Sustainable Finance: Fixed Income Meets Responsible Investing

We continue our series on Environmental, Social and Governance (ESG) related investment topics with this short primer on Sustainable Finance instruments. In prior reports, we have reviewed the meaning of ESG (ESG 101), as well as discussed specific ESG topics such as climate change (Investing and Climate Change). Additionally, we wrote about the energy transition movement, a theme with durability that has been previously highlighted at 1919 Investment Counsel (Electric Utilities).

At 1919, we support the growing field of Sustainable Finance through investments in impactful debt instruments such as Green, Social, and Sustainability bonds (GSS bonds).

WHAT IS SUSTAINABLE FINANCE?

There are several kinds of sustainable financial products. Within the Fixed Income sector, we will focus on GSS Bonds. GSS Bonds are a specific type of bond in which a country, municipality, or corporate entity, issues a bond and dedicates the proceeds of the bond to pre-defined eligible projects. Green Bonds were first created in 2007, but the market truly gained traction in 2013, when the International Finance Corp (IFC) issued a $1 billion Green Bond, drawing attention to the market.1 As of mid-2021, there has been over $1.2 trillion in cumulative Green Bond issuance worldwide.2 Issuances of Social Bonds and Sustainability Bonds, while still not as common as Green Bonds, have also grown. During 2020 alone, $408 billion of Social and Sustainability Bonds were issued, resulting in a doubling of the GSS market size over 2019.

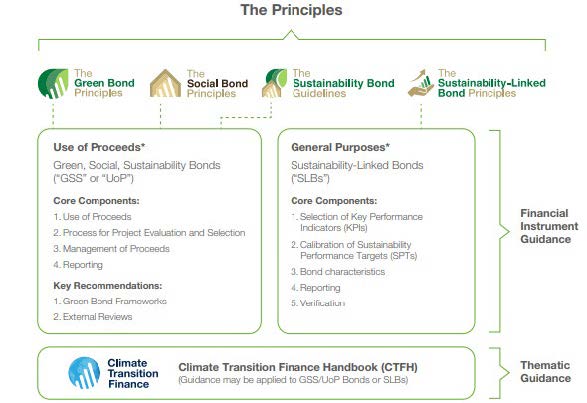

The International Capital Market Association (ICMA) recently updated its guidance for issuers of GSS Bonds, known as the Green Bond Principles (GBP), the Social Bond Principles (SBP), and the Sustainability Bond Guidelines (SBG).3 As a market-driven initiative, these Principles have been developed and adjusted over time with the input of prominent market participants, including investors, issuers, and underwriters. Within the voluntary guidelines, there is a focus on transparency and disclosure. Aligning with the Principles’ processes can help issuers build trust among investors and other market participants.4

HOW ARE GREEN, SOCIAL, AND SUSTAINABILITY BONDS SIMILAR TO OTHER BONDS?

A GSS Bond is legally pari passu (i.e., on equal footing) to other bonds of the same rank in an entity’s capital structure. The benefit of this structure is that it does not create a legally separate class of bonds; rather GSS Bonds are priced and traded in the same way as any regular bond from that issuer. This framework gives investors comfort that they are not losing any legal standing or protection from buying the impact-oriented bond. Further, it means GSS Bonds are not a separate asset class. At 1919, our Credit Research analysts review every bond, including GSS Bonds, that we purchase to ensure it fits our standard credit investment criteria; ratings, maturity, tranche size, and liquidity. Our Responsible Investing analysts review the issuer’s approach to sustainability as it relates to the specific GSS Bond. The GSS Bonds that are purchased are integrated into our clients’ fixed income portfolios as part of our process to create impactful portfolios for our clients.

HOW ARE GREEN, SOCIAL, AND SUSTAINABILITY BONDS DIFFERENT?

Unlike regular corporate bonds that raise fungible capital for use in any aspect of the entity’s finance needs, the typical GSS Bond is structured as a “Use of Proceeds” bond; however, it can also be structured as a Project or Revenue Bond. The issuer earmarks the bond proceeds to be used for specific projects. For example, a utility company may issue a Green Bond to finance the construction of wind or solar power projects (e.g., Avangrid Inc., 3.800% due 06-01-29). A REIT may issue a Green Bond to upgrade its properties to receive LEED-certification (e.g., Host Hotels & Resorts LP, 3.375% due 12-15-29). A bank may issue a Social Bond to support the company’s financing of affordable housing assets (e.g., Citigroup Inc., 0.776% due 10-30-24). A Sustainability Bond has proceeds designated to a mix of green or environmentally friendly and socially beneficial projects.

The guidelines for GSS Bonds include categories of activities that may be considered eligible projects. For example, the Green Bond Principles (GBP) lists the following, in no specific order:

- Renewable energy

- Energy efficiency

- Pollution prevention and control

- Environmentally sustainable management of living natural resources and land use

- Terrestrial and aquatic biodiversity conservation

- Clean transportation

- Sustainable water and wastewater management

- Climate change adaptation

- Circular economy adapted products, production technologies, and processes

- Green buildings5

The Social Bond Principles (SBP) guidelines also provide a list of common project categories such as affordable basic infrastructure and access to essential services, but also advises that eligible social projects can“…directly aim to address or mitigate a specific social issue and/or seek to achieve positive social outcomes especially but not exclusively for a target population(s).”6 Thus, the expectation is that the purpose of the project is to create a positive impact that might not otherwise have been made.

When issuing a GSS Bond, a corporate issuer typically provides information on its approach to sustainability and how the issuance helps it achieve its goals. Often, an external firm provides a “Second Party Opinion” assessing how the bond aligns with criteria such as GBP or SBP and whether the issuer’s framework is credible. An important component of the issuer’s offer is the commitment to periodic market updates about the use of funds to ensure accountability to the markets that the bond proceeds were used as intended.

Somewhat newer on the scene are the Sustainability-Linked Bonds (SLB). Unlike the GSS Bonds noted previously, the proceeds from SLBs are intended to be used for general purposes. However, the structure of the bond includes a “step-up” in which the issuer will pay a higher coupon, effectively increasing the cost of financing, if certain pre-determined sustainability targets are not met within the designated period. This structure suggests the issuer is committed to meeting its targets and investors should expect to see improvements in the organization’s sustainability-related programs and outcomes as a result.

WHAT IS A “GREENIUM?”

Given the explosion of interest in ESG investing, many investment funds and accounts have embraced ESG factors in their investment mandates. As we explained in our review of ESG factors in ESG 101, the use of ESG in the investment process is a broad term, and can be applied to any asset class, geography, or entity. In the case of fixed income, Green Bonds are clearly identifiable as focused on environmentally friendly projects. The demand for such bonds has outstripped available supply, leading to a slight premium or “Greenium” for these bonds, compared to the “regular” bonds by the same issuer. For issuers, this could make issuing a GSS Bond slightly cheaper and more attractive than a “plain vanilla” bond. However, the Greenium for Green Bonds may not continue as overall supply of GSS increases. For example, a recent analysis of Euro-denominated corporate Green Bonds against the non-green benchmark, showed the spread steadily tightening over the 12 months, April 2020 – April 2021. Green Bond issuance increased 41% year-over-year over a similar time period.7 Social and Sustainability Bond issuances appear to be increasing faster and may continue to garner a premium if demand for the bonds remains strong.

1919 INVESTMENT COUNSEL’S APPROACH TO SUSTAINABLE FINANCE

At 1919 Investment Counsel, we are interested in GSS Bonds for not only the potential for positive returns, but also the probable positive impacts from the resulting capital expenditures. This is especially the case for Green Bonds where the proceeds contribute to the energy transition movement. We are mindful of ICMA’s Principles and Guidelines in our analysis and review of relevant issuances. Our dedicated Responsible Investing research team reviews each GSS Bond and the issuer’s stated approach to sustainable debt, before it is purchased, while our Credit Research team screens the bond from a traditional credit view, examining factors such as ratings, liquidity, and maturity. Both of these teams monitor developments in the sustainable finance market, and exciting newer structures such as “Blue Bonds” designed to raise funds exclusively for projects deemed ocean-friendly, and “Diversity and Inclusion” bonds brought to market specifically through minority and women owned brokers. Our combination of expertise and dedication to providing thoughtful counsel enables our clients to gain exposure to the still evolving and impactful universe of sustainable finance.

ALISON BEVILACQUA

Principal, Head of Social Research

Alison is a Principal at 1919 Investment Counsel, LLC and the Head of Social Research. Alison leads the firm’s team of Responsible Investing analysts and SRI Committee to provide research and client service with respect to Values-oriented evaluations, Environmental, Social, and Governance factors, and Impact investing. Alison is a member of the 1919ic Proxy Committee.

Alison joined the firm in 1996 after working the staff of a multi-disciplinary university-based group pursuing development of an undergraduate business school curriculum that embraced sustainability.

Alison serves on the Governing Board of the Interfaith Center on Corporate Responsibility. Alison regularly represents the firm at meetings of socially responsible investing-related organizations.

Alison earned her B.A. from the University of Arizona and M.A. in Economics at Miami University.

BAYLOR LANCASTER-SAMUEL

Vice President, Credit Analyst

Baylor is a Vice President at 1919 Investment Counsel, LLC. Her primary responsibility is to conduct research on all taxable credit for the fixed income strategies. In addition to publishing commentaries on her coverage universe, Baylor is a member of the Fixed Income Committee and Third Party Committee. Baylor has an extensive background in credit research, with prior experience in institutional, family office, independent research, and rating agency roles. Baylor is a member of 100 Women in Finance and the Fixed Income Analysts Society, Inc. (FIASI).

Baylor earned a B.A. from New York University, College of Arts and Science. She earned an M.B.A in Finance from New York University, Stern School of Business. She also earned an M.A. from the University of Miami.

1 www.climatebonds.net.

2 www.climatebonds.net. Includes bonds aligned with Climate Bond Initiative definitions.

3 www.icmagroup.org/sustainable-finance/ 1919ic is a Member Investor of the GBP SBP Principles.

4 “Guidance Handbook.” June 2021. ICMA.

5 “Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds.” June 2021. ICMA.

6 “Social Bond Principles: Voluntary Process Guidelines for Issuing Social Bonds.” June 2021. ICMA.

7 “Q1 2021 ESG Finance Report: European Sustainable Finance.” Association for Financial Markets in Europe.