Weekly Market Insights 06.10.24

Mixed Economic Signals, Market Strength Continues

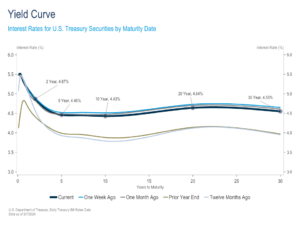

Financial Markets

Economic indicators gave mixed signals this past week, and investors had mixed reactions. The most noteworthy economic news came on Friday with the employment report. Interestingly, job creation came in stronger than consensus estimates, while the unemployment rate unexpectedly ticked higher. In other words, although job creation grew, joblessness also grew in an apparent contradiction. Investors chose to concentrate on the bearish side of the report (joblessness) in hopes that it encourages the Federal Reserve to cut rates sooner rather than later. It probably is a good idea to instead think that the two data points discount each other. Nevertheless, equity markets finished the week with gains.

The Dow gained 0.29%, the S&P 500 gained 1.32%, and the NASDAQ gained 2.38%. The question of when the Fed cuts rates remains unanswered. Interestingly, the Information Technology sector continued to lead the market, followed by Health Care and Communication Services, while Energy and Utilities stocks were the laggards.

Economics

As we alluded to in the opening, Friday’s employment report provided mixed signals about the labor market. Nonfarm payrolls grew by a higher than expected 272,000 in May, and the unemployment rate was up by a 10th of a percent to 4.0%—still quite low relative to historical averages. Friday’s employment report should not encourage the Fed to make changes anytime soon.

While the Fed may not be making any major changes, there are still interesting developments occurring in the world of central banking and monetary policy. The European Central Bank (ECB) and the Bank of Canada (BoC) made reduced policy rates last week, stepping ahead of the Federal Reserve. Europe and Canada have also been fighting inflation, so why is the Fed still on hold? The primary reason for this divergence in policy is that economic growth has held up much better in the United States, and, with inflation still stubbornly high, the Fed has wisely refrained from easing monetary policy too soon. Federal Reserve officials would certainly like the opportunity to lower interest rates, but they will not be swayed until they gain sufficient confidence that inflation is on a sustainable path to their 2% target.

One reason the ECB may have been a bit anxious to ease is Germany’s trade surplus unexpectedly declined in its most recent reading. As readers may recall from last week’s letter, we referred to Germany as the “Industrial Engine” of the European Union. Easing normally leads to a devaluation of the home currency, which has a positive effect on a country’s trade balance.

Conclusion

Our opinion has not changed. The U.S. economy is in fine shape, except for stubbornly high inflation. The Federal Reserve would very much like to bring the Fed Funds Rate down, but, acting as a good custodian of the economy, they have waited for more evidence that disinflation will continue. The economic statistics quoted above should give the Fed ammunition to hold off on making any major moves during their FOMC meeting this week.

The EU continues to trail the United States in terms of economic growth, and, with growth faltering, the ECB elected to lower interest rates. The United Kingdom appears to be a long way from achieving a full economic recovery. The country seems to be in political disarray, which makes acting on some of the important economic decisions more challenging.

In Asia, India continues to impress. The country has always had volatile politics and has just completed a surprisingly close national election. It will be interesting to see if there are any policy changes or disruptions. China remains the laggard in the group, while Japan continues to improve.

Read pdf here.