Investment Review & Outlook – October 2022

Key Takeaways

We believe that the Fed is committed to driving current inflation down to target levels (2 to 2.5%) and wants to make sure inflation will not flare up again due to premature easing, avoiding a repeat of the late 1960s and 1970s.

We believe that the Fed is committed to driving current inflation down to target levels (2 to 2.5%) and wants to make sure inflation will not flare up again due to premature easing, avoiding a repeat of the late 1960s and 1970s.- The consequence of Fed actions is a high probability of recession in 2023 which will increase unemployment and weaken demand. Longer- term low inflation is good for consumers, especially those on a fixed income. For investors, low inflation and low interest rates support stock, bond, and real estate valuations.

- At this point, we do not expect a severe recession. Many inflationary factors, like commodities, have peaked, and pandemic-related stimuli are winding down. Employment remains healthy and the economic slowdown may moderate wage pressures by reducing job openings versus generating high unemployment.

The Economy

By technical definition, a recession is two consecutive quarters of negative GDP growth. Based on that parameter, the US economy was in a recession for the first half of 2022, which we believe will turn into a broader recession in 2023, but expect will be moderate in severity due to the economy’s overall current strength.

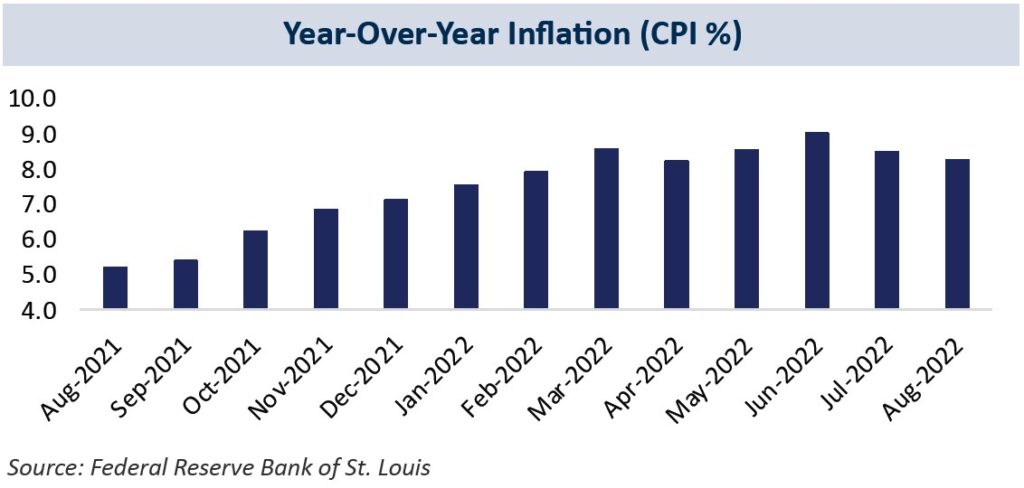

Inflation’s Trajectory and the Fed’s Aggressive Response

Inflation continues to be a challenge, rising quickly to reach an annual rate of 8.3% as of August 31, 2022. While the price of gasoline dropped sharply from its record high in June, other costs have increased, including the costs of essentials such as groceries and electricity.

With five consecutive interest rate hikes this year, the Fed is seeking to quell rising inflation by slowing growth and orchestrating a “soft landing.” While the Fed’s dual mandate is to keep prices stable and to maximize employment, it is clear that price stability is now its primary concern, even if rising unemployment is the result. Fed Chairman Powell has stated that the Fed will raise the fed funds rate and keep it elevated until inflation subsides to a level near its 2% target. With this in mind, the Fed raised the fed funds rate rate by three-quarters of a percentage point to a range of 3.00% to 3.25% on September 21, 2022, and signaled more increases to come in 2022 and potentially 2023.

“The FOMC is strongly resolved to bring inflation down to 2%,

and we will keep at it until the job is done.”

Fed Chairman Powell

Factoring in the Lag Effect

There typically is a lag between rate hikes and the resulting impact on the economy. Historically this lag has been in the range of 12 to 18 months. More recently, due to increased Fed transparency and speed of communication, among other factors, this lag time has compressed to 6 to 12 months. We are now at the beginning of the period wherein interest rate hikes, which started about six months ago, will begin to be felt across the economy. The most important factor to monitor will be the impact of rising rates on inflation, wages, and employment data.

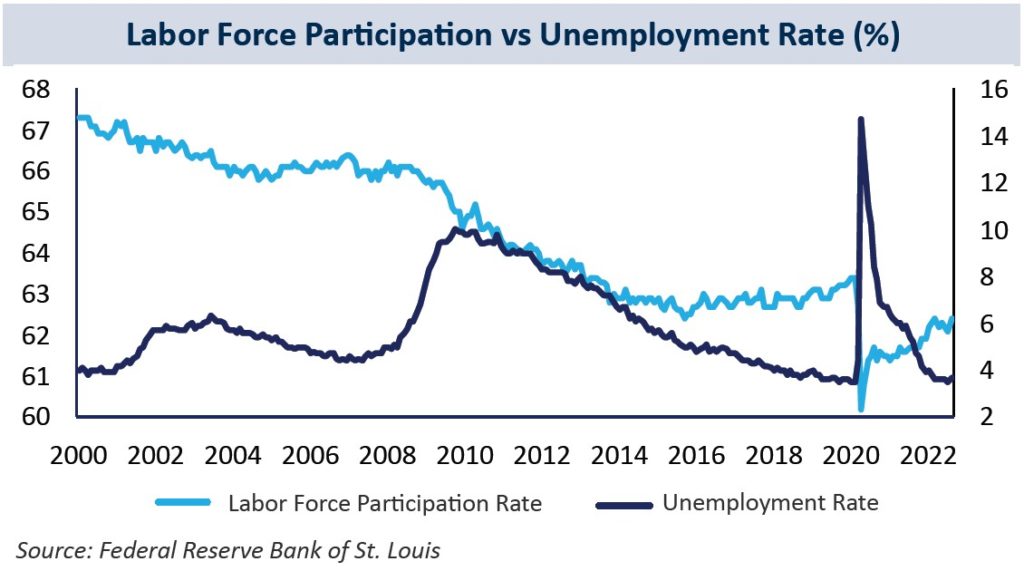

Employment Levels and Labor Participation

Significant interest rate increases to bring down inflation and slow an overheated economy still flush with pandemic-related stimulus may ultimately have a negative impact on employment levels. The latest August unemployment claims total was 213,000, an exceptionally low number signifying a very strong labor market.

In a rising rate environment, with a strong possibility of a recession, we expect an increase in unemployment as consumer demand slows and businesses cut costs by cutting jobs. This is part of the rationale for a soft landing: that higher rates will reduce job openings, putting downward pressure on wages without increasing unemployment significantly.

US labor supply and participation rates are ongoing concerns since tightness in the work force has driven up wages as businesses try to attract talent, which fuels inflationary pressures.

- The US labor force participation rate was 62.4% as of August 31, 2022, versus a pre-pandemic level of 63.4% and a low 60.2% in April of 2020.

- The labor force participation rate is the percentage of the population age 16 years and older that is either working or actively looking for work.

- According to the S. Bureau of Labor, the number of job openings decreased to 10.1 million as of the last business day of August 2022. This still represents about 1.7 job openings for every unemployed person.

A prolonged labor shortage has been driven by several issues, including pandemic-related early retirements, the impact of long COVID, retiring baby boomers, and lower immigration rates for both skilled and unskilled labor. While recessionary pressures may result in short-term higher unemployment levels and increased available labor supply, to some degree US labor shortages may be a multi-decade challenge.

The US Consumer and Household Wealth Considerations

Consumer spending is the main driver of the US economy and the US consumer has been challenged by rising inflation, high energy prices, and volatility in both the equity and fixed income markets. Retailers are seeing a pullback in overall consumer spending across regions, categories, consumer demographics, and income levels. However, credit card debt has spiked again, with debt levels higher than they were in March of 2020 as the pandemic took hold. During the pandemic, many consumers flush with stimulus dollars paid down debt.

Conversely, personal US savings rates, which soared to levels as high as 34% in April 2020 during the height of the pandemic, have fallen to 5% as of July 2022. The decline in the savings rate and spike in credit card debt is not a good sign when unemployment is poised to rise. In addition, US household wealth fell by more than $6.2 trillion in the first half of 2022, from a record $150 trillion at the end of 2021. A $7.7 trillion decline in stock market value in the first half of the year outstripped a $1.4 trillion gain in real estate values. The glow of the wealth effect felt by many consumers as investment portfolios and housing values soared in the pandemic has diminished.

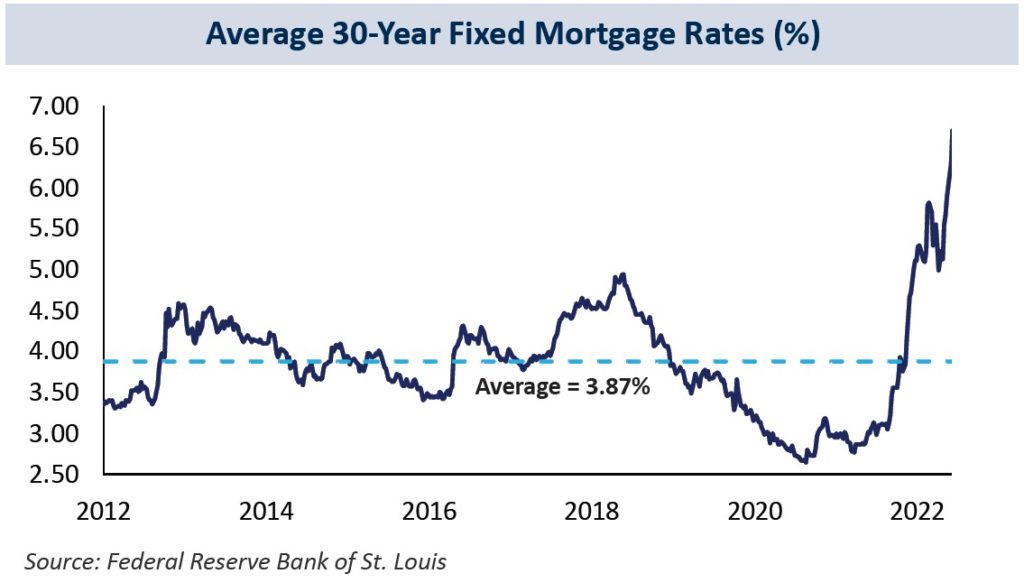

A Slowing Housing Market

Housing represents approximately 30% of the overall Consumer Price Index (CPI including energy and food prices). While we have seen home prices and rents skyrocket this year, demand is beginning to decline as mortgage rates approach 7%. The impact of higher rates is a decrease in affordability. The days of multiple bids and frenzied home buying are subsiding. The difference between the interest rate on existing mortgages and the current mortgage rate for new loans is the widest it has been since 2008. Many homeowners may choose to stay put rather than finance a new home purchase at a higher rate, constraining supply.

With constrained supply across the US, we expect housing may plateau at these relatively elevated prices. The average sales price of a home in the US was $525,000 as of June 2022, an increase of 40% in just two years.

A slowdown in home sales due to higher mortgage rates ultimately will have an adverse effect on other housing-related areas. For example, spending on home furnishings, paint, and other home-related products should fall. Consequently, a decline in housing sales has tended to reduce overall economic activity with a lag of approximately six months. However, the short-term economic disruption caused by higher rates may be a necessary and painful consequence of heading off inflation.

The Equity Market

A Bearish Equity Market

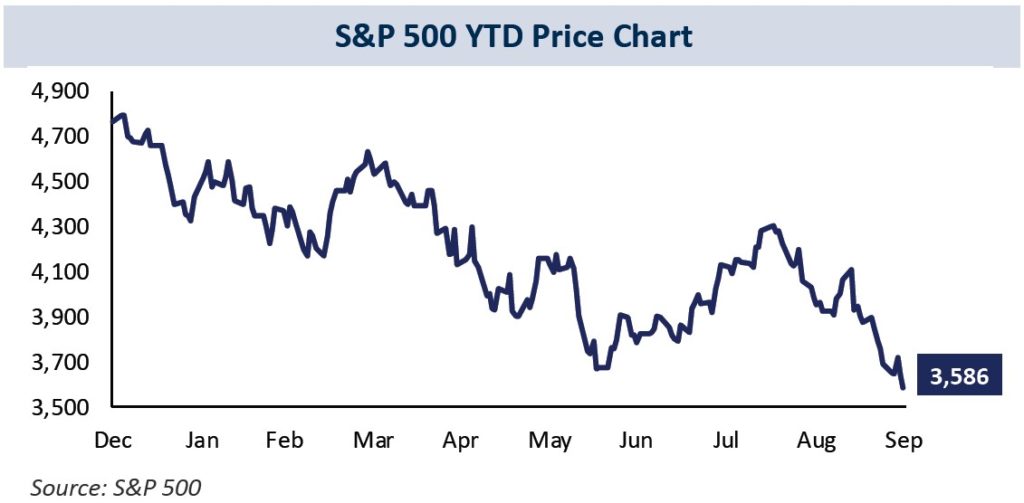

The stock market’s 21% drop in the first half of 2022 (as represented by the S&P 500 Index) was mostly valuation compression due to higher interest rates and inflation. A recession and recessionary earnings were not really priced into the market, but the market’s decline in September seems to be the beginning of this discounting process. History tells us the stock market corrects before a recession and then recovers before the economy bottoms. It is hard to know when economic activity bottoms and thus hard to time the market. Given the unknowns, focusing on the stocks of high-quality companies is critical.

The equity market continued to be roiled by volatility in Q3, punctuated by significant market drawdowns. However, overall corporate profitability remains strong, and fundamentals remain attractive. Stock valuations have reset at more attractive levels which eventually will present more compelling buying opportunities. Higher interest rates have driven stock market valuations to more reasonable levels assuming inflation continues to trend towards the Fed target. The forward P/E at the end of 2021 was at 21x and now is at 16x.

Yet investors’ concerns about rising interest rates, rampant inflation, and the potential impact of a prolonged recession on future corporate profitability may remain elevated until the Fed appears closer to ending this tightening cycle and may serve as significant headwinds to equity market performance.

Stock investors have not fully discounted recessionary earnings. Margin pressure and interest rate-generated demand destruction will depress corporate earnings. At this point, an 11% drop in S&P 500 earnings would be consistent with a moderate recession, possibly resulting in a 5 to 10% market decline from current levels.

Investment Considerations

Defensive stock positioning remains paramount with a focus on high- quality companies with attributes such as strong balance sheets, high returns on capital, and stable sales growth. A company’s ability to maintain its revenues, protect its margins, and grow earnings despite a potential economic slowdown also is important to evaluate. Additionally, the results of the midterm election in November may significantly impact the legislative policy agenda which, in turn, may have a meaningful impact on select sectors and industries.

Focusing on Investment Goals and not Market Gyrations

It is important to note that a bear market often plays out over the course of a year or more. It may take some time to see an equity market recovery. Patience will be critical, as will focusing on one’s long-term investment strategy in keeping with investment goals, risk tolerance, and time horizon, rather than making radical changes based on short-term market events.

The Fixed Income Market

Bonds Become Interesting

The dramatic swings that have occurred in the fixed income market over a short time period warrant attention. The Fed’s trajectory of five consecutive fed funds rate hikes has rapidly propelled the economy into a new rate environment after years of easy monetary policy. The Fed is committed to doing whatever it takes to reduce inflation closer to 2%, believing that the harm from persistent inflation outweighs the negative impact of hawkish policy on economic growth and employment.

While yields have increased, particularly on the short end of what is now an inverted yield curve, bond prices (which move inversely to yields) have plummeted. In an atypical occurrence, there has been a decline in the bond market at the same time the equity market has pulled back. Investors expect equities to be volatile, but bond market volatility has been an unsettling event for many investors.

To compound these issues, fears of a recession may lead to increased sensitivity regarding fixed income default risk. We believe investing in high- quality fixed income securities with minimal default risk is of the utmost importance. A focus on procuring attractive yields without taking on undue duration risk, while maintaining liquidity, allows for elevating the portfolio yield to levels not seen in over a decade.

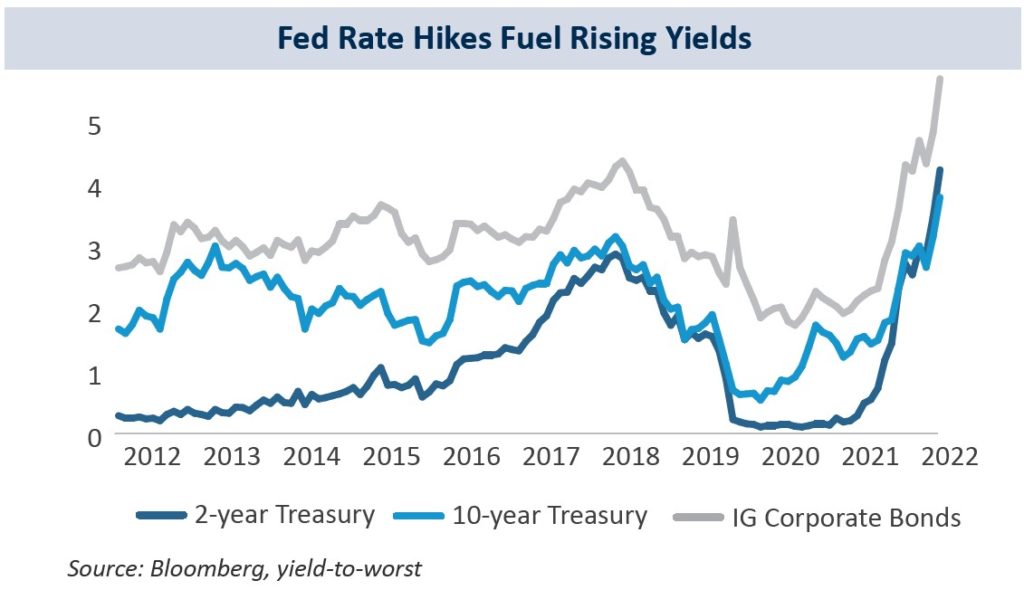

Treasury Yield Trajectory

While we anticipate higher interest rates over the next three to six months, with an inverted yield curve, investors in long-term bonds may already be pricing in a decline in economic activity and a moderation of inflation. The 10-year Treasury bond yield reached 3.94%, its highest level since 2010, before ending the quarter at 3.83%. The Fed ramped up quantitative tightening in September, seeking to cut $90 billion in assets from its balance sheet. This resulted in downward pressure on longer-term bond prices as the largest buyer of Treasuries withdrew from the market, thereby fostering higher rates further along the yield curve to lure other buyers to step in.

The 2-year Treasury yield reached 4.34% before closing the period at 4.28% following the Fed’s third “unusually large” 75 basis point hike and is trading at levels not seen since 2007. Short-term yields are higher than long-term yields, reflecting investors’ anticipation that higher rates will lead to slowing economic growth and a dampening of inflation. Surging Treasury yields, producing a risk-free return for investors, have had a negative impact on the stock market, as future earnings of riskier assets such as equities become less attractive on a relative basis.

An Update on Corporate Bonds

While corporate bond issuance has been surprisingly strong following the Labor Day holiday, we expect issuance to dampen as we enter late fall. We anticipate that 2022 issuance will end up quite comparable to that of 2021, with total annual corporate bond issuance in the $1.0-$1.2 trillion range.

As rates continue to rise, we anticipate decent corporate bond opportunities along the yield curve. From a credit risk perspective, corporate bonds that are backed by strong company balance sheets and sound credit fundamentals can weather a recession. Given global economic and geopolitical uncertainty, we expect volatility in the corporate bond market to persist and believe liquidity will be an important consideration for the foreseeable future.

A Municipal Bond Update

Municipal bond issuance and supply are limited. State and local governments still enjoy ample stimulus-related and income-tax-related cash reserves in the form of “rainy day funds,” so they have not had to rely on the bond market for much of their funding needs. The vast majority of these reserves remain unspent and even unallocated, which will provide a buffer in unexpected economic or public health setbacks.

Municipal credit quality is strong, with upgrades occurring for several states. However, if rates continue to rise and remain at elevated levels, municipalities may come to market with new issuance in anticipation of rates trending even higher for longer. Refinances have halted as municipalities are not interested in, nor do they need refinancing at this time.

Staying The Course During A Challenging Time

It has been a challenging year for investors from both a fixed income and equity market perspective, and we believe it will continue to be so for the remainder of 2022 and potentially into 2023. As we work with clients, the following considerations are top of mind:

- Concerns about inflation and a recession remain front and center.

- We expect market volatility to persist until inflation’s upward trajectory is reversed due to the Fed’s aggressive interest rate stance.

- We are focused on maintaining liquidity, income generation, and long- term growth potential in keeping with specific investment goals.

At 1919 Investment Counsel, LLC we will help you navigate this challenging time with ongoing, timely advice and a commitment to helping you achieve your investment goals.

Read PDF here.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

All information herein is as of September 30, 2022 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202.

©2022, 1919 Investment Counsel, LLC.