Investment Review & Outlook – October 2023

Key Takeaways

Despite the tight monetary policy of the last year and a half, the labor market, and therefore the US consumer, have remained strong. This has pushed out the timeframe for a recession, but we do not believe it has removed the likelihood of one.

Despite the tight monetary policy of the last year and a half, the labor market, and therefore the US consumer, have remained strong. This has pushed out the timeframe for a recession, but we do not believe it has removed the likelihood of one.- Hawkish guidance by the Federal Reserve indicating that rates might stay higher for longer than expected resulted in a decline in stocks during the quarter. Higher yields cause investors to reassess equity valuations and increase competition for investment dollars.

- Recent inflation data has shown a slight moderation, which should be well received by the Fed and may bring a halt to further interest rate increases.

There is no guarantee that forecasts or estimates discussed herein will materialize, or that trends discussed herein will continue.

The Economy

The US consumer has been resilient, and the economy less interest rate sensitive than expected in the current tight monetary policy environment. The significant increase in both yields and borrowing costs appear to be working their way through the economy but have yet to result in the expected economic slowdown.

While consumers have been challenged by persistent inflation, spending continues, helped by strength in the labor market. Rising energy prices impact consumer budgets, but rent and housing prices recently have stabilized. Higher rates definitely have had an impact on cooling the housing market, but not as much as one might expect. Homeowners fortunate enough to have locked into lower mortgage rates a few years ago are unwilling to sell, keeping demand for homes higher than inventory for sale.

Climbing Consumer Credit Balances

However, where we are seeing cracks is in the area of consumer credit card debt. Much of recent consumer spending has been credit card fueled as post-pandemic savings have dwindled. Record card balances, surpassing $1 trillion, and an upward trend in credit card and auto loan delinquencies have been reported. Credit card delinquencies have reached pre-pandemic levels, and there has been a 35% annual increase in lower-income Americans taking out payday loans.

Growing evidence suggests that many consumers may be financially stretched, as borrowing costs have reached their highest levels in 22 years. This is somewhat worrisome, as consumers drive most economic activity in the US, and pressure on their finances normally comes after an increase in unemployment, which has not yet materialized.

A Recession Or Soft Landing In 2024?

Several storm clouds are forming that lead us to conclude that a mild recession remains the likely outcome, although pushed out to 2024. While the rate of inflation has moderated, it is not yet low enough for the Fed to begin loosening its policy stance. Additionally, we expect that the resumption of student loan repayments, higher credit card balances and delinquencies, and increases in unemployment as rate hikes make their way through the economy will trigger a slowdown. The possibility of an extended auto sector shutdown will be a further drag on the economy.

The Fed’s Ongoing Battle With Inflation

At its recent Federal Open Market Committee meeting, the Fed held rates steady, after 11 consecutive hikes since March 2022, guided by “solid” economic growth and slowing job growth, noting that tighter credit conditions are likely to weigh on hiring as well as inflation. In August, inflation rose by an annual rate of 3.7% amid higher gasoline prices, while core numbers, which exclude volatile fuel and food costs, rose 4.3% from a year ago. This is a slight decrease in inflation as compared with six months ago.

It will be challenging for the Fed to reach its 2% inflation goal, necessitating another potential rate increase later this year, depending on economic conditions. “Broadly, stronger economic activity means we have to do more with rates,” Chairman Powell has stated, adding that lower inflation during the past few months allowed the bank to pause tightening in order to assess the ongoing impact of prior rate hikes. While the Fed’s summary of economic projections has two rate cuts slated for next year, we do not anticipate any easing will occur without evidence of a meaningful economic slowdown.

Lower Inflation, Good For Investors

In the long run, however, lower inflation is good for both consumers and investors. Low inflation supports higher consumer spending as well as higher stock valuations. If inflation continues to decrease, the real interest rate (the rate an investor receives after factoring in inflation) will be positive for the first time in a while, providing attractive returns for investors.

The Equity Market

Catch-Up To Magnificent Seven Leadership

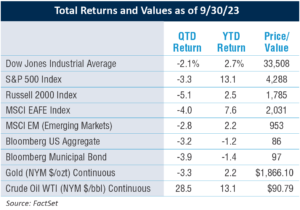

While the equity market, as measured by the S&P 500 Index, is up 13.1% in 2023, much of this return had been driven by only a select few mega-cap stocks, dubbed the “Magnificent Seven” (NVIDIA, Meta, Amazon.com, Microsoft, Apple, Alphabet, and Tesla), and was partly fueled by an AI euphoria that took hold during the summer. The market cap of these seven stocks has ballooned to where they now comprise 28% of the index, skewing returns for the whole index.

As a result, the S&P 500, which is a market-cap-weighted index, was up 13.1% through September 30th. A more realistic depiction of the broader market’s performance is gained by looking at all 500 components of the index equally, for which the year-to-date return is only 1.8%. However, the tide seems to have turned, as the performance of the market-cap versus the equal- weighted index has been fairly similar since the end of June.

The performance of these mega-cap stocks also was driven by investor hope that not only would the Fed stop hiking rates, but also that it might start to lower them. Growth stocks tend to do well when rates are low or declining. This hope for lower rates resulted in an expansion of the price/ earnings multiple, reversing the compression trend that occurred in 2022. Multiple expansion occurs when investors become more optimistic about a stock’s prospects, resulting in the stock price rising faster than any improvement in company earnings.

Emerging From An Earnings Recession

Even though there has not yet been a true economic recession in 2023, corporations have experienced an earnings recession with negative earnings growth since the start of the year, causing equities to become somewhat richly valued. However, earnings estimates for the 4th quarter and 2024 are starting to rise, which may serve to support the equity market’s performance next year despite a potentially slowing economy.

Investor Awareness & Sector Opportunity

In the first and second quarters of 2023, investors managed to look past the rising Fed Funds rate, fully expecting a soft landing. However, as the third quarter progressed, investors became resigned to the fact that rates may not be cut as quickly and significantly as expected, further confirmed by Fed Chair Powell at his recent press conference. Coupled with the prospects for a slowing economy, the result has been a dampening effect on stock valuations.

Across particular sectors of the stock market, healthcare stocks are an attractive investable area in terms of valuation, risk, and reward. While Medicare and procedural hospital and device issues have hampered sector performance, we believe resolution of these issues will occur in the near future. There are opportunities in this sector that provide a compelling balance of reasonable valuations and attractive growth potential.

Capital Costs Are Always On Our Radar

Higher interest rates mean companies have to pay more for debt capital, putting pressure on company cash flows and margins from the higher cost of borrowing. Companies that are highly reliant on a need to issue new debt to finance projects or to refinance existing debt will find their cost of capital has increased significantly.

The Fixed Income Market

In concert with the Fed rate hikes, attractive interest rates in the fixed income market are providing investors with a potential alternative to stocks for the first time in several years. For income-oriented investors, compelling fixed- income opportunities abound, with corporate bond and US Treasury yields above 5%. The trend in corporate bond issuance over the last few years was the growth of BBB issuance, with many companies taking advantage of a low interest rate environment to issue debt. We have also seen some upgrades in bond ratings as many companies took the opportunity to focus on strengthening their balance sheets. Recently, the percentage of BBB obligations in the Bloomberg Aggregate Bond Index has dropped below 50%, a reflection of improving corporate balance sheet health. Stronger corporate balance sheets support our thesis for a mild recession.

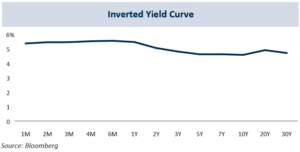

Protracted Inverted Yield Curve, Harbinger Of Recession?

As we have written previously, an inversion of the yield curve, where longer- dated bonds yield less than shorter-dated maturities, tends to be a precursor to a recession. The yield curve has now been inverted for over a year without a recession, surpassing the record for the number of days of the last protracted yield curve inversion. This might make an investor think that the inverted yield curve signal is not relevant in this economy. However, it may be notable that the prior record ended in May of 2007, ultimately being followed by a deep recession.

Municipal Bond Perspectives

Unlike the Treasury yield curve, which is heavily inverted on the short end, the municipal bond yield curve is flat out to 10 years and then steepens dramatically. This is partly due to the fact that the municipal bond market is highly fragmented, with many regional nuances and differences in supply availability. For example, California and New York issuance is limited, while Texas offers abundant supply. As the pandemic government stimulus dwindles, we expect to see a greater demand for municipal bond issuance to fund projects, creating more investment opportunities for municipal bond investors.

In terms of credit quality, we believe we have seen the high-water mark, with the government funding many municipal balance sheets and projects. While most municipalities are in great financial shape post-pandemic, due to the tailwinds of fiscal stimulus and ample rainy day funds, we expect credit quality to deteriorate as the impact of higher inflation, higher rates, and growing recessionary pressures take hold.

Final Thoughts

The equity market has rebounded somewhat from the declines of the previous year, but competition from higher yields is beginning to weigh on valuations as investors adjust expectations for the economic outlook and earnings growth. Attractive yield opportunities are available across the fixed income spectrum, which has been advantageous for income-oriented investors.

While inflationary and increasing recessionary pressures may lead to volatile markets as we close out this year and enter 2024, a diversified portfolio that includes a selection of securities based on an investor’s goals, risk tolerance, and time horizon is still the recipe for positive long-term investment outcomes. In addition, ample liquidity for short-term cash flow needs will allow investors to navigate this period of market adjustment, until the stage is set for a broader market advance in 2024.

From managing cash flow to generating income and growing wealth, 1919 Investment Counsel is committed to helping clients reach their goals by investing in the equity of successful companies by investing in the equity of successful companies and the fixed-income securities of creditworthy borrowers, always with an eye on managing risk.

Read pdf here.

All information herein is as of June 30, 2023 unless otherwise stated. The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Past performance is not a guarantee or indicator of future results. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of 1919 Investment Counsel, LLC (“1919”). This material contains statements of opinion and belief. Any views expressed herein are those of 1919 as of the date indicated, are based on information available to 1919 as of such date, and are subject to change, without notice, based on market and other conditions. There is no guarantee that the trends discussed herein will continue, or that forward-looking statements and forecasts will materialize.

This material has not been reviewed or endorsed by regulatory agencies. Third party information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

1919 Investment Counsel, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission. 1919 Investment Counsel, LLC, a subsidiary of Stifel Financial Corp., is a trademark in the United States. 1919 Investment Counsel, LLC, One South Street, Suite 2500, Baltimore, MD 21202.

©2023, 1919 Investment Counsel, LLC. MM-00000716