Weekly Market Insights 04.11.22

Inflation dominates the markets

Financial Markets

Analysts, investors, and financial journalists alike have been focused on inflation and what it means for the economy and financial markets. The question has become paramount as more Federal Reserve officials make public their concerns about how they, the Fed, have gotten behind in trying to control price pressures. As inflation has risen, markets have behaved just as one might expect. The Dow closed the week down 0.28%, the S&P 500 down 1.27%, and the NASDAQ down 3.86%. The big gainers were Health Care and Energy, while the losers were Communication Services, Consumer Discretionary, Industrials, and Information Technology.

Economics

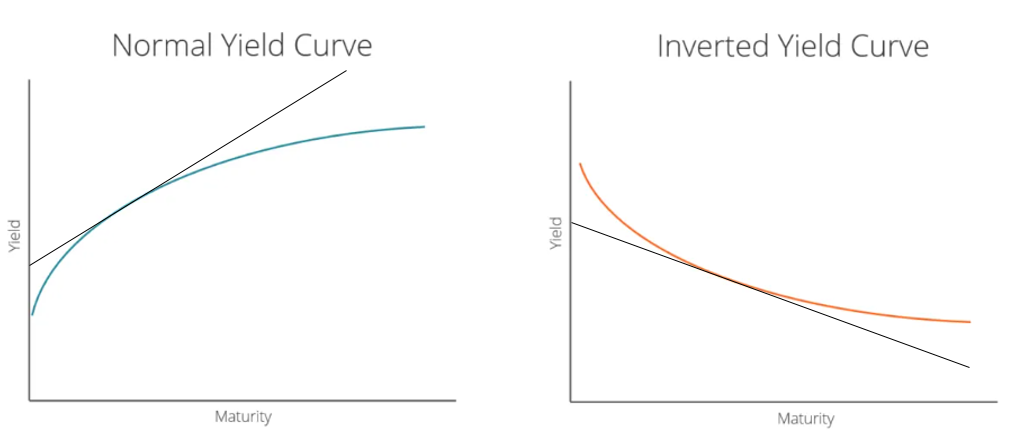

The economic outlook becomes a bit more confusing each week. We promised last week to address the important issue of an inverted yield curve, which we will, but we also want to spend time on inflation, the Fed, and globalism. Most readers are aware that all of these are related. Starting with the yield curve, it is simply a graph showing yield on the vertical axis and maturity on the horizontal axis. The most commonly cited yield curve refers to Treasury securities. Normally, it is positively sloped, meaning lenders demand a higher yield to lend for longer periods of time, but, on occasion, this reverses. Investors consider this phenomenon a harbinger of recession and not without reason. Five of the last six inverted yield curves have preceded a recession, but, importantly, the time from inversion to recession has varied greatly.¹ This remains on the forefront of many investors’ thinking, but there are other elements to consider.

Source: Corporate Finance Institute

The Federal Reserve is undoubtedly a major factor. They control the money supply and short-term interest rates, and, therefore, heavily influence investor thinking and the relation between short and long term rates—in other words, the yield curve. The Fed is clearly in a tightening mode. It seems that each week another Fed governor is being quoted as calling for higher rates. We, at the moment, remain in Chairman Powell’s camp, which argues that the most likely short-term path is another 25 basis point hike at the next meeting. Of course, this can quickly change. The Fed does not want to cause a recession by overtightening, but they are committed to reverse the trend of inflation.

We have written a lot about inflation and its causes. Certainly, an important cause is this enormous amount of liquidity in the system, and it is the Fed’s job to reduce it. Sudden shocks to the monetary system like aggressive tightening will indeed reduce excess money supply, but it will also increase the likelihood of a recession. It is important for the Fed to consider if there are other reasons for the inflationary pressures. Our view is that there are. Along with excess liquidity, the global economy has not recovered from the economic effects of the pandemic, which created havoc for supply chains, global transportation, labor markets, and, of course, energy. All are contributors to higher inflation.

Any interruption in production or transportation is inflationary but very likely to be temporary and self-correcting. Employment shortages are another cost push inflation factor. Interestingly, even as COVID restrictions have been lifted, employees have not returned to work as quickly as expected. This remains a mystery to analysts. Fortunately, a positive development is that labor force participation rates appear to be improving, and this should remove some of the upward wage pressure we have been seeing. In the past, we have written about our view of a boom in the use of technology and innovation. They will be important factors in improved efficiency in the intermediate and longer-term. Unfortunately, the Fed is not particularly concerned with the intermediate or long-term at the moment.

Globalism is a largely misunderstood concept. It can be a positive for all economies, but it must be handled correctly. It keeps prices down, distributes production to the most efficient producers, and forces domestic producers to invest in efficient technology and their work forces. The rise in energy prices has been a huge contributor to inflation, and solving the energy shortages will be difficult because of the many reasons for shortages.

The Ukraine-Russia conflict is one primary problem that only time will solve. The United States, although a large producer, is just one of many countries that can influence prices. It takes time to develop more productive capacity, and it wasn’t very long ago that oil producers were under fire for overproduction. Now, they are feeling the heat for not producing more. It’s really no one’s fault, but, often when the economics change, so do attitudes, and peoples’ views can be a bit paradoxical. There are plenty of energy sources, but it takes both time and technical advances to clean our most abundant resources, and, of course, the end of the conflict will go a long way in reducing shortages.

For those readers who want an excellent overview of changes in the energy world, we highly recommend, The New Map: Energy, Climate and the Clash of Nations, by Daniel Yergin. In any case, we remain in the camp that a recession is not in the near future.

Read PDF here.

¹Barron’s April 4, 2022