Weekly Market Insights 09.18.23

A Bad Week for Tech

Financial Markets

Technology stocks, the market leaders for the year, reversed course and drove equity markets down this past week. Of course, there were other pressures, but the tech sector stood out. The Dow was the only index that could hold any of the gains from earlier in the week. The Dow gained 0.12%, the S&P 500 lost 0.16%, while the tech-heavy NASDAQ lost 0.39%. There were a number of issues weighing on investor sentiment, both domestic and global. Investors, who have been growing more and more comfortable with their Fed outlook, will be waiting anxiously for the FOMC meeting and rate announcement this week.

Economics

A number of economic announcements last week may have made investors reconsider their view on both inflation and interest rates. The Consumer Price Index (CPI) rose more than expected, the culprit mainly being the price of energy. One of the most discouraging things about inflation pressures stemming from energy prices is there is not much that the U.S. can do about it. Higher prices at the pump led to a lot of talk about political failure, but the price of energy is globally determined. Having said that, shale oil companies have slowed drilling in favor of returning capital to investors, but that is not the main reason behind the recent rise in oil prices. Russia and Saudi Arabia’s decision to extend production cuts has been the main cause. The consumer, who represents about 70% of the U.S. economy, continues to spend at a strong pace, but higher energy prices may present a headwind.

As we know, the auto workers have gone on strike. They are seeking significant increases in pay and benefits. The strike, of course, will detract from economic growth if it lasts long enough, and it will drive up auto prices. An interesting sidebar—we have written in the past about the substitution of capital for labor. The companies will almost certainly give in to many of the strikers’ demands, but it may very well hasten the capital for labor transition. In the short-run, this would be somewhat disruptive, but, longer-term, it would dramatically increase efficiency, lowering costs and prices.

Globally, the European Central Bank hiked interest rates another 25 basis points. Paradoxically, the Euro fell, particularly against the U.S. dollar. Theory tells us that when a central bank raises rates, that country’s currency should appreciate. One potential reason this did not occur is continued struggles in Germany, the dominant EU economy. Much of Germany’s malaise stems from the slump in China. Weaker demand from China has weighed on German exports and negatively impacted the country’s economic growth.

This, of course, brings us to China. We have written frequently about China and its economic problems, but, just this past week, President Xi complicated the analysis. A second high ranking official has disappeared—Defense Minister Li Shangfu. It is difficult to explain the disappearance, as secrecy is a byword of Chinese politics, and both ministers were appointed by Xi recently. This occurs as China is struggling, not only to get out of a recession but to establish leadership in the newly-expanded BRICS.

Conclusion

Investors looking around the globe can be excused if they think confusion reigns supreme. All this and the United States is entering what promises to be a very acrimonious election season. Still, the United States remains the most advantageous place to invest. Higher yields have presented investors with an interesting choice between equities and fixed income—not a terrible position to be in.

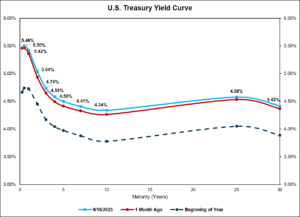

The United States Treasury yield curve shows the yields of Treasury securities with maturities ranging from 30 days to 30 years. The light blue line is the yield curve as of last Friday. The red line is the yield curve as of the prior month’s end. The dark blue line is the yield curve as of the beginning of the year.

Read pdf here.