Investment Review & Outlook – April 2024

Key Takeaways

US economic growth has proved remarkably resilient during the first quarter of the year, primarily due to low unemployment giving consumers the confidence to keep spending.

US economic growth has proved remarkably resilient during the first quarter of the year, primarily due to low unemployment giving consumers the confidence to keep spending.- The strength in the economy has moderated the decline in the inflation rate, keeping the Fed on hold so far this year, and dampening investor expectations for a meaningful number of rate cuts in 2024.

- The equity market rally has broadened somewhat beyond the narrow advance of 2023, with positive stock performance from more sectors and companies than had been the case recently. High interest rates have provided bond investors with attractive income opportunities.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

Economic Review

The US economy continues to do well, with GDP growth of 2.3% through February, slightly above our expectation for 2024 GDP growth of approximately 2%. The strong labor market has played a significant role in keeping the economy moving in the right direction. However, the unemployment rate rose slightly to 3.9% in February, versus 3.7% in January. This is the first increase in the unemployment rate in four months, and it now sits at its highest level of the last two years.

The Fed interest rate increases in 2022-2023 have had less of a negative impact on jobs and the economy than might have been expected, causing investors to embrace the idea of a soft landing, whereby the Fed is successful in cooling inflation without causing unemployment to rise. We believe the possibility of a mild recession still exists, as the effect of higher rates continues to ripple through the economy, and any slowdown in the labor market will directly weigh on consumer demand. In addition, many corporations issued debt during the recent period of historically-low rates. If they have to come back to the bond market to issue debt at higher current rates, it increases their costs, which may lower their demand for additional labor.

Unemployment, Job Creation, & Labor Force Participation

The unemployment rate increase has been countered by the large number of jobs created, more than 275,000 in February, significantly above the 200,000 that were expected. Additionally, the labor force participation rate, which measures the percentage of the population that is either working or actively looking for work, has increased to 62.5%, from its 2020 pandemic low of 60.1%. While not yet reaching the pre-pandemic rate of 63.3%, the participation rate is trending upward, which is a positive indicator.

The labor force participation rate for those 25-to-54 is 83.5%, back to levels we have not seen since the early 2000s, which is a very encouraging sign. Yet it also is important to consider that during the pandemic, a significant number of workers over 55 took early retirement and have not returned to the workforce, further fueling the labor shortage in the US. Amid pandemic-related stimulus, and the wealth effect created by the rising stock market and increased home values, members within this cohort saw their net worth appreciate significantly. However, these actions have led to shortfalls in some specialized areas of the labor market, such as seasoned healthcare professionals.

THE LABOR FORCE PARTICIPATION RATE FOR THOSE 25-TO-54 IS 83.5%, BACK TO LEVELS WE HAVE NOT SEEN SINCE THE EARLY 2000S, WHICH IS A VERY ENCOURAGING SIGN.

Wage Growth & Consumer Spending

Wage growth remains robust, and so does productivity. As a result, unit labor costs are not increasing, which helps dampen inflation. However, this benefit tends to be offset somewhat by minimum wage increases occurring in 50% of the US states.

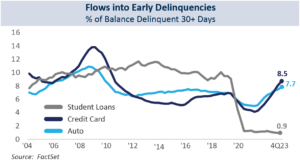

Retail sales also are an important economic indicator in the consumer-driven US economy. While January retail sales declined 1.1%, they bounced back a bit in February. Consumer sentiment has been steady since January, registering at 76.5 for the preliminary March estimate, which is almost 25% above the November 2023 reading. One concern is that much of consumer spending is paid for with credit cards. Despite low unemployment, US delinquency rates on credit cards and auto loans are the highest in more than a decade. Normally, delinquencies do not start to rise until unemployment does. Current high interest rates make it difficult for borrowers to pay down their balances, an issue that will become even more significant if unemployment spikes.

Inflation – Still Higher than 2%

As of the end of February, the inflation rate was 3.2% year-over-year. Our long-term outlook for inflation is higher than the Fed target of 2%, for the following reasons:

- The labor force remains constrained due to demographic dynamics, immigration issues, and a mismatch of available labor skills versus job requirements.

- Heightened geopolitical risk, increased regulations, and potential import tariffs are inflationary factors, as the resultant increase in the cost of goods is passed on to the consumer.

- The housing market, a key driver of inflation, continues to suffer from a lack of inventory. Baby Boomers account for nearly 38% of homeowners nationwide but represent only 21% of the population. This housing shortfall will last until inventory improves, keeping home prices quite high. In combination with higher mortgage rates, this makes homeownership unattainable for many buyers.

However, we believe inflation below 3%, as well as increased productivity from advancements in automation, robotics, and artificial intelligence, provides a positive environment for growth in the economy and in the equity markets nonetheless.

Are There Rate Cuts Ahead?

Interest rates may have peaked, but we do not see them falling as quickly as investors anticipated at the start of the year. We anticipate 2 to 3 Fed rate cuts in 2024, starting in the middle to latter half of the year, depending upon ongoing inflation moderation that trends closer to the Fed’s target rate.

After its recent FOMC (Federal Open Market Committee) meeting in March the Fed stated:

“In support of its goals, the Committee decided to maintain

the target range for the federal funds rate at 5.25 to 5.50 percent.

In considering any adjustments to the target range for the federal funds rate,

the Committee will carefully assess incoming data, the evolving outlook, and

the balance of risks. The Committee does not expect it will be appropriate

to reduce the target range until it has gained greater confidence

that inflation is moving sustainably toward 2 percent.”

-FOMC Press Release 3/20/24.

Fed Chairman Powell said that it was too soon to say whether the recent trajectory of lower inflation had stalled or reversed, and that more data would be needed before confirming rate cuts are warranted. However, Fed officials have maintained their projection that they will lower the federal funds rate by three-quarters of a percentage point to a range of 4.5% to 4.75% by year-end.

Election Year & Geopolitical Uncertainties

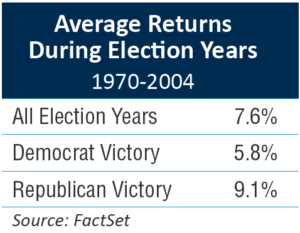

Both domestic politics and geopolitical dynamics have the potential to disrupt the US economy and markets this year. In a US presidential  election year, rhetoric from both parties will ramp up, with the potential for markets to react to headline risk in this increasingly polarized political landscape. However, based on historical data going back 56 years, the stock market tends to rise in presidential election years by 7.6%, on average.

election year, rhetoric from both parties will ramp up, with the potential for markets to react to headline risk in this increasingly polarized political landscape. However, based on historical data going back 56 years, the stock market tends to rise in presidential election years by 7.6%, on average.

Geopolitical dynamics, including the wars in Ukraine and the Middle East, add to the level of uncertainty globally. In addition to the heightened risk to the people and places in these areas of conflict, a rise in geopolitical tension tends to be inflationary as it impacts trade, shipping costs, the prices of key natural resources, and results in less economic and political cooperation among major nations.

Equity Market Highlights

A Broadening of Equity Market Opportunities

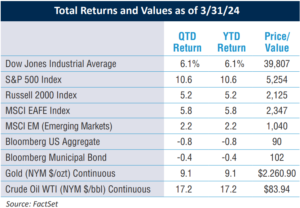

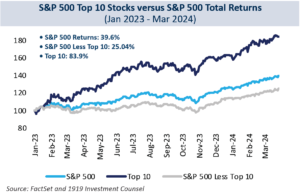

It was a strong end to the first quarter in the equity markets with both the S&P 500 and Dow Jones Industrial Average closing the quarter on record highs, and the S&P 500 up 10% year-to-date. The euphoria surrounding AI’s potential impact on productivity and future growth continues to drive investor interest. However, in 2024, stock performance has broadened beyond the very small number of stocks that led the charge in 2023, fueled by earnings growth and a resilient economy.

While the “Magnificent Seven” companies still demonstrate attractive above- average earnings growth, their performance versus the broader market may not be as pronounced in 2024, relative to last year. The concentrated investor enthusiasm appears to be broadening out into the rest of market as investors seek out companies with lower valuations that can benefit from continued economic growth, and the potential productivity enhancements offered by the adoption of generative AI tools.

The markets tend to do well when short-term interest rates are cut by the Fed, although we think much of the benefit for stocks has been pulled forward by investors. Smaller companies, in particular, benefit when short-term rates decline, as they typically rely more on debt, and a reduction in borrowing costs is impactful. Small-cap companies have been out of favor over the past several years, leaving them relatively inexpensive and potentially attractive for investors going forward.

Equity returns are very dependent on interest rates and monetary policy expectations. So while we believe the economy may slow in the next few months, the impact on stocks may well be positive. For each piece of data that shows a weakening economy, investors will draw a conclusion about a greater likelihood of additional rate cuts, which are beneficial to equity returns, provided the market has not already priced in such cuts.

Equity Market Bubble?

With the equity market reaching numerous new highs in 2024, investors may wonder whether they should be concerned about a market bubble. In 2023, only a small handful of stocks outperformed the rest on the promise of AI, and one could draw similarities to the tech bubble of 1998-1999. Yet during that late 90s period, many of the dot-com companies involved in the equity run-up had no earnings. This is not the situation today, and earnings growth continues for the technology and communications services companies that have been leading the equity market charge.

Fixed Income Market Highlights

The Fed Holds Rates Steady

The Fed slightly upgraded its growth and inflation forecasts (to 2.1% from 1.4%, and 2.6% from 2.4%, respectively) but still anticipates lowering rates by year-end. The Fed’s March statement was nearly identical to the last one, with Chairman Powell stating that risks between growth and inflation were balanced, while the strong inflation readings in January and February were bumps in the road to the broader disinflation story (with January’s strong inflation numbers likely related to seasonal factors).

The dot plot, a chart that indicates short-term rate projections for the FOMC, has 10 members anticipating three cuts this year, and 9 expecting two or fewer. At 1919, we are in the latter camp given strong inflation readings of late and the fact that a quarter of the year has passed with the Fed in no hurry to act.

Treasury Response

10-year Treasuries remained stuck in the 4.25% range after the Fed meeting, reinforcing the point that longer maturities are governed more by inflation expectations and supply/demand than by Fed policy. The short end of the yield curve rallied somewhat, but Treasury bills still yield approximately 5% or more, meaning the more tepid pace of easing is already priced in, consistent with our views.

Attractive Fixed Income Opportunities Continue

Despite the higher interest rate environment versus recent experience, we remain conservative with regards to credit quality and prefer shorter-maturity positioning within portfolios. The economy and inflation continue to show resilience and the yield curve remains inverted, meaning shorter-maturity bonds yield more than longer-duration, riskier debt. We do not see a catalyst for a meaningful drop in yields in the near term. Therefore, we continue to favor a more defensive portfolio, particularly as we move into the election season, and will look for opportunities to lock in yields on longer-maturity bonds when we are convinced inflation remains in a decelerating trend.

Issuance Insights

After only one quarter, corporate bond issuance has been at record- breaking levels and is expected to be robust throughout the first half of 2024. Corporate bond yields in the 5.5% to 6.0% range are an attractive proposition for short- and intermediate-term investors.

In the municipal bond market, supply also has increased. Because 2024 is the last year in which federal infrastructure money can be allocated for a project, we expect to see more municipalities return to the capital markets, issuing municipal bonds to meet future project-funding needs.

Increased issuance should result in better pricing, driving yields higher, providing greater opportunities for tax-sensitive municipal bond investors.

Closing Thoughts

The Fed’s multi-year effort to control inflation continues, and we expect the higher interest rate environment to persist for some time. We do expect the Fed to gradually reduce short-term interest rates at some point this year, but this will depend on the Fed’s confidence in a sustainably slowing economy.

Regardless, we expect ample growth opportunities among a wider breadth of high-quality companies. We also expect yields in the fixed income markets to remain relatively attractive, providing welcome income opportunities. As always, we look forward to helping you meet your income and growth objectives throughout 2024 and beyond.

Read pdf here.

All information herein is as of March 31, 2024 unless otherwise stated. The information provided here is

for general informational purposes only and should not be considered an individualized recommendation

or personalized investment advice. Past performance is not a guarantee or indicator of future results.

No part of this material may be reproduced in any form, or referred to in any other publication, without

the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains

statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated,

are based on information available to 1919 as of such date, and are subject to change, without notice,

based on market and other conditions. There is no guarantee that the trends discussed herein will

continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information

contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange

Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the

United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202.

©2024, 1919 Investment Counsel, LLC. MM-00000980