Weekly Market Insights 11.04.24

A Big Week in China—a Bigger One in the U.S.

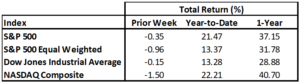

Financial Markets

United States equity markets were volatile this past week, and for good reason–the long-awaited presidential election will occur tomorrow. Volatility was the name of the game, and it was somewhat expected, although, as we and many other observers have pointed out, economic indicators suggest that the United States economy is doing very well. Alas, the looming election overrides all else.

Economics

We realize we may sound like a broken record, but it bears repeating—the United States economy is the strongest in the developed world. The unemployment rate held at 4.1% for the second month after peaking at 4.3% in July. This statistic is one of the most important we follow, as a strong number implies a continuation of consumer spending and can provide investors with a psychological boost. Payroll additions came in well below estimates, but the hurricanes and the ongoing Boeing labor strike are expected to have distorted the numbers. However, this pales to investors compared to the FOMC (Federal Open Market Committee) meeting on November 6 and 7.

Globally, there is an event that may challenge the U.S. election in capturing the attention of investors. That is the week-long meeting of China’s governing body. The emphasis, of course, will be on finance and economics. We anticipate more announcements about stimulus and some debt forgiveness. However, we believe it will take much more than that to solve China’s problems. One reason is the significant issues have been caused by poor economics, not just bad finance. Economics is far more challenging to change. We will follow it closely.

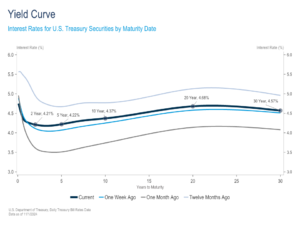

Yield Curve Update

Interest rates have risen since the Fed’s September rate cut, primarily driven by resilient economic growth, labor markets, and consumer spending. Fiscal policy concerns linked to the election outcome have added to interest rate pressures, which we will delve into later. Since the Fed’s September 18th meeting, the 2-year Treasury yield has risen by nearly 60 basis points, while the 10-year yield has risen by about 70. During the week, 2-year and 10-year yields increased by 10 and 14 basis points, respectively, while the curve steepened slightly to +0.18%.

Third-quarter GDP, PCE Deflator, and nonfarm payrolls highlighted last week’s economic releases, and all were generally consistent with the economic trends that have been in place for some time—surprisingly strong economic growth, continued disinflation, and gradual labor market cooling. While there was some volatility in the immediate aftermath of the reports, interest rates would eventually resume climbing higher in each case. The preliminary reading for the 3rd quarter real GDP came in at 2.8%, higher than consensus estimates, calling for a 2.6% increase. At the same time, the PCE Deflator indicated that inflation continues to decline towards the Fed’s 2% target. Friday’s employment report showed that just 12,000 jobs were added in October, significantly lower than estimates for 110,000 to 120,000 additions. While the hurricanes and the Boeing strike certainly contributed to the weak payroll number, there were also notable downward revisions to prior months, adding to the idea that the labor market is cooling. While some noise in the payroll report was expected, the weak report likely locks in at least one rate cut at next week’s Fed meeting. Fed Fund futures indicate as much, currently pricing in a 99% probability of a 25-basis point cut.

Renewed concerns over climbing government debt levels and persistent deficit spending have added to interest rate pressures. Regardless of who wins the White House, a shift in the near term towards fiscal austerity looks doubtful, and increased Treasury issuance will likely be required to fund this continued deficit spending. Absent an offsetting increase in demand, increased Treasury supply will pressure yields higher.

The Fed meeting will undoubtedly take a backseat to the election this week, but both events will have significant implications for the U.S. economy going forward. As always, we will keep readers updated on what develops.

Conclusion

Our conclusion today is not particularly satisfactory. The reason, of course, is the outcomes of the presidential race are unknowable. Elections aside, the United States economy is in very good shape and continues to be the best region globally to invest.

Read pdf here.