Building Your Philanthropic Legacy: Charitable Remainder Trust

A Charitable Remainder Trust (“CRT”) is an irrevocable trust that provides income to the donor or other noncharitable beneficiaries for a specified period of time, with the remainder going to one or more charitable organizations upon termination of the trust. An important aspect of the CRT is that the trust itself is tax-exempt and the donor enjoys a tax deduction for the present value of the amount that will go to charity. However, income distributions to non-charitable beneficiaries are taxable.

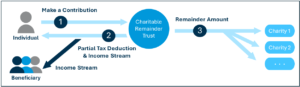

How it Works:

- The donor transfers appreciated assets (e.g., stocks, real estate) into the CRT.

- The trustee sells the assets tax-free and reinvests the proceeds to generate income.

- The trustee pays an annual income stream to the donor or other non-charitable beneficiaries for a set term (up to 20 years) or for life. The income can be a fixed annuity amount (CRAT) or a percentage of the trust’s value (CRUT). The amount of the income stream must be at least 5% but no more than 50% of the trust’s assets annually.

- The income paid to the beneficiary is taxable based on the tax character of that income (dividends, interest, rent, retirement distributions, capital gains, etc.).

- The donor receives an upfront charitable deduction based on the present value of the remainder interest that will eventually go to charity. This is computed based on a number of factors, including the length of the trust term (which is either a term of years or based on the life expectancy of the income beneficiaries), the payout rate, and prevailing interest rates.

- Under IRS rules, for each contribution of property to a CRT, the present value of the remainder interest that will eventually pass to charity must be at least 10% of the fair market value of the contributed property. Note that it is possible to add assets to a CRUT but not to a CRAT.

- When the trust term ends, the remaining assets are distributed to the designated charitable organization(s).

The key benefits of a CRT include deferring capital gains tax on the sale of appreciated assets, receiving an income stream (which can be for life), obtaining an immediate income tax deduction, reducing estate taxes, and facilitating a future charitable gift. However, there are a number of special rules that apply to CRTs, so careful attention to compliance is important.

The income from a charitable remainder trust is distributed in one of two ways:

- Charitable Remainder Annuity Trust (CRAT): The trust pays a fixed dollar amount each year to the noncharitable beneficiary regardless of the current value of the trust assets. This fixed annuity allows for potential growth in the trust principal since the annuity payments remain constant.

- Charitable Remainder Unitrust (CRUT): The trust pays a percentage of the trust assets to the non-charitable beneficiary each year. If the trust value increases over time, the amount paid to them will also increase proportionally.

The charitable remainder beneficiary can be any 501(c)(3) charitable organization such as a public charity (including a Donor-Advised Fund), as well as a private foundation or any qualified charity selected by the trustee or other designated person. IRS charitable deduction limitations apply.

CRTs are subject to various private foundation tax rules such as the prohibition on self-dealing. For example, it is not permissible for the grantor to borrow from the CRT.

The trustee of a CRT can be an individual, including the grantor, or a professional trustee, such as a trust company. We advise working with a professional trustee given the nuanced tax rules and specialized tax compliance.

The CRT is a sophisticated gift planning vehicle, and as with all such vehicles, professional counsel should be retained to fully analyze the effectiveness of a particular vehicle given a particular set of circumstances.

Read pdf here.