Weekly Market Insights 09.11.23

The G-20 without China and Russia

Financial Markets

Equity markets declined last week, led by two dominant technology companies. They are, of course, Apple (AAPL) and Nvidia (NVDA). The Dow fell by 0.75%, the S&P 500 by 1.29%, and the tech-heavy NASDAQ by 1.93%. Friday found some relief, but it was clearly a tough week for investors. Equity prices were influenced by rising interest rates, but, as we write later in the economics section, fear of rising interest rates may be a bit premature.

Economics

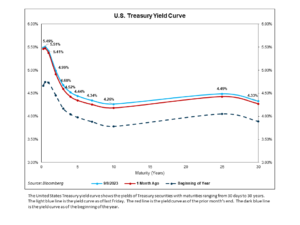

As always, investors are correctly concerned about the future posture of the Federal Reserve. Recent economic releases argue that inflationary pressures may be easing, allowing for some more leeway in the Fed’s future tightening plans. We caution, of course, that all economic releases are famously variable and can be subject to volatility. Economic growth appears to be slowing, and, as we highlight later, the yield curve appears to be moving in the right direction, at least for the time being (see chart below).

Although the future of the economy remains uncertain, we are starting to see more and more that, “This time may be different.” An argument can be made that it may actually be true this time. Without going into the theory of cycles, here is our thought process.

Cycles, particularly economic cycles, consist of a series of smaller sub-cycles. They tend to move sequentially. While the economy is still strong, some of the early sub-cycles may begin to weaken progressively until the economy collapses and recession arrives—unpleasant but somewhat orderly. What happened this time was the pandemic. It interrupted the cycle, not allowing it to come to an orderly conclusion, so many of the sub-cycles never came to an end. This has caused confusion among analysts. All of this is just a complicated way of explaining that an inverted yield curve may not predict a recession this time.

Briefly, on the international side, the G-20 met without the helpful presence of China and Russia. It all went well.

Next week, we will explore in more depth China’s efforts to transform the loosely-organized BRICS into something formidable enough to challenge the West.

Conclusion

The United States economy appears to be in a somewhat better position than previously thought. Relative to other regions around the world, U.S. markets, both equity and fixed income, continue to play a dominant role in most investors’ portfolios.

Yield Curve Update

Since our last update two weeks ago, the Treasury yield curve became less inverted by 8 basis points. Declining yields on the front end of the curve (maturities less than 10 years), paired with increasing yields on the long end (10 years +) drove the change. While the shape of the yield curve changes for countless reasons, the two major and interrelated factors that we will focus on are Federal Reserve monetary policy and variances in economic activity.

On the economic front, softer labor market data along with indications of a growing but not overheating economy drove increased confidence that a soft landing may be achievable, or, at the very least, that a recession is not imminent. Releases showing decelerating payroll growth, decreased job openings, a slight uptick in the unemployment rate, and month-over-month consumer income and spending growth all worked to support longstanding hopes of achieving improved labor market balance without realizing significant consumer pain. Ultimately, these economic developments led to investor optimism that less restrictive Federal Reserve monetary policy and stronger economic growth may be on the horizon, materializing in lower rates on the front end of the curve.

Of course, there are many other explanatory factors behind yield curve movements, but our goal is to provide a general explanation behind major changes.

Read pdf here.