Weekly Market Insights 05.20.24

Markets Continue to Rise

Financial Markets

United States Equity markets continued their remarkable run this past week. The Dow increased by 1.24%, the S&P 500 by 1.54%, and the NASDAQ by 2.11%. The equity markets have clearly been the stars of the investment world. Interest rates, the Fed, and inflation have been the focus, so, logically, this past week’s inflation reports were top of mind for analysts and investors. While the report was certainly positive and must have pleased the Fed, the question of when they will make their first easing move remains unanswered. This is not meant to throw a damper on investor enthusiasm, but it should serve as a reminder that economic data is volatile and one report does not mark a trend.

The Economy

The Federal Reserve wisely continues to be circumspect when discussing plans for future rate cuts. There has been a lot of press about trade, tariffs, and globalism, and, as we get closer to the election, the talk will most likely become louder and more shrill. Free and open trade is an excellent way for the global economy to operate. Unfortunately, it depends on everyone obeying the rules and this has not been the case. China and Russia are in the process of forming a partnership, and, rather than participating in a free trade world, they are trying to play by their own rules. In this case, the problem is not Russia. When is the last time anyone purchased anything with the label “made in Russia?” China, of course, is a different story. The United States and the West should not allow China to disrupt trade, no matter how tempting it may be to use trade as a campaign tool. Having said that, the United States appears to be in good economic shape. Inflation is slowing, the economy is growing, and there are signs that housing supply is improving.

Conclusion

Although we argue that the U.S. economy’s progress looks bright, the equity market has made rapid advances, and investors should keep this in mind. This is not a warning or a clever way to say the market is overbought. We are simply reminding investors to always remain vigilant.

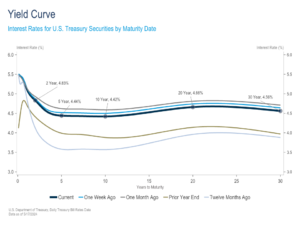

Yield Curve Update

Yields have been on the decline in recent weeks after reaching a year-to-date peak in late April. Fueled by a stretch of weaker economic data, encouraging inflation reports, and comments from Federal Reserve officials, the 10-year Treasury yield has declined from just above 4.7% to around 4.4% over the last three weeks. The decline in the 2-year yield has been more modest, falling around 20 basis points over that same span, widening the yield curve inversion to 40 basis points.

A streak of weaker economic data paired with some welcome inflation news has helped drive yields lower. Of note, employment growth slowed notably in April, the unemployment rate ticked higher to 3.9%, and earnings growth decelerated to an annualized 3.9%. On the economic growth front, retail sales decelerated and surprised to the downside, consumer sentiment dropped by 13% in May, and Industrial Production underwhelmed, coming in flat month-over-month. Together with this week’s lower than expected CPI report, recent economic data may have provided some reprieve for Fed officials looking to gain further confidence that the economy is not overheating and that inflation is on a sustainable path towards 2%.

Federal Reserve officials have been consistent in their “higher for longer” messaging, but they have also signaled that the Fed’s next move is more likely to be a cut than a hike. While comments from Chairman Powell and other FOMC members have been far from dovish, the Fed’s bias towards cutting over hiking is evident. Judging by the reaction in yields, market participants are seemingly gaining confidence that the economic data will cooperate and that the long-awaited Fed rate cut is within sight.

Read pdf here.