An Update on Planning in a Low Interest Rate Environment

Planning Strategies

“Out of adversity comes opportunity.”

─ Benjamin Franklin

While low interest rates continue to put pressure on income oriented portfolios, the recent market correction and low rates have created some unique estate planning opportunities. Last summer, we released a piece entitled “Planning in a Low Interest Rate Environment.” All of the topics covered there are still very much alive today and the advice is still relevant. But, we are writing again on this topic to emphasize a few key points in the wake the recent market volatility, which has been triggered by multiple factors all hitting at once: the spread of the coronavirus, energy prices falling, the Chinese economy slowing, election year politics and the uncertainty it causes, and high stock market valuations.

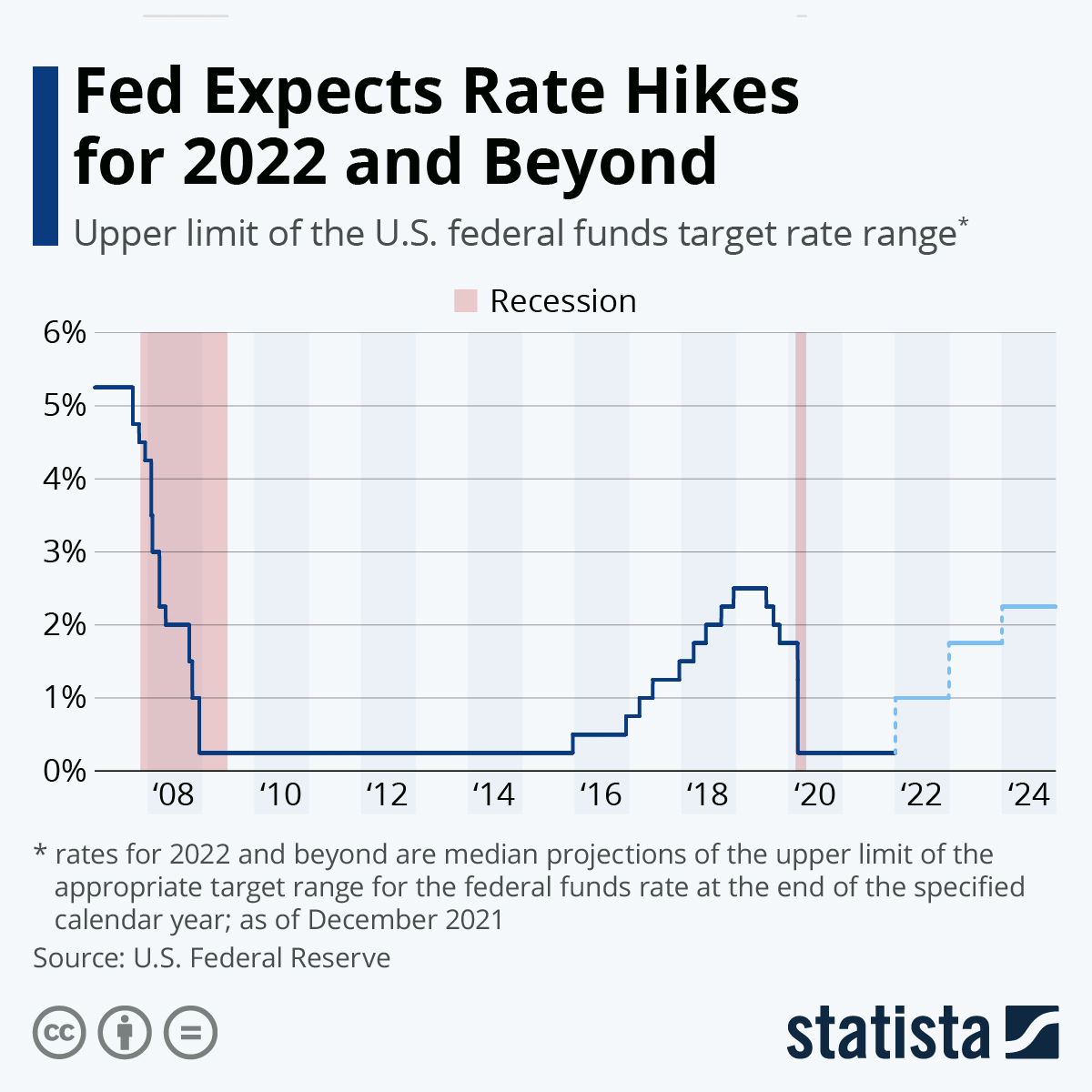

On March 3, 2020, Jerome Powell, the Federal Reserve Chairman, announced that the Fed is cutting interest rates by 50 basis points (one half of one percent) to combat economic woes caused by the coronavirus outbreak. This move will have a ripple effect across all types of financial instruments and products as well as certain estate planning techniques. Accordingly, we believe our thoughts from last summer bear repeating. The current market lends itself to some rare planning opportunities.

Here are a few things we believe our clients should be considering in this environment:

- Refinance your mortgage. Very low interest rates present a great opportunity for anyone with a mortgage to refinance and lock in a new lower rate for up to 30 years. It is not difficult to find banks offering loans at less than 4% per annum on 30-year home loans.

- Consider making low-interest loans to your children. The IRS sets the rate on loans between family members at the Applicable Federal Rate (or “AFR”). This rate changes from month to month but can be fixed for the life of the loan. Right now (March 2020), the mid-term AFR on loans between 3 and 9 years is only 1.53%. The recent interest rate cut will likely force the IRS to lower the AFR next month (April 2020) to something close to an all-time low.

Market conditions combined with low interest rates make the GRAT particularly compelling now.

- Make tax-efficient gifts using GRATs. As we said last summer, Grantor Retained Annuity Trusts (GRATs) are trusts that allow the grantor to transfer the future appreciation over an IRS hurdle rate to their heirs. For March 2020, the hurdle rate (also known as the “Section 7520 rate”) is 1.8%. We expect the rate to drop in April 2020 as well. The way these trusts work is that the grantor makes a gift of property that is expected to appreciate over time. The grantor retains an annuity interest in the trust equal to the fair market value of the gift. This results in a zero net gift with no gift tax due. However, as long as the assets appreciate at a rate more than the hurdle rate, the excess appreciation passes on to the next beneficiary, most likely your children or trusts for their benefit. As you can imagine, very low interest rates make this strategy attractive, especially in an environment with rising equity valuations. However, even in times such as these, creating a GRAT can be a good idea. Market volatility can be the friend of the GRAT. While downside volatility can cause the strategy to fail, upside volatility, especially around the time the annuity payment is due, is a good thing. Moreover, under current tax rules, appreciation can be locked in by the grantor swapping in cash for the appreciated security in the trust. Further, GRATS done in the past can be refreshed by substituting cash for an underperforming stock and then re-GRAT-ing the shares using today’s values and rate.

- Use your estate and gift tax exemption this year. As of January 1, 2020, the Federal estate and gift tax exemption was increased to $11.58 million per person by way of an inflation adjustment. The exemption today is the highest it has ever been. Under the Tax Cuts and Jobs Act of 2017, the high exemption level is set to last through December 31, 2025. After that date, it will reset to the pre- 2018 level, which is $5 million plus inflation adjustments. However, the exemption could be reduced as soon as 2021 if Congress and the President choose to do so. A number of Democratic candidates have called for lowering the estate tax exemption and for higher estate tax rates. Because of the political uncertainty, we advise anyone with wealth over $20 million to consider their planning options now before the exemption goes away. As the year progresses, we expect the urgency around executing an estate plan will only increase and that lawyers and financial advisors will be overwhelmed with requests and demands on their time. The exemption also can be levered using valuation discounting techniques. A 30% discount is not unheard of with proper planning.

- Lower valuations create gifting opportunities. The recent drop in equity markets created an opportunity for anyone thinking about making a gift of a portion of their securities portfolio to children or a trust for their benefit. The valuation drop essentially means that donors can gift more shares or use up less of their exemption than they would have last December. These market conditions combined with low interest rates also make the GRAT particularly compelling now.

How can we help? If any of these ideas interest you, contact your Portfolio Manager or Client Advisor at 1919 Investment Counsel. We would be glad to walk your through the strategies and help you develop a plan that makes sense for you and your family.

WARWICK M. CARTER, JR

Principal, Senior Wealth Advisor

Warwick M. Carter, Jr. is a Principal at 1919 Investment Counsel based in New York. As a Senior Wealth Advisor, his primary focus is generational wealth planning for high net worth individuals and families. He also advises on philanthropic planning. When giving advice, Warwick takes a comprehensive approach to assessing all aspects of a client’s tax, financial and family situation. Warwick works closely with Portfolio Managers and Client Advisors in all of our offices to integrate wealth strategies with a client’s investments. He regularly meets with outside advisors to devise appropriate solutions that will help grow wealth in a tax-aware way over the long term.

Warwick is a graduate of Denison University and the Columbus School of Law at The Catholic University of America. He also holds a master’s in taxation from Georgetown University. He is admitted to the bar in New York and the District of Columbia. Warwick is also a member of the New York State Bar Association and the Society of Trust and Estate Practitioners (STEP).

Email address: wcarter@1919ic.com