed cuts in the near future. Longer-dated yields fell more than yields on the short-end with 10-year and 2-year yields declining 40 bps and 35 bps, respectively. A slew of supportive economic data and more dovish signaling from Federal Reserve officials fueled the renewed optimism. Of note, October’s CPI and PCE indices came in softer than expected, job openings declined significantly to the lowest level since March 2021, consumer sentiment rebounded from depressed levels, and retail spending remained largely steady month-over-month.[2] However, Friday’s hotter than expected employment report provided some slight pushback against this trend, with faster job growth and lower unemployment renewing fears that a persistently tight labor market could force the Fed to hike again. Yields, particularly on the front end, spiked higher following the report.[3] Still, taken together, recent economic releases have further reinforced the economic trends that have been in place for much of the past year—improved labor market balance, a moderation in consumer demand, and continued disinflation toward the Fed’s 2% target. All eyes will be on tomorrow’s CPI report and Wednesday’s FOMC meeting for more information on inflation, monetary policy, and the trajectory for interest rates.

Conclusion

It is difficult to look far beyond the end of the year. Once 2024 begins, the presidential election will come more into focus. The economy continues to fall in line with the Fed’s plans, with activity slowing and disinflation continuing. Dangers remain on both sides of the equation—the Fed overstepping and triggering a recession, or the Fed reversing course too early, causing inflation to return. An extreme in either direction is rather unlikely.

Read pdf here.

[1] Figures from OMFIF 2023. https://www.omfif.org/2023/11/dollar-remains-dominant-despite-growing-demand-for-currency-diversification/.

[2] October headline CPI was flat month-over-month, lower than consensus estimates calling for 0.1% rise. The PCE Deflator increased 0.05% month-over month, lower than consensus calling for a 0.1% increase. JOLTS Job Openings declined to 8.73 million from 9.35 million in the prior month. Michigan Consumer Sentiment increased 13% in November. Retail sales declined 0.1% month-over-month, better than expectations for a 0.3% decline.

[3] The 10-year Treasury yield increased 8 basis points and the 2-year Treasury yield increased 13 basis points on Friday.