Investment Review & Outlook – January 2024

Key Takeaways

- Investors have priced in an optimistic soft-landing scenario, but our expectation is for a slowdown or mild recession in early 2024 as the economy continues to feel the effects of two years of sharp Fed tightening.

- Despite slowing economic growth, lower short-term interest rates and an acceleration in corporate profit growth have the potential to provide moderate returns for equities during the year.

- Current fixed-income yields in the face of declining inflation offer attractive real returns for investors seeking income.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

Review

At the beginning of the year, investors had every reason to think that the speed and magnitude of recent Fed rate increases would slow the economy enough to bring about a recession. Adding to the negative outlook was a regional banking crisis that flared up in March as a result of higher rates. However, what actually happened was that inflation began to fall, employment stayed strong, and consumers continued to spend, keeping the economy humming along, capped by robust 4.9% annualized GDP growth in the third quarter. By December, dovish comments by Fed Chair Powell indicating that the Fed most likely would start cutting rates seemed to increase the likelihood of a soft landing, whereby the economy slows enough to tame inflation without bringing about a recession. Stock and bond investors welcomed both the economic data and the change in tone by the Fed, igniting a late-year rally in both asset classes.

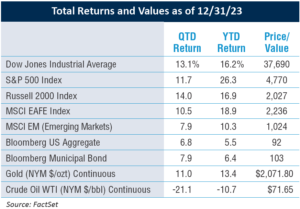

For the quarter, the S&P 500 returned 11.7%. Bonds, represented by the Bloomberg Aggregate Bond Index, returned 6.8%, fueled by a decline in interest rates. The regularly-quoted market-weighted S&P 500 Index returned 26.3% for the year, versus 13.9% for the equal-weighted index, the widest spread between the two since the tech bubble of 2000.

We remain concerned that the rosy scenario priced in by investors for a soft landing, with a growing economy and reasonably healthy corporate profit growth, leaves very little room for disappointment, especially at current valuations.

The Fed’s More Dovish Approach & The Lag Effect

Chairman Powell was expected to be fairly hawkish in his comments following the December meeting, pushing back on recent investor exuberance that surfaced in November. We anticipated that the Fed would wait until inflation is somewhat closer to 2% before talking about cutting rates. Instead, comments that economic conditions were improving enough that three rate cuts were on the horizon were a welcome surprise for equity and bond investors, resulting in a short-term broad-based rally.

There typically is a time lag from the initiation of a rate hike to when the maximum impact on the economy is felt. This lag seems to have shortened from the typical 12 to 18 months, so it is difficult to gauge how long any headwinds might persist and to what extent economic activity still may slow even if rates have peaked. According to the Philadelphia Fed, the median forecast for 2024 GDP is 1.7%. We are on the low side of the forecast. Despite Powell’s recent optimistic comments, the last rate increase was as recent as July, not all that long ago. In fact, the perception that interest rates will decline in 2024 may have a slowing effect on the economy if consumers and corporations delay spending until rates actually drop.

Fed Remains Data Driven

The Fed remains very data dependent and policy responses will continue to vary based on future economic indicators. So while the Fed has communicated three potential rate cuts in 2024 based on current trends, its forecasts have historically not been accurate. In fact, recent retail sales suggest an economy with enough strength that it would be premature to ease interest rates any time soon. In addition, payroll data have been strong, weekly initial jobless claims are near 50-year lows, while the unemployment rate is only 3.7%.

THE FED REMAINS VERY DATA DEPENDENT AND POLICY RESPONSES WILL CONTINUE TO VARY BASED ON FUTURE ECONOMIC INDICATORS.

Tracking Inflation Trends

Core CPI (Consumer Price Index), as measured on a year-over-year basis, remains around 4%, twice the Fed’s 2% target. However, the Fed is more focused on core PCE (Personal Consumption Expenditures), which makes it easier to see the underlying inflation trend by excluding two categories, food and energy, where prices tend to swing more frequently and dramatically. Core PCE for 2023 was 3.2%, closer to the Fed’s target, rising only 1.9% over the last 6 months, on an annualized basis. The encouraging PCE data provides solid evidence that inflation has been tamed and allows the Fed to focus on cutting rates in the near future.

The post-pandemic repair of the supply chain seems to have fully occurred and is an important part of resolving inflationary pressures. Maybe inflation was transitory after all. While the cumulative effects of goods inflation are abating, prices for services are not likely to revert to previous levels.

There still is a labor shortage, which puts persistent upward pressure on inflation and remains a challenge to the predominately service-based US economy. The number of job openings has declined but still exceeds the supply of available workers, causing upward pressure on wages. Even with surging immigration, the workforce continues to shrink as more baby boomers retire, and this demographic shift appears likely to be a headwind for labor supply for some time.

Fortunately, an uptick in productivity has provided some relief. Increased productivity allows more economic activity with the same number of workers, and recent enthusiasm over the promise of productivity gains from artificial intelligence is encouraging.

Consumers & Small Businesses Are Challenged

Additional evidence of a slowdown can be seen by lower-income consumers who continue to be challenged by inflationary pressures and tightened credit conditions. Many in this demographic have used most, if not all, of the savings they built up during the pandemic. Although offset by some wage increases, their purchasing power continues to be eroded by inflationary pressure. Increased credit card usage and evidence of rising credit card delinquencies have resulted, which might be expected after the onset of a recession, not when the labor market is strong. Many borrowers were able to take advantage of locking in ultra-low rates available a few years ago for expenses such as mortgages, but credit card borrowers feel the immediate and significant impact of recent rate increases.

In addition, the disproportionate pressure on lower-income consumers is indicated by companies reporting that consumers continue to trade down in brands, looking for lower pricing and discounts. Tighter bank lending standards, implemented after the banking crisis in the first quarter of 2023, also have been a headwind for small business investment, making it more difficult to build inventory, hire new people, and expand.

Some Global Context

From a global perspective, the US has weathered this pandemic-related economic storm better than Europe. Led by Germany, much of Europe is in a recession while the UK also is experiencing slower growth.

In the world’s second largest economy, China’s post-pandemic economic resurgence has not been as significant as expected and headwinds continue. China is experiencing deflationary pressures but has yet to produce a solution to address them, and credit issues are negatively impacting China’s real estate industry. As an important trading partner for Europe, China’s lackluster growth has contributed to Europe’s economic woes.

As We Enter An Election Year

With 2024 being an election year, an incumbent administration typically does everything possible to ensure consumers are optimistic as they head to the polling booths. For example, if there is economic weakness in the first half of 2024, the Administration can reactivate the Employee Retention Credit (ERC) without congressional approval in order to stimulate a slowing economy.

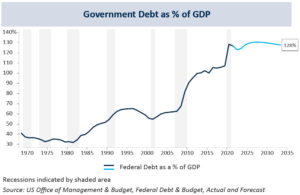

Another factor that is certain to be part of the political dialogue is US government debt-service levels. While lower rates will help reduce interest outlays, the sheer magnitude of the debt and budget deficit, as a percentage of GDP is an issue for the US economy. In fact, it has been forecast that the $1 trillion in interest payments on government debt in 2024 will exceed the entire US defense budget by approximately $200 billion.

Given the US strength and stability in the global economy, the dollar’s role as the world’s reserve currency, and the confidence in the Fed, the US has been able to borrow at lower rates and spend more than would otherwise be the case. Any loss of global confidence in the Fed’s credibility and the dollar as a reserve currency is a negative tipping point to avoid.

The Equity Market

The Year Of The Magnificent Seven

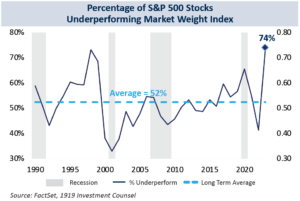

Looking back at 2023, the headline phenomenon for the stock market was the performance of the “Magnificent Seven” stocks (NVIDIA, Meta, Amazon. com, Microsoft, Apple, Alphabet, and Tesla) and the concentration of market capitalization that resulted. Investor exuberance was compounded by the enthusiasm surrounding ChatGPT, artificial intelligence (AI), and the potential of machine learning, with many of these companies leading the AI charge. At a point during the year, these 7 stocks comprised a whopping 29.1% of the S&P 500.

Consequently, this very small group of stocks had an outsized impact on the performance of the market-weighted S&P 500 Index versus the other 493 components. The index rose 26.3% as of year-end 2023, with a valuation close to 20x earnings. In comparison, the equal-weighted index, which values all 500 components of the index equally, was up only 13.9% for 2023, and at a more reasonable valuation close to 16x earnings. This data illustrated the outsize impact of those seven large-cap companies on the performance of the S&P 500.

A Broader Market Now Beckons

By year-end, it was encouraging to see the market beginning to broaden from such a narrow group, with the equal-weight index beginning to close the massive performance gap relative to the market-weight index. If lower rates come to pass, the broader equity market will benefit investors, although valuations are not particularly compelling at this time as investors already have priced in lower rates. It is interesting to note that the last time the cap-weighted S&P 500 Index substantially outperformed the equal-weighted index was in 1999-2000, leading up to the bursting of the tech bubble. During this period, the cap-weighted index outperformed by 15%. However, the trend reversed in 8 of the next 10 years, with a cumulative underperformance for the cap-weighted index of 96%. While the largest companies in the S&P 500 may still be great companies and should offer reasonable returns over time, if history is a guide the chances of continued outperformance of the cap-weighted index are low.

Slower Growth May Be A Headwind For Equities

The current forecast for growth in S&P 500 earnings for 2024 is 10%. While growth in earnings and lower interest rates may be supportive of equity valuations, slower economic growth will be a headwind. As a result, we expect positive but somewhat subdued equity returns in 2024.

However, concerns regarding rapidly rising inflation have abated, lessening the probability of equity valuations dropping significantly as they did in the inflation-ridden 1970s. Fortunately, the Fed has been able to curtail protracted inflation, with recent data trending more toward the 2% to 3% range, without even more significant rate increases, suggesting a benefit for stocks.

The Fixed Income Market

Attractive Real Yields

There has been a rapid increase in rates over the past 18 months. The Fed’s terminal rate appears to have been reached, and cuts in short-term rates are expected in 2024. Similar to the response in the equity market, bond investors cheered the Fed’s December comments by buying bonds and driving the 10-year Treasury yield down to 3.9%, significantly below the 5% level it touched as recently as October (bond prices and yields move in opposite directions). We expect the 10-year Treasury yield to remain in the 4% range and investment-grade corporate bonds in the 5% range, by the end of the year, where the potential decline in yields from benign inflation data may be offset by the boost in Treasury issuance along with the increased cost of financing the high level of government debt. Unlike short-term rates that are more easily impacted by Fed policy, long-term rates are determined by bond investors, who often are influenced by long-term inflation expectations, and supply considerations.

THE FED’S TERMINAL RATE APPEARS TO HAVE BEEN REACHED, AND CUTS IN SHORT-TERM RATES ARE EXPECTED IN 2024.

Investment-Grade Corporate Bonds Considerations

Overall, corporate bond yields offer attractive income potential. Again, with yields offering 5% or higher, investment-grade bonds should keep portfolios well ahead of inflation without a significant increase in credit risk, especially in light of the expectation for a mild recession if any. Corporate supply should be lower in 2024, as many companies pulled forward issuance ahead of the prospects of an economic slowdown. Without a flood of supply overwhelming the market, the yield differential between corporate bonds and comparable-maturity Treasuries should remain somewhat stable and not widen dramatically, which would cause price volatility.

A Word About Municipal Bonds

In the municipal bond market, issuance was light throughout 2023, resulting in a rally of 6.4%. By the end of December, the muni rally appeared to be overdone, and munis were rich to Treasuries once again. Given that the yield curve remains inverted, with longer rates below short-term ones, it does not seem warranted to aggressively extend muni bond duration. Instead, we will look for a muni bond pullback to offer investors a more attractive entry point, which probably will coincide with a pickup in muni bond issuance. However, this potential for increased issuance is not guaranteed because the infrastructure stimulus dollars already available to states and local governments have yet to be fully utilized or even allocated in many instances.

Credit Quality Deterioration?

Credit quality may have peaked for many states, as reserves boosted by significant federal pandemic aid and Rainy Day Funds have declined. Nonetheless, most states are in good enough shape to weather any mild recession. However, isolated credit quality concerns are emerging. For example, California is facing a significant budget shortfall. While the state has a large Rainy Day Fund and is rated Aa2, the state has quickly gone from having a huge budget surplus to a sizeable deficit. The state is highly levered to personal income tax revenues, and the extent of realized capital gains can have a substantial impact on total tax collection amounts. We are paying close attention to rapidly changing scenarios such as those underway in California and remain committed to investing in high-quality municipal bonds.

Keeping a Long-Term Perspective

Following 2022’s sharp and broad-based declines in equity and bond prices, returns in 2023 have provided a welcome relief for investors. Keeping a long-term perspective and focusing on individual needs are the keys to successful investing. While we have laid out our economic and market forecasts, it is important to remember that using forecasts in order to time the market to make investment decisions is difficult at best, even for the Fed. Time in the market with high-quality securities, not market timing, is the recipe for building wealth.

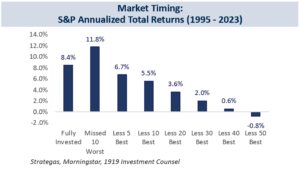

The chart below shows that if one misses just 50 of the best days in the stock market over a 28-year period, it reduces long-term returns significantly. The best solution is to employ an asset allocation strategy based on an investor’s specific needs, focusing on adequate liquidity and volatility buffers, with a longer-term commitment to equity assets for growth.

We remain committed to helping you achieve your investment goals and wish you and your loved ones a happy, healthy, and prosperous New Year.

Read pdf here.

All information herein is as of December 31, 2023 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize. This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed. 1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202.

©2024, 1919 Investment Counsel, LLC. MM-00000828