Equity Compensation Plans: What do I need to know?

Today,[1] about 43% of public companies and 35% of private companies provide equity compensation benefits to their employees.[2] Employers are increasingly offering this type of compensation to enhance employees’ total pay and provide them with incentives as direct owners in the company.

Receiving a portion of your compensation in equity may sound straightforward (and exciting if you’re part of a quickly-growing team); however, the mechanics can become complicated quickly.

This article introduces the main types of equity compensation plans, and strategies for maximizing your benefits.

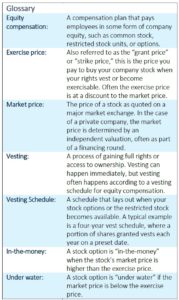

After reviewing the glossary to the right, let’s start by examining some of the most common equity compensation plans.

Common Types of Equity Compensation Plans

It’s essential to understand your particular type of plan in order to maximize your available benefits.

Stock Options

In contrast with listed options, such as puts and calls, compensatory stock options are awarded to employees as part of their total compensation. In particular, early-stage companies often grant stock options to employees in lieu of higher salaries, promising the potential for greater upside post-IPO or as the company matures.

A stock option gives you the right, not the obligation, to buy shares in your company at a specified price at a certain time. Often the exercise price is below the market price, allowing the option holder to profit from the immediate sale after exercising the option.

There are two stock option grants: Incentive Stock Options (ISO) and Nonqualified Stock Options (NQSO). ISOs are often given to senior executives and key employees, while NQSOs are more commonly used for other employees. You can verify the type of options you have by looking at the option grant agreement provided by your employer. The option grant agreement will also spell out when your stock options vest. Typically, options vest over four years, with a quarter of the shares available for exercise after the first year, and the rest vesting monthly over the next three years.

Restricted Shares

There are two types of restricted shares: (1) Restricted stock, which is typically granted to company directors or executives, and (2) restricted stock units (RSUs), which are awarded more broadly across an organization. With RSUs, employers grant a specified amount of shares that follow a vesting schedule, typically annually. Unlike a stock option, there is no exercise price. The employee receives the RSUs and can sell or hold the shares beginning at the vesting date. An RSU is more like a promise to be awarded shares of stock at a particular time if certain conditions are met, such as continued employment. Unlike restricted stock, RSUs are not actual stock, meaning RSU holders do not receive dividends or have shareholder voting rights. However, once the RSUs vest, the employee will receive unrestricted shares in company stock.

Employee Stock Purchase Plans

An Employee Stock Purchase Plan (ESPP) allows employees to buy shares in their employer’s stock through direct paycheck deductions. The big incentive for this plan is a discount of 5% to 15% off the current market price. In addition, ESPPs frequently have a lookback period that will give the employee the lowest price over a specified date range. An ESPP is a great way to supplement retirement savings between the lookback period and the discounted purchase price. Keep in mind the maximum annual purchase in an ESPP is $25,000, per current Internal Revenue Service rules. These plans are also designed for the long-term saver.

Strategies to Maximize Your Equity Compensation

There are many ways to act on your equity award, and there is no one-size-fits-all answer. The right strategy will be the one that fits within your unique financial situation and goals. That said, here we introduce some common scenarios that may be helpful as you consider your options. For guidance on your specific situation, please contact us directly.

Sit tight

ESPPs are a good fit for the long-term saver. With ESPPs, the best strategy is often to sit tight. With ESPPs, the shares will move up and down based on the market price, and holding the stock allows the investment to grow over time, akin to the buy-and-hold strategy that some investors employ. You also will be entitled to receive dividends on your shares as long as you hold them.

Image Source: Shutterstock

If you are early in your career and in the active wealth-building phase, ESPPs can be a fantastic tool to accumulate more shares of your company. Over time, as the strategy succeeds, the natural consequence is a position in your company stock that will be larger than your other positions. Eventually, this position may grow to become a concentrated position. As you wind down active working years, a concentrated position can become a risk management issue that requires close monitoring and a strategy to unwind and diversify.

Keeping this in mind, ESPPs, like restricted stock and RSUs, can offer paths to upside potential that are unavailable to non-employees. Long-term capital gains can be a powerful wealth-building tool if used thoughtfully in the context of your overall financial and investment plan.

Exercise and hold

Stock options are a different sort of animal, especially before a company has gone public. Leaving stock options alone may result in a sizeable missed opportunity. At the same time, it comes with significant risk. For example, since an early-stage company’s share price often increases substantially post-IPO, it can be beneficial to exercise your options at a lower valuation. Since these are compensatory stock options, you would owe taxes on the exercise, but the taxes due will be substantially lower than after the IPO if the stock goes up substantially. Before making this decision, please check with your 1919 Investment Counsel advisor or with your tax professional.

Selling to meet cash needs or diversify

If you are buying a home, paying educational expenses, or covering major medical bills, you may cash-in rather than invest your equity compensation awards. In such cases, the need for funds sooner rather than later supersedes other considerations. Additionally, periodically selling company stock and reinvesting in other sectors is a good strategy to diversify wealth, depending on your overall exposure and risk tolerance.

It’s not uncommon to hear about a lower-level employee who never sold her company shares and is now a millionaire. Unfortunately, there are less publicized tales of employees losing big chunks of their wealth due to sustained drops in their company’s share price. Particularly for those getting multiple, large stock options or restricted stock grants, regular selling of a portion of your company stock is a prudent step to protect your wealth. Be careful to consider blackout periods and insider trading rules that limit when you can sell your shares.

Tax Considerations

Talking about taxes isn’t typically a favorite pastime, but rash or uninformed decisions about your equity compensation can result in a surprise tax bill. Generally, the most meaningful tax savings are achieved by paying the lower, long-term capital gains tax rate instead of the higher ordinary income tax rate. Based on current federal tax brackets, many taxpayers with equity compensation will be subject to the 15% federal capital gains tax rate. In contrast, the corresponding ordinary income (and short-term capital gains) tax rate will be materially higher, likely in a range of 22% to 37%. A 3.8% Net Investment Income Tax may apply as well. Accordingly, there can be substantial tax savings by having your equity compensation gains taxed as long-term capital gains rather than as ordinary income.

Stock options: NQSO vs. ISO

ISO stock options are less common. They receive more favorable tax treatment, as there are no taxes due when granted, vested, or exercised. Taxes on ISOs are deferred until the shares are sold, and the gains are taxed at long-term capital gains rates as long as you hold the stock for at least two years from the grant date.

NQSOs, on the other hand, have a more complicated tax treatment. The difference between the market

price when you exercise and your strike price, or “bargain element,” is taxed at your ordinary income tax rate as compensation. This cannot be avoided. However, if the stock is held for one year after exercise and two years after the grant date, then the subsequent stock price gain qualifies as long-term capital gains.

One final note: exercising and holding can subject you to the Alternative Minimum Taxes (AMT) if you sell within two years of the grant date, so check with your tax professional before deciding.

Restricted Stock

If your employer grants you restricted stock, you may be able to be taxed on the value of the restricted shares at the time of the grant instead of at vesting by making an election under section 83(b) of the tax code. This is advantageous if the stock has great upside potential between the grant and vesting dates. If you make an 83(b) election, the value of the stock will be taxed as ordinary income at the grant date and will establish your cost basis in the shares upon vesting. Further, the time frame for measuring long-term capital gain will begin as of the grant date. There is some risk here, though: Because restricted stock is subject to forfeiture if you leave the company or otherwise don’t qualify for vesting per terms of the stock grant, you could have to pay taxes on the compensation you don’t receive. Another downside is that the shares may lose value.

RSUs

With restricted stock units, the market value of your stock on the vesting date is taxed as ordinary income. The IRS treats this as compensation income. Your employer is required to withhold taxes and typically does so by taking back some of the RSUs at vesting. Going forward, your cost basis in your shares is the market value on your vesting date. If you hold the stock for a year beyond the vesting date, the gains on the sale are treated as long-term capital gains. Unlike restricted stock, an 83(b) election is not possible with RSUs.

ESPP

No taxes are due when money is deducted from your after-tax paycheck to purchase company stock in an ESPP. Taxes become relevant when you sell because the discount received on the initial purchase may be taxed as ordinary income. If you sell more than one year after the purchase date and two years after the grant date, the gain is taxed at long-term capital gains rates. On the other hand, if the shares are sold within a year of purchase or two years of the grant date, then all or part of the gain is taxed as ordinary income. If you sell within two years of the grant date, the bargain element will be taxed to you as compensation and reported on your W-2 form. All else being equal, selling shares in an ESPP should be focused on reaching dates when the gains are considered long-term and thus eligible for the lower capital gains tax rate.

Conclusion

We hope you have a better understanding of some equity compensation plans and important considerations when evaluating your equity compensation offer, but we are happy to answer any questions you have. Together, your 1919 Investment Counsel advisory team can help you develop and deploy the best strategy that protects and grows your wealth.

JIM O’CONNOR, CFA, CFP®

Principal, Portfolio Manager

Jim is a Portfolio Manager with 1919 Investment Counsel, LLC. He has more than 15 years of experience in the financial services industry, focused on equity analysis and managing portfolios for individuals, families, foundations, endowments and institutional clients.

Before joining 1919 Investment Counsel, Jim was a Portfolio Manager with Rand & Associates, an independent Registered Investment Advisory firm. Prior to joining Rand & Associates, Jim was an Investment Analyst at ArrowMark Partners in their Larkspur, California office. Earlier, he spent approximately a decade as a Research Analyst and Portfolio Manager at Aster Investment Management in San Francisco.

Jim received his BA from UC Berkeley and an MBA from the University of Southern California. He holds the professional designations of Chartered Financial Analyst (CFA) and Certified Financial Planner™ (CFP®) and is a member of the CFA Society of San Francisco.

Outside of work, Jim enjoys playing the guitar, playing soccer and spending time with his wife and two kids.

Email address: joconnor@1919ic.com

Read pdf here.