Investing & Climate Change ─ Balancing Risks & Opportunities

While the urgency of the COVID-19 pandemic and the current health and economic crises have necessarily dominated the public discourse over the past year, the simmering trouble of climate change and the global push to rein in greenhouse gas (GHG) emissions have not gone away. At 1919 Investment Counsel, we continue to focus on this long term challenge and the impact it can have on client portfolios. We consider climate change – and the societal and governmental response to it – a key theme that poses both threats and opportunities for investors. The threats to specific GHG emitting industries may seem more obvious, but the opportunities for industries, companies, and technologies which are part of the solution abound. At 1919 we focus on examining both sides of this equation for the ultimate purpose of driving more attractive risk- adjusted returns for client portfolios while considering both near term and long term dynamics.

CLIMATE CHANGE: A COMPLEX SYSTEM

Our Earth’s climate is a system of interconnecting feedback loops. With a maddening number of cogs and levers and self-reinforcing actions, changes in climate can have multiple and far-reaching impacts on our global economic and social welfare. As a result, private and public organizations the world over are preparing and enacting plans to mitigate current impacts, moderate behaviors, and transition to a lower-carbon economy.

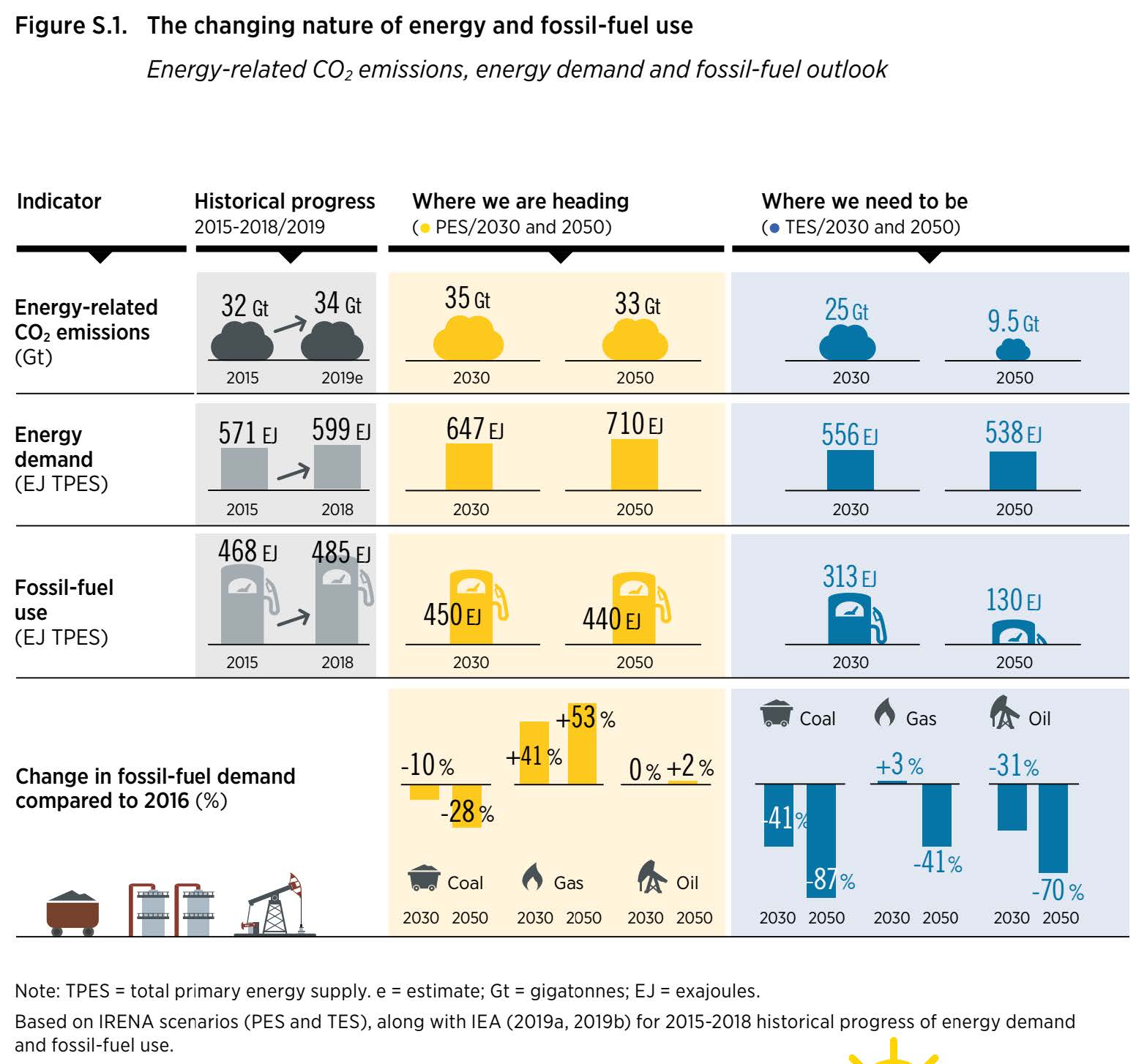

Source: IRENA

WHY INVESTORS CARE

As long-term investors we are less focused on what a target investment company will report as next quarter’s earnings, but are more driven by what we see as the long term value of the company over a multiyear time horizon. We must consider how climate change will impact the operations and assets of the companies we entrust with our clients’ capital. It is not only the direct impact of climate change that we must consider, but also its associated effects: how climate change will drive regulatory changes (e.g. energy efficiency mandates and incentives, carbon taxes, etc.) as well as corporate and consumer behaviors (e.g. consumer preference for companies and products viewed as more climate friendly than competitors). These associated effects are expected to be in play for the long term, making climate challenges an important issue for our long-term investment philosophy.

Source: International Energy Agency

IMPLICATIONS

It isn’t difficult to find examples of what systemic disruptions climate change might bring. One part of our planet – the Arctic Circle – is already experiencing notable impacts. In fact, the Arctic is heating up much more quickly than the rest of the planet. There is a natural seasonal fluctuation, but on November 1, the Arctic sea ice extent1 was 24% less than the historic average; each of the last 13 years has been the lowest sea-ice area per year.2

A shrinking ice cap is both a consequence of climate change and an accelerator; the light-colored ice reflects solar energy while darker oceans absorb energy – less ice leads to more exposed land and water, and warmer water melts more ice. Nations around the Arctic are adapting to more open ocean and uncovered land – we can expect to see more fishing and shipping action on newly accessible routes, as well as increased natural resource exploration and strategic military activity.

Globally, less Arctic ice contributes to sea level rise. In 2019, the global mean sea level was 3.4 inches above the 1993 average. From 2018-2019, the global sea level rose by 0.24 inches. The rate of rise has been accelerating – from 0.06 inches per year throughout most of the 20th century to 0.14 inches per year from 2006-2015. These numbers may seem small but have large impacts. Relative sea level rise can increase the extent and risk of damage when floods occur. Changes in coastlines directly affect the people living there in terms of risk to home and livelihood. For example, between 2000 and 2017, the Atlantic Coast and Gulf of Mexico regions were hit by 13 hurricanes that each caused more than $10 billion in damages. That is real destruction of homes and property, real money spent by states and businesses on recovery, and real opportunities lost, as money spent on repairs isn’t available to be reinvested in community or business growth.

In the U.S., almost 40% of the population lives in relatively high-population-density coastal areas. Globally, eight of the world’s ten largest cities are near a coast. Sea level rise and the increased saltwater inundation, storm surge flooding, and coastal degradation will impact all types of coastal infrastructure including transportation, power plants, chemical, oil, and gas plants, and agriculture. By the end of this century about 200 million people will be newly living below sea level, 70% of which will live in just eight countries with China, Bangladesh, and India leading the numbers.3 An additional 160 million will be affected by higher annual flooding. Coastal areas at risk need to prepare – but what happens if they can’t or won’t? Millions of people will be dislocated, investments will be lost, and nations will risk political disruption.

What kinds of business might be impacted, for better or worse, by sea level rise and the subsequent adaptation and mitigation activities? As an example, think about coastal real estate developments: there are lenders, insurers, builders, utilities, transportation companies, engineering and materials companies, and even municipal bond issuers that are involved. As investors, we need to understand if companies are considering the potential for disruption and are resilient enough to recover from whatever changes may occur.

FIT FOR PURPOSE

As our world attempts to come out of the pandemic- instigated slow-downs and divisive social conflicts, some thought leaders are talking about building back better, or in other words, changing the focus of investments and commitments to a path that is more sustainable for people and planet. One of those areas is investments in energy. Generating energy from fossil fuels contributes to GHG emissions and climate change. It is important to remember that carbon-induced damage isn’t something that can be reversed by simply stopping greenhouse gas emission. The amount of carbon that is currently in our atmosphere won’t disappear or decrease even if we suddenly went to zero emissions. If we want to reach the climate accord goal of keeping global temperature rise to 1.5°C, GHG emissions must begin falling by 7.6% each year starting now.4 However, that positive impact is short-lived and relatively minor in the grand scheme of things because emissions and air pollution are expected to rebound once our economy fully restarts. In order to reach the 1.5°C goal, new investment dollars need to be directed toward energy transition areas.

WHAT ARE COUNTRIES DOING?

The 2015 Paris Agreement under the United Nations Framework Convention on Climate Change (UNFCCC) commits nations to keep global mean temperature rise below 2°C and make efforts to limit to 1.5°C. On Nov 3, 2020 the U.S. formally withdrew from the accord, but most of the world’s countries remain committed.5 In Fall 2020, China, South Korea, and India announced pledges to become carbon neutral. These pledges come with plans to reduce carbon-based (e.g., coal) power sources and support green industries. This transformation will take billions of dollars of investment, some of which is already occurring. While China is estimated to account for about half of global coal demand in 2024, the country has boosted its wind and solar power capacity in the last ten years.

WHAT ARE THE INVESTMENT IMPLICATIONS OF CLIMATE CHANGE?

In the 1919 investment process, we balance multiple factors when selecting the companies in which we invest. Besides financial records, these factors include climate and other environmental, social, and governance factors such as corporate leadership, strategy, resilience, long- and short-term market trends, population trends, political shifts, and regulatory action. We also need to balance the risk of any given investment with the potential for a positive outcome – that is, the opportunity for a value-add payoff. This balancing act must consider the implications of climate change that can now be identified. In some cases, when considering the climate-related risks for any given company we may determine that the risk is acceptable and manageable. In all cases, it is important to have good information. To that end, we support efforts to improve relevant corporate disclosure such as a carbon management policy or whether the company is integrating the potential for changing climate conditions into its long-term planning.

Investing for climate action can come in different forms. In some portfolios, we choose to use divestment, or avoid investing in companies with ownership or significant exposure to real fossil fuel assets. We also use “portfolio decarbonization,” or lowering the overall portfolio contribution to greenhouse gas emissions, and investing in solutions companies.

We are focused not only on the challenges that climate change might pose for investors, but also the opportunities to be part of the solution. We believe that investors don’t have to choose between doing good and doing well in their portfolios; we can help clients by identifying investable ideas in companies that have built businesses that will benefit from the efforts to combat climate change. Some of these themes have begun maturing significantly relative to where they were several years ago. The reasons for this include technology driving efficiency up and cost down (solar, wind, and in some cases fuel cell technology fit this description) as well as public sentiment and regulation that has become more proactive in tilting the scales toward carbon-friendly solutions (biofuels fit well in this category). We have identified several themes that we find attractive. Some of these themes are investable today and some still need additional evolution of the industry, technology, or regulatory framework in order to support a viable business. Below are five themes that are following:

- Renewable energy generation, storage, and transportation – While renewable energy might be the most obvious climate impact investment, this area has suffered from boom/bust cycles in the past and long term investors need to be selective in choosing the right stocks. Our 1919 analysts focus on identifying companies that offer a defendable competitive advantage and sustainable business model that will enable them to survive and prosper through these cycles. Storage and transportation solutions, including enhanced batteries and carbon friendly hydrogen, are key opportunities as well. Wind and solar energy are, by nature, intermittent and not aligned with power demand timing; battery storage is a key enabler for widening the scope and application of wind and solar Hydrogen has potential to be used as a mode to transport green energy from its source to demand centers (“exporting the sun”), although hydrogen powered by renewable energy is a concept that, as yet, has very limited commercial viability until government incentives and technology develop further to spur its growth. Some interesting companies in renewable energy include SolarEdge and Enphase. These companies have shied away from focusing on the more commoditized areas like solar panels and instead have focused on the more complex electronics systems that make solar power safer, more efficient, and help enable power storage, smart home, and electric vehicle (EV) charging solutions as part of a solar power echo system.

- Renewable fuels for mobility – While EVs attract a lot of attention and present some interesting opportunities, biofuels and their supply chains are another area for investors to consider. For example; California has implemented a robust program to drive incentives for low carbon transportation fuels that rewards low carbon alternatives such as renewable diesel from used restaurant grease. Beyond understanding the supply chains, technologies, and supply/demand dynamics, an understanding of the regulatory framework is critical as well, as this regulatory framework can provide opportunity as well as risk of unfavorable changes that must be monitored by investors. Darling Ingredients and Valero Energy have created a profitable Green Diesel joint venture which produces high-quality diesel fuel from waste products and has been recognized as having an 80-90% lower carbon impact than fossil fuel alternatives and benefits from considerable incentives driven by this carbon displacement.

- Energy efficiency, storage, and transportation – A key source of carbon displacement can come from making buildings, factories, and mobility options more energy efficient.6 Opportunities here can come through technologies, engineering, construction, and from capital providers that support investment in more efficient use of energy, often while incorporating renewables into the project or technology solution as well. Hannon Armstrong Sustainable Infrastructure Capital is a financial company that has carved out a niche as a capital provider to climate change solutions including energy efficiency projects as well as renewable energy.

Source: IRENA

- Circular economy – Recycling is an area that can impact climate change and other key environmental Solutions and technologies that drive more sustainable resource conservation of water, metal, plastic, etc. will reduce waste and in turn drive more efficient use of the resources needed to produce or extract the virgin materials.

- Environmentally-friendlier food solutions – Food supply chain waste reduction and alternative food technologies offer significant opportunity to offset one of the key areas of greenhouse gas emissions and environmental stress in the world (see graphic below). Food represents over 25% of all greenhouse gas emissions by some measures.7 Solutions might come from enhanced substitutes for animal proteins or solutions that reduce waste in food production and offer pathways for repurposing or recycling that waste. Beyond Meat is focused on making low GHG meat alternatives that are as, or more attractive to consumer palates than the incumbent animal based options.

CONCLUSION

For the foreseeable future, climate and carbon management will remain a key issue for investors to consider. The global political response in regulation and behavior is dynamic, as are corporate responses and technological advances. As realities evolve, we continue to monitor the investment landscape for emerging risks and opportunities that influence environmental, social, and governance factors that could affect our client portfolios, as well as how corporate activity aligns with the goals of our clients who have chosen to apply values guidelines to their investments.

ALISON BEVILACQUA

Principal, Head of Social Research

Alison is a Principal at 1919 Investment Counsel, LLC and the Head of Social Research. Alison leads the firm’s team of Responsible Investing analysts and SRI Committee to provide research and client service with respect to Values- oriented evaluations, Environmental, Social, and Governance factors, and Impact investing. Alison is a member of the 1919ic Proxy Committee.

Alison joined the firm in 1996 after working the staff of a multi-disciplinary university-based group pursuing

development of an undergraduate business school curriculum that embraced sustainability.

Alison serves on the Governing Board of the Interfaith Center on Corporate Responsibility and the FTSE Russell ESG Advisory Committee. Alison regularly represents the firm at meetings of socially responsible investing-related organizations.

Alison earned her B.A. from the University of Arizona and M.A. in Economics at Miami University.

SHAYA BERZON

Equity Research Analyst

Shaya is a Principal at 1919 Investment Counsel, LLC. His primary responsibility is as an Equity Research Analyst covering the following industries: energy, clean energy and related technology, impact investing, materials, and consumer staples. In addition, he supports portfolio managers as they construct and manage client portfolios. Shaya participates in investment and equity strategy committee meetings.

Shaya entered the Financial Services Industry in 2003. He joined 1919 in 2006. Previously, he was a CPA in public practice and an associate analyst in the equity research department at T. Rowe Price.

Shaya volunteers with several local community organizations and serves as a board member of BJSZ, a congregation in Northwest Baltimore serving over 300 local families.

Shaya holds an M.B.A. in Finance from Johns Hopkins University as well as a Bachelors and Masters in Talmudic Law from Ner Israel. He is a state of Maryland Certified Public Accountant (inactive).

1 Sea Ice is frozen ocean water. Sea ice grows during the winter months and melts during the summer months, but some sea ice remains in the region all year.

2 https://www.bloomberg.com/graphics/climate-change-data-green/ice.html?sref=orcXmzh8

3 https://www.statista.com/chart/19884/number-of-people-affected-by-rising-sea-levels-per-country/

4 https://sdgs.un.org/goals/goal13

5 We note that President-Elect Joe Biden is likely to re-engage the U.S. in the Paris Agreement climate accord.

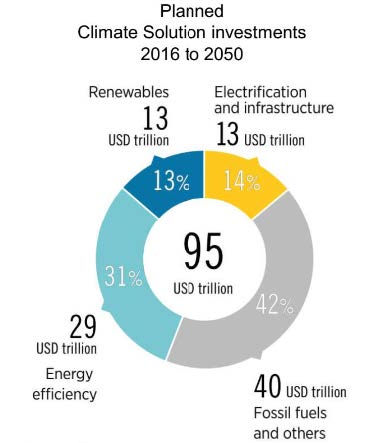

6 IRENA estimates this amount based on current plans in place while stating that Paris compliance would require $110t and that there is room for a $130t scenario as well.

7 Poore & Nemecek Science magazine 2018 with further elucidation here.