Investment Review & Outlook – July 2023

Key Takeaways

The US economy has remained fairly strong, delaying the onset of a recession resulting from the Federal Reserve increasing interest rates 10 times over the last year. A mild recession is our base case as we expect the interest rate environment will slow economic growth eventually, increasing financial pressure on consumers and corporations alike, while helping the Fed achieve its goal of reining in inflation.

The US economy has remained fairly strong, delaying the onset of a recession resulting from the Federal Reserve increasing interest rates 10 times over the last year. A mild recession is our base case as we expect the interest rate environment will slow economic growth eventually, increasing financial pressure on consumers and corporations alike, while helping the Fed achieve its goal of reining in inflation.- The strong performance in equities during the quarter was based more on relief over the debt ceiling resolution, signs of cooling inflation, and enthusiasm surrounding artificial intelligence (AI) than on improving company fundamentals. This leaves the market at lofty valuations and in a vulnerable position as the Fed continues to slow the economy with higher rates.

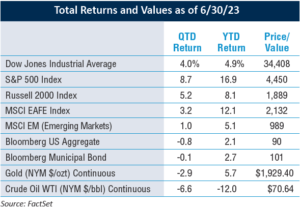

- While the commonly quoted cap-weighted S&P 500 Index has returned 16.9% year-to-date, this is somewhat misleading in terms of overall market strength, given that this return was driven primarily by only a small handful of stocks. In stark contrast, the equal-weighted S&P 500 Index returned 7%.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

The Economy

As we reach mid-year, the strength of leading indicators, such as unemployment levels, wage growth, and consumer spending seems to indicate a recession is not on the immediate horizon. The persistence of inflation, despite the Fed’s aggressive action, likely means there are more rates hikes to come.

Monetary policy operates with a lag, and the Fed’s tightening regime to slow growth may gain significant traction as we enter the latter half of the year. Money supply has dropped, commodity prices are weak, and there are early signs of slowing growth in some areas of the US. However, the fundamentals behind sticky inflation remain problematic. The supply of labor, including from immigration, does not show signs of improving. Similarly, housing, another important component of inflation, may remain supply-constrained for some time. With factors such as these in mind, the Fed has indicated it will resume increasing rates.

Unemployment Levels & Wage Growth

While weekly unemployment claims recently have trended slightly higher to the 250,000 range, the labor market remains strong. A 300,000 level may be a key Fed data point that will signal rate hikes are helping to slow growth.

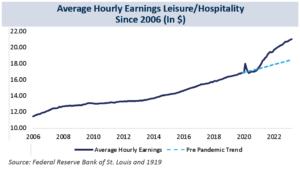

Likewise, even though the number of job openings per available worker has declined, labor demand still substantially exceeds the supply of available workers. Wage growth has been strong, with employers increasing salaries in order to retain staff and attract talent, indicating the labor market remains tight, and therefore making it more difficult to rein in inflation. The wage pressure has been most evident in areas such as retail as well as leisure and hospitality as shown in the following chart.

US Consumer Spending Trends

With labor market strength, it should come as no surprise that consumer spending remains robust, although with a shift in demand towards consumer staples and away from spending on discretionary items such as apparel and electronics.

MONETARY POLICY OPERATES WITH A LAG, AND THE FED’S TIGHTENING REGIME TO SLOW GROWTH MAY GAIN SIGNIFICANT TRACTION AS WE ENTER THE LATTER HALF OF THE YEAR.

Consumers also appear to be favoring larger retailers once again. During the pandemic, lack of inventory at larger retailers (such as Walmart and Amazon) drove some consumers to other sources. That trend is beginning to reverse, as larger retailers regain market share.

Inventory availability has meant an increase in promotional sales activity and advertising spending. Large retailers benefit from scale and have the financial resources to incur substantial advertising costs. These advantages enable those companies to take market share from smaller competitors, a scenario that may be magnified if recessionary pressures on smaller retailers increase.

A Word About Housing

The housing market appears to be in relatively good shape. New-home sales have picked up, which is not something we would expect during a period of rising interest rates and a slowing economy. This is partly due to a supply-demand imbalance that has sparked new construction activity.

However, existing-home sales have slowed. Homeowners with low mortgage rates are less likely to sell their current home and buy a new one at today’s higher rates. Consequently, we find ourselves in a unique environment where existing-home prices remain relatively robust while sales activity actually has slowed.

What The Fed Is Forecasting

Although at the most recent meeting in June, the Fed paused after 10 consecutive rate increases, it signaled the likelihood of two more rate hikes in 2023. The pause provides an opportunity to take stock of the impact of Fed policy and any ongoing fallout following the banking-sector turmoil in the spring. At the same time, the economy has not slowed meaningfully enough for the Fed to have achieved its goal, and the commitment to the 2% inflation target stands.

The sentiment of Federal Reserve Chairman Powell after the last FOMC meeting is clear:

“Inflation has moderated somewhat since the middle of last year. Nonetheless, inflation pressures continue to run high, and the process of getting inflation back down to 2 percent has a long way to go.”

-Chairman Powell

A Challenging Economic Environment Ahead

The US economy may not yet be in a recession, but we are witnessing a number of states that may be heading in that direction, as indicated by upticks in unemployment. For example, California, with a significant $3.6 trillion GDP (the highest in the US) and a state that may be considered a leading indicator for US economic activity, now has an unemployment rate of 4.5%, up from 3.8% in Summer 2022.

Higher interest rates raise borrowing costs for both consumers and corporations, which, in an economy dependent on credit, does some of the Fed’s work by dampening demand. This trend was further exacerbated by the banking crisis earlier this spring which increased pressure on lending and constrained the supply of loans to consumers and businesses.

Consumers will feel financial pressure as the economic environment becomes more challenging while interest rates remain high. This, in turn, will make it difficult for companies to implement price increases, and corporate profit margins will narrow with profits suffering as a result.

The Equity Market

Relief & Enthusiasm Sparks Rally

The recent rally in the equity market was fueled primarily by a collective sigh of relief over the government’s debt ceiling deal, as well as the sudden and growing enthusiasm surrounding the potential of AI to impact every area of our lives. Developments in AI, led by the rapid adoption of large language models such as ChatGPT, proved to be a tailwind for the technology, communication services, and consumer discretionary sectors driving performance that lifted the overall market in the second quarter. Anticipation that we have moved closer to the end of the Fed’s rate hike cycle further reinforced investor optimism.

However, the market rally was not based on improving near-term fundamentals or a rosier outlook for corporate earnings, therefore we expect market volatility to return as investors renew their focus on earnings, and recessionary pressures increase.

A Concentrated Mega-Cap Tech Story

The story of the equity market in the second quarter was truly a tale of a concentrated handful of mega-cap stocks (Nvidia, Microsoft, Meta, Alphabet, Amazon, and Tesla, for example) driving the performance of the entire S&P 500. The result was a year-to-date total return of 16.9% for the market-cap-weighted index. This is a significant divergence from the equalweighted index total return of 7% for the year. The equal-weighted index values all stocks in the S&P 500 equally, regardless of market-cap. With a market-cap-weighted index, if a stock or sector rises significantly, becoming more expensive, it takes on a larger weighting and therefore has an outsized impact on the index, possibly distorting the return.

While these stocks may lead the charge for some time, returns eventually will normalize, either with the rest of the market catching up or these mega-cap stocks cooling to more reasonable valuations. The following charts show the significant overall impact a few stocks in three sectors had on the overall market.

As a result, stock prices have risen without a commensurate increase in corporate earnings, driving up P/E multiples and making valuations less compelling. In comparison, the earnings yield of stocks (earnings per share/price per share) has narrowed relative to the 10-year Treasury yield, as interest rates have increased. When this ratio narrows, it suggests that there is less compensation to an investor for the risk of owning stocks relative to bonds, in the near term.

When interest rates rise, equity multiples compress, which may be a potential headwind for equity returns later this year or in early 2024. However, from a longer-term perspective, it is important to note that stocks will continue to play an important role in providing growth in a diversified portfolio.

The Fixed Income Market

The Fixed Income Landscape

Apart from the Fed’s monetary policy actions, supply and demand factors have been impacting the taxable fixed income market. Following the debt ceiling agreement in June, the supply of Treasuries is set to rise considerably, in particular the supply of Treasury bills which mature in one year or less. The Federal Government looks to borrow up to $1 trillion by year-end through new Treasury issuance.

TODAY’S HIGHER INTEREST RATE ENVIRONMENT, WITH BOND YIELDS NEAR THEIR BEST LEVELS IN YEARS, PRESENTS INVESTORS WITH OPPORTUNITIES TO BENEFIT FROM COMPELLING INCOME ACROSS THE FIXEDINCOME SPECTRUM.

In addition to the increase in the supply of Treasuries, the Fed is moving forward with its quantitative-tightening program whereby Treasuries and mortgage-backed securities continue to roll off of its balance sheet monthly, driving down the price of these securities which causes yields to rise. This means that investors, not the Fed, must absorb any new supply, leaving less liquidity in the financial system.

Somewhat countering the dynamic in Treasuries is a decrease in the net supply of corporate bonds, as many companies pulled forward issuance last year ahead of the onset of Fed rate hikes, and the pace of mergers and acquisitions died down. Against this backdrop, we expect rates to be volatile, although we do not expect the 10-year Treasury yield to rise much above 4% as an economic slowdown takes hold.

However, investment-grade corporate bonds are not yet signaling a recession, as spreads relative to Treasuries remain below the historical average of 151 basis points, dating back to 1973 (a basis point is one hundredth of 1 percentage point). The spread currently stands at 123 basis points. Corporate bond spreads typically decline when investors are pricing in less risk. An expected decline in corporate issuance and the general good health of corporate balance sheets, should help keep spreads somewhat in check as well.

Ample Opportunities For Yield

Today’s higher interest rate environment, with bond yields near their best levels in years, presents investors with opportunities to benefit from compelling income across the fixed-income spectrum. Some short-term bond yields are near 5%, while the two-year Treasury yield reached 4.87% as of June 30. In addition, most sectors of the bond market have returned 3% – 4% this year.

With the potential for two additional Fed rate hikes this year, we expect the higher interest rate environment to persist. After years of low, lackluster yields, it is now an environment where bonds can provide meaningful income while continuing to serve as ballast for navigating equity market volatility.

Yield Curve Inversion Considerations

Currently, short-term rates remain well above 10-year Treasury yields, creating what is known as an inverted yield curve, long considered to be a leading indicator of a recession. The inversion also appears to reflect investor sentiment that rate hikes eventually will slow the economy meaningfully, at which point the Fed may have to cut rates if unemployment spikes and economic growth slows too much.

An Update On Municipal Bonds

If the economy does go into recession, as we forecast, slowing growth may result in credit-quality deterioration for some municipalities. At this point, however, many states are in good shape financially, with ample rainy-day funds in hand and high-quality municipal bond offerings.

For investors, municipal bond issuance continues to be lackluster. Due to constrained supplies, muni bonds remain expensive relative to Treasuries, with short-term Treasuries offering a more attractive risk/reward scenario.

OUR PERSPECTIVE

The pros and cons of this higher interest rate environment are working their way through the US economy. Investors are benefiting from income opportunities provided by higher-yielding bonds more than they have in years. At the same time, higher interest rates are putting pressure on consumer and corporate cash flows, dampening economic activity by making new investments or major purchases less attractive. Slower growth helps the Fed in its fight to bring down inflation but likely results in some shorter-term recessionary pain, especially when accompanied by higher unemployment.

While a concentrated cadre of mega-cap technology, communication services, and consumer discretionary stocks have led the charge, posting notable returns year-to-date, we expect a resumption of market volatility to be a headwind as the economy slows, which typically is a challenging period for stocks. Focusing on high-quality companies with the resilience to navigate future market storms will be an important factor through the remainder of the year.

At 1919 Investment Counsel, our overarching mission is to focus on your goals: from managing cash flow to generating income and growing wealth. We are committed to implementing and managing your investment strategies, with an eye towards the most compelling opportunities in the equity and fixed income markets, and while navigating market volatility and looking to mitigate risk. We hope you and your family have a safe and enjoyable summer.

Read pdf here.

All information herein is as of June 30, 2023 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202.

©2023, 1919 Investment Counsel, LLC. MM-00000559