Weekly Market Insights 02.06.23

The Fed Slows with Mixed Economic Signals

Financial Markets

U.S. equity markets closed Friday on the downside, but the S&P 500 and NASDAQ still had excellent gains for the week. The Dow closed down 0.15%, the S&P 500 closed up 1.62%, and the NASDAQ closed up 3.31%.

As anyone who follows the markets is aware, investors were eagerly awaiting the Federal Reserve’s announcement on interest rates last week. The question surrounding the meeting was whether Chairman Powell and the voting members were going to hold rates steady, slow the increase to 25 basis points (quarter of a percent), or continue with another 50 basis point hike. Investors were happy that the rise in the Fed Funds rate was on the low side, and interpreted Chairman Powell’s press conference remarks as dovish, and the market rallied. The theory behind the positive reaction is that the economy is slowing and the Fed is responding with lower interest rates, making a soft landing a bit more likely. Alas, at the end of the week, the jobs report came out far stronger than investors expected, and the market lost some ground. However, the jobs announcement was not too damaging to investors’ psyche, as the market closed the week with considerable gains. Last week’s performance continued a very positive year. One important point is that if the FOMC didn’t know the jobs number, they still had a very good idea of what it was. Despite this, they moved in a less aggressive way anyway, showing confidence in their policy actions.

The Economy

As January has come to a close, we have a detailed report on the past month’s economic indicators. In our economics portion, we will isolate three areas—central banks, labor and jobs, and international.

Interestingly, after an extended period of behaving in lockstep, Chairman Jerome Powell and his counterparts at the Bank of England and European Central Bank, Andrew Bailey and Christine Lagarde, respectively, have diverged, with the ECB being the most hawkish. There are good reasons for the Fed and ECB to begin to diverge on the rate of interest rate increases. The first and most obvious is that the Fed started raising interest rates much earlier than the ECB. Furthermore, wage rates in the United States have shown signs of slowing, while they continue to rise in Europe. Wage growth without a corresponding increase in labor productivity is a principal cause of inflation, and Europe hasn’t seen adequate labor productivity for their current level of wage growth.

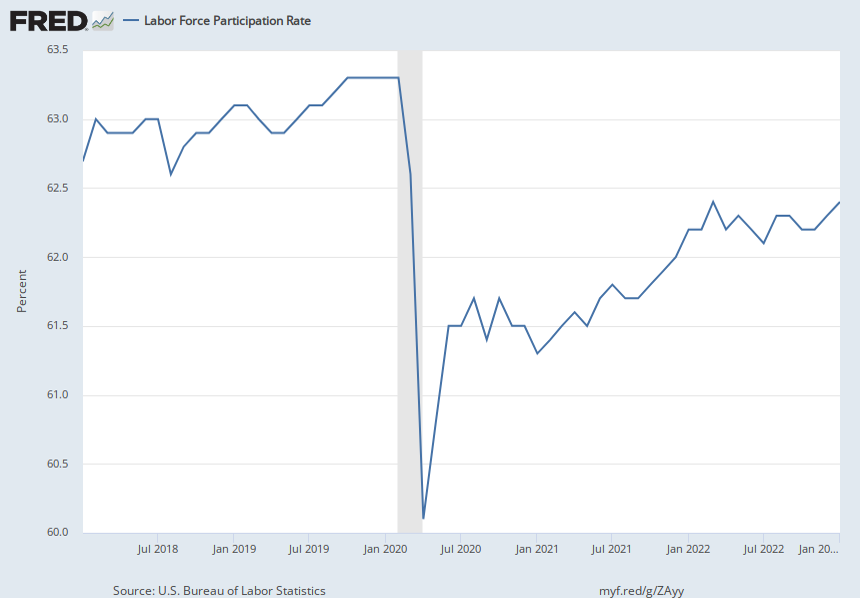

The United States also has labor problems, but they don’t appear to be influencing inflation to the same degree as in Europe. The primary labor question in the U.S. is, why is the labor force shrinking? No one seems to have a solid answer. What is interesting is the reduction of the Labor Force Participation Rate.[1] It appears, for some reason, people are dropping out of the labor force; there would be 2.9 million more workers today if the Labor Force Participation Rate was the same as in February 2020, according the U.S. Chamber of Commerce. No one appears to have a satisfactory answer. Some have argued that it is related to Covid. That was a reasonable explanation for a time, but the impact of Covid is slowing and should be reflected by an increase in the participation rate. Another argument is that due to Covid and various social needs, the country’s automatic stabilizers are too generous. That is possible, and, if true, the labor force should increase over time as the impacts of these social assistance programs fade. As you can see in the chart below, the Labor Force Participation Rate has struggled to return to its pre-pandemic high.

Conclusion

The Fed’s move is encouraging, but it shouldn’t be considered the end of tighter monetary policy. The economy has plenty of problems, some unsolved and others the Fed appears to be getting a handle on, but there remain questions. Unfortunately, many of the remaining questions are in the realm of politics, and are inclined to be pushed back in hopes that they go away. As we pointed out last week, investors should not focus on the strength of the dollar as a signal of strength or weakness of a particular country. In fact, it proves neither.

January Economic Indicator Update

January’s economic indicators showed further signs of disinflation, but also increased labor market tightness and increasing consumer strain. While inflation has been the dominant economic issue for some time, increasing concern over slowing growth and a potential recession has intensified in recent months. The labor market is central to this competing growth-inflation dynamic. While a strong labor market provides key support for consumption and economic growth, it may also act to prolong or intensify inflationary pressures. A slowing economy will almost certainly bring increased job cuts, but the hope is that an initial reduction in job openings will succeed in easing wage pressures with minimal associated consumer pain.

Inflation Indicators

Sticky housing and rental inflation was an area of focus for much of 2022, but, with more real-time indicators suggesting shelter disinflation is on the horizon, the focus has shifted to core services—an area highly impacted by labor market strength and wage inflation.

- The Consumer Price Index declined 0.1% month-over-month, down from November’s 0.1% rise, bringing the year-over-year rate to 6.5%. Core CPI increased 0.3% in December and 5.7% from the prior year.

- Shelter was once again a dominant contributor, making up 1/3 of the headline CPI measure and 1/2 of the core.

- Deemed as the “most important” inflation metric by Fed Chairman Powell, the price index for PCE services minus housing and energy rose 4.1% from a year ago, down from 4.3% in November.[2]

- This alternative metric is seen as a better measure of core services inflation and includes spending on services like health care, education, hospitality, dining out, haircuts, and more.

Labor Market Indicators

After several months of slowly cooling labor market data, many of January’s employment indicators reversed course sharply. As we have stated previously, the next leg lower in inflation will be largely dependent on increased labor market slack, as an improved labor supply-demand balance should lessen wage pressures and translate to more tempered consumer demand. Compensation makes up a sizeable share of operating expenses for service-oriented businesses, so reduced employment costs will diminish the need for price increases to offset those costs. While we continue to see some anecdotal evidence that companies are slowing hiring in preparation for an economic slowdown, the labor market remains very tight by most metrics.

- Non-farm payrolls increased 517,000, well ahead of consensus estimates for a 185,000 rise. There were also upward revisions to prior months totaling 71,000.

- The Unemployment Rate fell to 3.4%—the lowest reading since 1969.

- Labor Force Participation ticked up 0.1 percentage points to 62.4%.

- The Employment Cost Index (ECI) increased 1.0% in the 4th quarter and 5.1% year-over-year. This marks a deceleration from the 3rd quarter’s 1.2% pace.[3]

- JOLTS (Job Openings and Labor Turnover)[4] job openings rose back above 11 million, higher than 10.4 million in November and the highest reading since July.

- In a report from the outplacement firm Challenger, Gray & Christmas, Inc.,[5] layoff announcements increased 440% from the prior year, and job cuts rose 136% from the December 2021. January layoff announcements totaled 102,943.

Consumer-Related Indicators

After a prolonged period of conflicting data, consumption indicators have started to follow consumer confidence readings lower. We are seeing a depletion of savings, increased borrowing, and lower spending, potential signals of mounting consumer strain.

- Michigan Consumer Sentiment rose 8.7% from December but is still about 3% from levels seen this time last year. Sentiment is also very depressed from a historical perspective.

- Conference Board Consumer Confidence decreased slightly in January with a 6.7% decline in the Expectations component reflecting consumers’ concerns over the economy in the next 6 months.

- Real Personal Consumption Expenditures fell 0.3% month-over-month, a sharper slowdown than November’s 0.2% decline.

- Retail sales dropped 1.1% in December, following November’s 1.0% decline.

- 46% of credit card holders are not making their payments in full each month, up from 39% a year ago. Even more concerning, 43% of those with debt are not aware of the rates associated with their cards.[6]

Economic Growth Indicators

Real (ex-inflation) GDP growth in the 4th quarter was solid, coming in at a 2.9% seasonally-adjusted annual rate. As a whole, 2022 GDP grew just 2.1% from 2021, including two consecutive quarters of decline in the first half of the year. 2022 reflected the return to a more normal pace of growth after 2021’s stimulus and reopening fueled surge. With many economic growth indicators weakening further in January, expectations are for below-trend growth in 2023.

- Industrial Production fell 0.7% in December, following November’s 0.6% decline.

- Core Durable Goods Orders fell 0.2% month-over-month, following November’s 0.1% decline.

- January’s ISM Manufacturing PMI fell to 47.4, marking the second consecutive month in contraction territory and the lowest reading since May 2020.

- The ISM Services PMI surprised to the upside, increasing to 55.2 but follows a 49.6 reading in December.

While inflation has shown encouraging signs of decline, increased labor market slack has not yet developed. Even with a strong labor market, cracks in consumer strength are beginning to materialize. Inflation in the services sector has proven to be sticky, and it looks as though we will need to see more significant labor market weakness and reduced consumer demand before substantial improvements can be made.

Read pdf here.

[1] The Labor Force Participation Rate is defined by the Current Population Survey (CPS) as “the number of people in the labor force as a percentage of the civilian noninstitutional population […] the participation rate is the percentage of the population that is either working or actively looking for work.”

[2] Graham, Jed. “The Fed’s New Key Inflation Rate Eased in December; S&P 500 Rises.” Investor’s Business Daily, January 27, 2023. https://www.investors.com/news/economy/fed-key-inflation-rate-may-trip-up-the-sp-500/.

[3] ECI captures total employee compensation, including wages and benefits. Benefits includes things like health insurance, retirement plans, and paid time off.

[4] JOLTS stands for Job Openings and Labor Turnover Survey. This measure tells us how many job openings there are each month, how many workers were hired, how many quit their job, how many were laid off, and how many experienced separations.

[5] Challenger Gray Layoff Announcements are published by Challenger, Gray, and Christmas, Inc. on a monthly basis. This release provides information on the number of announced corporate layoffs by industry and region.

[6] Smith, Paige. “Consumers Roll Over Debt Without Knowing Their Interest Rate.” Bloomberg, January 10, 2023. https://www.bloomberg.com/news/articles/2023-01-10/us-consumers-roll-over-more-credit-card-debt-as-inflation-bites?sref=J9GPLx1B.