Weekly Market Insights 04.15.24

Inflation, the Fed, and Interest Rates

Financial Markets

United States equity markets were hit hard this past week, driven by fears that persistent inflation remains a very real threat. Leading into the weekend, there were also concerns about Iran entering the fray in the Middle East which turned out to be correct. The S&P 500 fell 1.56%, the Dow fell 2.37%, and the NASDAQ fell 0.45%. Recent economic data points have not been ambiguous. Inflation reports, led by energy prices, have come in higher than expected, and employment data continues to indicate a tight labor market. This information, along with hawkish comments from some Fed officials, has investors very concerned. Economic indicators are quite volatile, in the post-COVID era especially, so it takes more than a month or two to confirm a trend. We continue to believe the Fed is on the right track.

Economics

Most recent economic releases show the United States economy continues on a positive path, counterintuitively disappointing investors who are hoping for rate cuts sooner rather than later. It will be a very interesting exercise to see how the latest quarter’s earnings reports come in. If they are reasonably strong, investors will have to decide whether they are more inclined to follow earnings or interest rates.

The European Central Bank (ECB) did not lower rates after its most recent meeting. The European economy has lagged the U.S., and they gave every indication that a rate cut is near.

Asia is a very interesting study. China, as most are aware, is having quite a difficult time economically, while the countries on the periphery are doing quite well. This must be vexing for President Xi Jinping, who has been diligently trying to convince these countries that China is the hub of economic success for them. This, and the difficulties of the “Belt and Road” program, will be hard to overcome.

We wrote last week that we would cover some important topics that may arise during the presidential campaign, one of which is the independence of the Federal Reserve. The Fed’s first job is to keep inflation under control. This, of course, is achieved by controlling the money supply, and one tool the Fed uses to do this is raising or lowering the Fed Funds Rate.[1] Since its inception in 1913, the Fed has assumed other duties, principally trying to ensure non-inflationary full employment. One of the major reasons the Fed strives to act independently of political influences is because political interests and economic interests of the country may differ broadly. For example, in an election year, the economy may be on the verge of overheating. In this case, the Fed’s obligation should be to raise interest rates in order to slow the economy and raise unemployment. Clearly, an incumbent president would want to keep interest rates low, even if it’s not the best long-term decision for the economy. This may drive an economy into hyper-inflation. The point being, what is good for an election bid may not be good for the economy, and, therefore, the country.

Conclusion

The market appears to be in a state of confusion. There are reasonable arguments on both sides of the interest rate debate. Traders, those who have very short time horizons, rule the roost in these situations. Interestingly, this is sometimes how corrections start. While it is too early to make that call, we will keep readers abreast of the situation.

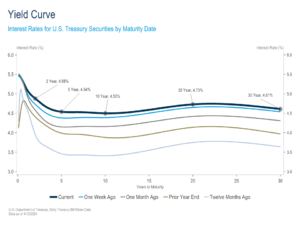

Yield Curve Update

Yields increased significantly over the past two weeks after economic releases stoked fears that sticky inflation, stronger economic growth, and a stubbornly tight labor market may delay or diminish the Fed’s plans for rate cuts this year. Of note, the ISM Manufacturing Index moved back into expansion territory for the first time since September 2022, nonfarm payroll growth accelerated, and the Consumer Price Index (CPI) came in stronger than expected. Hawkish comments from Fed officials suggesting the potential for no or fewer rate cuts this year also contributed to the rise in yields. The 2-year increased 28 basis points, the 10-year increased 32 basis points, and the yield curve inversion stayed relatively constant at -38 basis points over the two week span.

In the most recent week, the increase in yields was primarily driven by Wednesday’s stronger than expected Consumer Price Index (CPI) report. Both the headline and core CPI measures increased 0.4% month-over-month, ahead of consensus for 0.3%, and were unchanged from the prior month. On a year-over-year basis, the headline and core indices increased 3.5% and 3.8%, respectively. Because core CPI strips away volatile food and energy prices, it provides a more consistent view of inflation over time, and, thus, is given more attention from economists—including those at the Fed. While Wednesday’s CPI reading signaled yet again that inflation may prove to be stickier than hoped, the details of the report provide some reason for optimism. Shelter and car insurance prices contributed meaningfully to the stronger than expected core reading, increasing 0.4% and 2.6% month-over-month and 5.7% and 22.2% year-over-year, respectively. This matters because there is reason to believe that both components should normalize over time. For one, the CPI shelter component tends to lag real-time housing and rental data which has declined significantly from its 2022 peak. The other culprit, car insurance, is surging due to prior increases in car prices and pricing responses to driver behavior. In time, we can expect both components to, at the very least, provide less upward pressure on the CPI measures than they are at the present.

The Fed’s preferred inflation gauge, the Personal Consumption Expenditures Index (PCE), will be released later this month, and, while CPI and PCE tend to move in the same directions over time, differences in index construction and methodology can result in significantly different inflation readings for the same period. At 2.5% and 2.8%, respectively, the headline and core PCE measures are running about one percentage point lower than CPI. There will be plenty of economic news and data before the release on the 25th, but the PCE reading will be the next major inflation report for the Fed to consider before its next meeting on May 1st.

Read pdf here.

[1] The federal funds rate is the target interest rate range set by the FOMC. This is the rate at which commercial banks borrow and lend their excess reserves to each other overnight. The FOMC sets a target federal funds rate eight times a year, based on prevailing economic conditions. The federal funds rate can influence short-term rates on consumer loans and credit cards. Investors keep an eye out on the federal funds rate as well because it has an impact on the stock market.