Weekly Market Insights 11.06.23

A Great Week for Equities—Will it Last?

Financial Markets

It has almost become axiomatic that an equity rally follows a bond rally. That is just what happened this past week. Market participants, having seen the latest economic releases and Fed comments, have decided that the Fed’s most likely path is to hold rates where they are, and the central bank’s next serious move may even be easing. The political and economic world remains in a flux, but there are signs that the inflation clouds may be parting, letting some light shine through. There are a lot of interesting things happening in the economic world, but more about that later.

The Dow gained by 5.07%, the S&P 500 by 5.85%, and the NASDAQ by 6.61%. Investors should be happy with this turn of events but should also remember this is happening on the heels of a very difficult three months. An interesting but counterintuitive truth is, in the world of equities, all eyes are on the bond market.

Economics

U.S. hiring is slowing according to the latest Bureau of Labor Statistics (BLS) data. The payrolls gain was the smallest since June. Cooling labor demand is in line with some other ongoing economic developments, like rising borrowing costs and increasing energy prices due to the wars in the Middle East and Europe. Along with reduced hiring, wage growth slowed moderately from September. Interestingly, despite the labor participation rate ticking lower in October, there has been some growth in the size of the labor force with workers being enticed back by higher wages and benefits. An increase in labor supply is just another factor contributing to declining pressure on wages. Taken together, what we are seeing is a balancing of the supply and demand for labor.

Looking globally, China’s economic struggles continue. They started with the misguided effort to rapidly grow their economy by hyping the real estate market with quasi-government loans. As they flooded the country with money, they simultaneously embarked on a project to build goodwill, project their power, and increase their influence internationally. This project is known as the “Belt and Road Initiative.” The program involved lending billions to developing countries for infrastructure projects, and, to most China watchers, has been a failure. Many loans are now in default, and the much anticipated goodwill vanished when borrowers found out the contractors had to be Chinese. It does not appear that China’s economic problems are going away anytime soon.

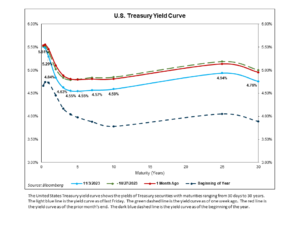

Yield Curve Update

The Treasury yield curve experienced a bull flattening move last week, with long-term rates decreasing more than short-term rates. Generally, “bull flattening” occurs when investors expect inflation to fall in the long-term, which, if proven true, would provide the Fed with more room to cut rates in the future. Relative to just one week prior, 10-year yields declined by 26 basis points, while 2-year yields fell by 18, combining to result in a more inverted curve. While the yield curve is subject to countless influences, the primary catalysts for last week’s moves were Federal Reserve monetary policy and economic releases.

Wednesday marked the conclusion of the Federal Reserve’s October Open Market Committee (FOMC) meeting, after which Chairman Powell addressed the media in his post-meeting press conference. While the Fed’s decision to hold rates steady for a second meeting in a row was widely anticipated, Powell’s press conference comments were not. Powell largely reiterated the Fed’s unwavering commitment to controlling inflation, but he also downplayed the “efficacy” of the September dot plot projections which called for one more rate hike before year-end and fewer cuts in 2024. Ultimately, investors interpreted these comments as a dovish turn from the central bank, driving longer-term inflation expectations and interest rates lower.

Friday’s cooler than expected employment report provided additional downward pressure on long-term yields. October’s 150,000 payroll additions came in below estimates, and hiring in the prior two months was revised lower by a combined 101,000. The Unemployment Rate ticked up to 3.9%, and hourly earnings came in cooler than expected. Despite a slight decline in the Labor Force Participation Rate to 62.7%, Friday’s employment data was, overall, indicative of improved labor market balance, adding to investor confidence that the Fed’s tightening campaign could be coming to an end.

Economic Indicator Update

Taking a step back, October’s economic releases were more of a mixed bag, with indicators relating to economic activity, the labor market, inflation, and consumer health sending inconsistent messages. Despite this variability, indicators are generally conveying the same message that they have been for several months now—slowing growth, improved labor market balance, lower but increasingly sticky inflation, and a resilient consumption despite growing consumer strains. The bullet points below include some recent economic indicator highlights:

- In the preliminary reading for 3rd Quarter GDP, growth was reported at a 4.9% quarter-over-quarter annualized rate, higher than consensus calling for 3.8% and an acceleration from the 2nd quarter’s 2.1% growth.

- The Core PCE Deflator decelerated to a 3.7% year-over-year rate, a tick lower than the prior month’s 3.8%.

- JOLTS Job Openings rose slightly to 9.55 million, consistent with the prior month but still very elevated relative to the 6.5 million unemployed, indicating that the labor market remains tight.

- Personal Consumption Expenditures increased 0.7% month-over-month, higher than the 0.6% consensus estimate and 0.4% rise seen in the prior month.

- The Michigan Consumer Sentiment Survey declined 6% in October, following two consecutive months of very little change. The Expectation sub-index drove most of the decline, falling 10% from the prior month.

Conclusion

Recent economic releases have given investors and analysts hope that the inflation clouds are clearing. Certainly, the United States remains the best positioned economy globally. It is, in a way, a thumbs up for capitalism. This doesn’t mean last week’s rally will continue non-stop. Free markets tend to move in fits and starts, and geopolitical tensions remain sharply elevated. In fact, it would not be uncommon for last week to have been considered a relief rally within the longer-term trend.

Read pdf here.