Weekly Market Insights 12.16.24

A Market in Confusion

Financial Markets

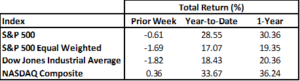

Equity markets moved lower in the first two days of trading last week but looked like they would turn higher after a Wednesday in-line Consumer Price Index (CPI) report. For a moment, life was great, but traders changed their tune, and markets once again moved into negative territory. Some tech-oriented mega-cap stocks continued to lead the parade, but it was insufficient to prop up the overall indices. Ultimately, the markets closed the week lower.

There are many potential reasons why traders turned on the market midweek. Perhaps it was profit-taking, or investors took a closer look at valuations. As the incoming president’s appointees and plans come together, traders and investors may be lowering their risk profiles in light of the new information. This is not a garden variety change of administration, so it must weigh heavily on investors’ minds. As readers will see, the potential changes coming from the new administration make both economic and market analysis more challenging. This week, one thing is sure—all eyes will be focused on the Federal Reserve!

Economics

A changing administration can have significant consequences for any economy, particularly one that has the potential to be more consequential than most. We don’t have enough data to feel comfortable making strong predictions at this point, but what we can do is take what we have been told by the president-elect and report what standard economic analysis would suggest. Lower tax rates will help to boost consumption but could also exert upward pressure on inflation. Lowering tax rates without offsetting fiscal adjustments could significantly add to the already high federal deficit, resulting in additional inflationary pressures and a weaker dollar. The results of any serious economic analysis of the United States would have the analyst marvel a bit about the apparent strength and soundness of the U.S. economy relative to other developed economies. Are there problems lurking in the future? Yes—inflation, a large and growing federal deficit, and the deteriorating financial health of certain social programs, but we are aware of them, and they can be addressed with a bit of wisdom.

We have often written about technological developments that hold great promise for the future. Of course, we are talking about quantum computing and artificial intelligence. Continued advancements in these areas could solve some of the problems we highlighted. Both areas are vital to progress. They are contributors to what we call Total Factor Productivity (TFP), and historically, significant increases in TFP have led to substantial increases in economic well-being (the First Industrial Revolution, for example). Happily, we don’t have to be AI experts to feel comfortable saying this. Increases in Total Factor Productivity make each hour of human work more productive than it was before. In the case of economic advancement, productivity is the name of the game.

The E.U. remains in a slow recovery. The ECB lowered interest rates again this past week, which should provide additional support. However, it seems reasonable not to expect a full recovery until Germany, Europe’s economic engine, begins to advance more rapidly.

China continues to suffer economically. Unfortunately, the country is not suffering from a simple cyclical downturn but rather a flawed economic system. A strong domestic economy can almost act as an automatic stabilizer. That is what is missing.

Conclusion

These days, it is challenging to come to satisfactory conclusions. The United States economy remains the strongest in the developed world. Investors are seemingly cautious about some of the changes that could come with the new administration, but we remember when President-elect Trump first came into office. The changes were not so dramatic. It’s not easy to enact widescale changes in a country as large and diverse as the United States. One thing we feel confident in saying is don’t panic.

Read pdf here.