Electric Utilities Set to Benefit from EV-Driven Grid Investment

Wildfire-induced blackouts in California and more recent events in Texas, where unpreparedness curtailed energy supplies, highlight the vulnerabilities of the US power grid. Over the next two decades, the need for grid investment will be substantial; driven, in part, by the economic impact of outages, but even more by the electrification of the transportation sector and continued transition to renewable sources of energy. Multiple factors are coalescing to accelerate the transition from internal combustion (IC) to electric vehicles (EVs) over the next decade, which will necessitate much-needed investment in US infrastructure. In this piece, we share our research on electrification and the role of electric utilities with insights on technologies and trends set to transform mobility industries and the public sector globally.

WHY NOW?

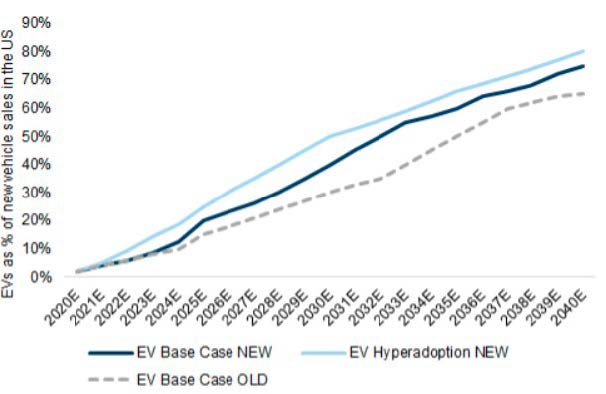

When investors think of EVs, model lineups, price, and battery-range anxiety are often front of mind. In 2020, there were about 25 battery EV models available in the US. Through 2022, another 30-40 models are set to be introduced.1 Most forecasts suggest that by 2030, EVs could account for 30% of light-duty vehicles sold. In many cases, EV list prices are already at parity with IC counterparts, with any premium for EVs likely to erode as battery prices decline. Federal, state, and local support is growing and President Biden’s jobs plan could provide an additional spark.

Collectively, these factors will accelerate EV adoption through the next decade, but adoption comes with a significant side effect.

US EV Adoption

Source:Goldman Sachs

THE GRID

In order to upgrade the world’s infrastructure to accommodate widespread usage of EVs, a sizeable amount of capital will be needed to prepare the electrical grid. “Behind-the-meter” electric transmission and distribution (T&D) investment could be required for decades. In addition to establishing a public charging network and incorporating a greater amount of renewable energy to provide zero-carbon EV power, grid upgrades will be needed to accommodate load growth, congestion, and capacity needs. Outlays will correspond to the pace of adoption and stand to reach several hundred billion dollars. For a deep dive into these investments and associated considerations, please see 1919’s companion piece, Grid Infrastructure Gets a Spark from Vehicle Electrification.

ELECTRIFICATION

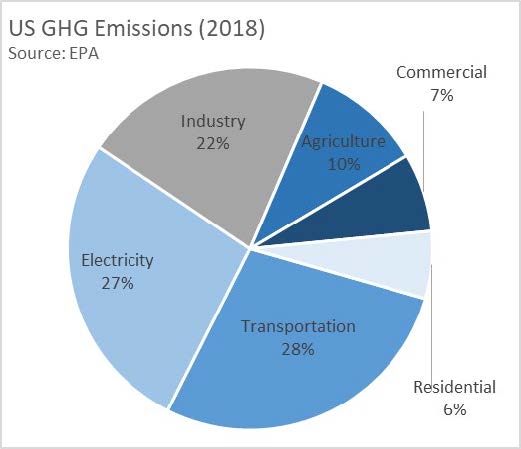

EVs stand to be a meaningful contributor to the energy transition movement, a theme with durability, which has previously been highlighted at 1919 Investment Counsel Electric Vehicles Disrupting the Automotive Industry. Transportation is now the largest contributor to the nation’s greenhouse gas emissions with light-duty vehicles and trucks accounting for 60% and 23% of this output, respectively.2 Consumers, corporations (especially fleet operators), and original producers of auto components (OEMs) are coalescing around adoption of EVs. The inflection point may only be a few years away as a greater number of passenger EVs are released and carriers begin to incorporate more EVs into their fleets.3 In addition, renewable energy sources now account for ~20% of power generation and are expected to top 40% by 2050 according to the Energy Information Administration.

One goal under the President’s jobs plan is to accelerate energy transition and fully de-carbonize the power sector by 2035. That would require additional and significant investment in generation and T&D capacity and run in parallel to EV preparations.

ELECTRIC UTILITIES

Serving as gatekeepers to the power grid, electric utilities already invest about $55 billion annually in T&D assets plus another $45 billion in generation, and will play a central role in enabling vehicle electrification.4 Utilities are regulated entities; they can earn an authorized return on equity and must maintain a specified capital structure. Most are able to grow regulated capital between 5%-7% per annum.

Preparing the grid for EVs over the next 20 years would elevate overall capital spending by 50%+ annually to more than 10% on a straight-line basis. Practically, this is a tall order because state Public Service Commissions (PSC) would need to increase return thresholds, in all likelihood leading to higher customer bills. Rather, utilities may reprioritize projects. Capital expenditures are somewhat fungible and the same return is earned regardless of asset investment so EV infrastructure could be emphasized at the expense of other projects. Instead of raising growth rates, upward pressure on the rate base extends the runway for years to come, such that EPS growth remains firmly in the mid-single-digit area.

That said, not all electric utilities benefit equally. As a starting point, those utilities operating in regions where adoption is occurring fastest and where state PSCs are most supportive, have the best prospects. Additionally, most states have yet to greenlight a make-ready EV strategy. Time is on their side for now, but rising EV adoption and broader de-carbonization efforts will require action in the near future. As an investable theme, certain companies align with electrification improvements more than others. NextEra Energy (NEE), a renewable energy leader and operator of Florida Power & Light, and Eversource Energy (ES), a unique “wires only” utility in New England, both appear well positioned to benefit. Additionally, electrical equipment company, Eaton Plc. (ETN) will provide many of the building blocks utilities require to enable an EV transition and will directly participate in the EV and charging markets.

CONCLUSION

Ultimately, federal, state, and local governments, as well as corporations, auto component manufacturers, and vehicle owners, largely have aligned on EV adoption. This transition will require a wave of capital investment for decades to come and lengthen the duration for electric utilities to grow rates at a healthy mid-single-digit level. Of course, that growth may be uneven at times while other crosscurrents could surface. For example, higher interest rates would make utilities less attractive versus risk-free alternatives. Also, the possibility of idiosyncratic factors such as regulated changes to capital structure or return thresholds could undermine growth. Yet, these seem insignificant when balanced with the essential role electric utilities will play not only in EV transition, but also in de-carbonizing the power generation industry. At 1919 Investment Counsel we continue to monitor the evolution of the electrification trend for investment opportunities for our clients’ portfolios.

ERIC G. THOMPSON, CFA

Principal, Equity Research Analyst

Eric is a Vice President at 1919 Investment Counsel, LLC. His primary responsibility is as an Equity Research Analyst covering the Industrial and Utility Sectors. Eric has over 16 years of experience as a Research Analyst with 15 of those years following the Industrial Sector. Prior to joining the firm, Eric was a Senior Equity Analyst covering Indus- trial and Healthcare companies at Wilmington Trust Investment Advisors. Prior to this, he was an Associate Analyst with Legg Mason.

Eric is a CFA charterholder and received an M.B.A. from Cornell University’s Johnson Graduate School of Manage- ment. He earned a B.S. in Finance from Towson University.

1 https://evadoption.com/future-evs/

2 Source: EPA

3 UPS has agreed to purchase 10,000 EVs from Arrival. https://arrival.com/news/ups-invests-in-arrival-and-orders-10000-gen- eration-2-electric-vehicles

4 https://www.eia.gov/todayinenergy/detail.php?id=47316, https://www.eia.gov/todayinenergy/detail.php?id=48136