Disruptive Innovation Q&A

Insights: Disruptive Innovation Strategy

Technological change is rarely slow and gradual. It often starts slowly but then accelerates, eventually reaching a “tipping point” followed by the establishment of a new paradigm. But it all begins with breakthrough innovation.

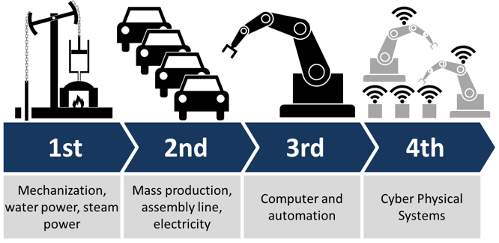

The first industrial revolution was triggered by the steam engine, the second, by electrification, and the third by the internet and automation. In each case, certain companies, the “disruptors”, were able to harness breakthrough innovation to upend existing markets and force technological change.

We believe we are at the beginning of a fourth industrial revolution, where recent breakthroughs in areas such as genomics, Artificial Intelligence, (AI) and 5G wireless networks will empower the next generation of disruptors.

THE FOURTH INDUSTRIAL REVOLUTION

Source: Christoph Roser at AllAboutLean.com.

At 1919 Investment Counsel we have developed a strategy to invest in tomorrow’s leading companies by focusing on how innovation unfolds, rather than on short-term swings in stock prices. It’s diversified across industries, but concentrated in the best-positioned companies within each industry. By keeping turnover low, managing risk and taking a long-term perspective, we are able to capture the compounding benefits of price appreciation in a tax-efficient way.

1. How do you define “disruptive innovation”, and describe the characteristics of the companies you invest in?

First, it is important to draw a distinction between “incremental” and “disruptive” innovation. People often think of innovation in terms of a “better”, “faster”, or “cheaper” version of a product, such as a smartphone or a laptop computer. That would be an example of incremental innovation and is frequently practiced by companies to protect existing sales. It is a legitimate strategy, but one often with diminishing returns. We are looking for companies that view large mature markets as opportunities in which to employ disruptive innovation.

For example, one investment theme we are excited about is Precision Medicine, where a combination of DNA sequencing, genetic tests, and custom-tailored drugs will completely transform medicine, delivering the right treatment to the right patient at the right time. We have recently invested in Illumina (ILMN), the leader in DNA sequencing equipment, and Exact Sciences (EXAS), a leader in genetic testing for colorectal cancer.

In general, we are not looking to invest in companies that may be cheap but mediocre, or to invest in great technology trapped inside a large, mature company. We are looking for the strongest companies that are best-positioned to profit from a disruptive and innovative business model.

2. Explain your strategy for finding stocks and building a portfolio of disruptively innovative companies?

We tend to focus on business strategies which leverage scale in some way, such as through network effects, where the value of the product or service increases with the number of people who use it – think social networks. Another example would be a company that employs data analytics and machine learning. The more data available, the better trained the algorithm, the stronger the product. In each case a natural market structure evolves, where the best companies benefit from positive feedback and become stronger, while weaker companies become less competitive.

In practice, we are looking for companies that are growing sales organically, not through acquisitions, have a market cap of at least 1 billion dollars1, and have reached a certain scale so that their business is self-supporting. After limiting our focus to stocks with these characteristics, we systematically look across industries for potential investments. For the most part, we are looking for businesses with high margins, strong competitive position, and an attractive valuation over an appropriate investment time horizon.

Recognizing that “winner-take-all” dynamics are at play, we limit our selection to the top companies within each theme and diversify the portfolio among several themes. This “thematic diversification” has two main advantages:

- It helps reduce volatility when problems arise in a particular industry. Stock prices often move together in bouts of market hysteria or euphoria, but diversifying thematically helps mitigate industry-specific

- By restricting our focus to only the strongest companies, we increase the likelihood of success in each of our targeted investment

When we value a stock, we think about where the business might be in 3-5 years, rather than the typical approach which is to assume a certain growth rate over the next 4 quarters and apply a multiple of sales, earnings or cash flow to derive a price target.

Disruptively innovative companies often see accelerating growth, not linear growth. By taking a 3-5 year view, analyzing the market opportunity and competitive landscape, we find that the companies in which we are most interested are attractively priced.

3. How is your approach different from thematic ETF’s and Smart Beta strategies?

Thematic ETF’s and Smart-Beta products tend to focus on a single theme and diversify by adding more stocks. The issue with that approach is that to get to a 40-50 stock ETF you are potentially investing in companies that are poorly-positioned or have minimal exposure to that theme.

For example, a typical Autonomous & Electric Vehicle ETF may only have a 1% weight in Tesla and a much higher weight in gasoline-powered automobile manufacturers like Daimler, GM, Ford, Volkswagen and BMW2. Legacy manufacturers may introduce electric models, but we believe Tesla is best positioned to capitalize on broad EV adoption and is well-positioned for autonomous driving, while the others will have to contend with falling gasoline vehicle sales and consolidation.

Our approach is different. Rather than adding more stocks, we add more themes, focusing only on the strongest companies within each theme. We cap the weight of each position to about 5% to contain single-stock risk, and if a stock falls below 1%, we make a decision either to sell it or buy more. We also limit the weight of each theme to about 10%.

Through our thematic approach we gain the benefits of diversification while maintaining strong exposure to the best companies. We aim to hold about 40 stocks and to keep portfolio turnover in the range of 30% or less per year. We believe a buy-and-hold strategy is appropriate for a portfolio of disruptive innovators, which also brings the benefits of low portfolio churn and tax efficiency.

4. How do you think about stock price volatility and manage risk?

We expect that price volatility will be elevated in this strategy given the low turnover, moderate number of holdings, and focus on high-growth companies.

While we do not employ stop-losses thresholds or use options to hedge risk, we do measure the contribution of each stock to the portfolio’s Value-at-Risk (VaR)3 on a daily basis, a commonly used risk management technique to guide our tactical decisions.

It is important to note that we are not inclined to sell a stock based solely on price swings since the investment case for each of our investments is long-term oriented. Our sell discipline is based on an evaluation of the fundamentals, including valuation, and we make decisions based on whether the stock has reached its full potential, the investment thesis has changed in a material way, or we have uncovered a better investment opportunity.

5. How do you leverage the extensive Intellectual Capital at 1919ic?

In several ways. The first is through our Advisory Board, made up of investment professionals who have decades of experience. Each member plays a key role in this collective effort, ranging from fundamental research by our healthcare analyst to discussions about portfolio strategy with senior members.

In addition, we are able to tap into a broad pool of resources at the firm, including 11 fundamental research analysts covering all sectors of the market as well as our colleagues who focus on Socially Responsive Investment (SRI) opportunities.

We are a 100-year old multi-generational wealth manager. Our clients understand that markets can be volatile at times, but they also understand the compounding benefits of long-term investing. This strategy was designed with their needs in mind.

“People tend to overestimate what can be done in one year and to underestimate what can be done in five or ten years.”

-Bill Gates, Founder of Microsoft

6. What role do you see this strategy playing in a balanced portfolio?

Our strategy is best described as “large-cap growth” given that the weighted-average market capitalization of our strategy is typically over $100 billion. For investors seeking long-term capital appreciation, this strategy can provide a growth tilt to a balanced portfolio, or it may serve as the growth arm of a growth-value barbell strategy.

It should be understood that this is a low-turnover, moderately-sized strategy in terms of the number of stocks, where investment decisions are based primarily on fundamentals. While enhanced volatility is to be expected, our belief in developing this strategy is that the long-term compounding benefits of investing in tomorrow’s disruptors will outweigh short-term volatility

1 As of May 2019 the weighted average market capitalization of our strategy was $122 billion dollars.

2 https://www.solactive.com/wp-content/uploads/solactiveip/en/Factsheet_DE000SLA5MZ4.pdf

3 Our Value-at-Risk (VaR) calculation estimates the 1-day negative (i.e. left-tail) return of the portfolio at a 5% probability based on returns from the most recent 90 day period. We decompose VaR into stock-level contributions to manage risk at the security level. More details can be found at: https://faculty.washington.edu/ezivot/econ589/v11n2a4.pdf