Weekly Market Insights 04.22.24

Markets in Retreat

Equity Markets

United States equity markets struggled this past week, with the S&P 500 falling for the third week in a row and suffering its worst week since March of 2023. Unlike the week before, markets did not try to make a comeback on the final trading day of the week. The Dow increased 0.01%, the S&P 500 fell 3.05%, while NASDAQ fell 5.52%. Last week, we questioned whether this may have been the start of a long-awaited correction, the start of a bear market, or just a minor dip in the market’s normal progression. The unfortunate answer is we don’t know. But, as we write in the economics section, we put the odds in favor of it being a correction or just a normal market move within a larger bull market. Investors would be wise to put the past two weeks in perspective. The S&P 500 is up more than 20% since late October—a significant return in a short amount of time. It should come as no big surprise that traders would be quick to protect profits at any sign of trouble.

Economics

Investors have been frightened by the potential for a hawkish pivot from the Federal Reserve after receiving some stronger than expected inflation data. We believe there are four main factors that have been particularly worrisome for investors. We know we are mixing cause and effect, but it helps explain how investors are reacting at the present:

- The price of energy is rising.

- Labor markets remain strong.

- Fed governors have become more tepid in their pronouncements on rate cuts.

- And, of course, global instability.

We have discussed each of these factors in the past. Yes, rising energy prices are a problem, but this is out of the hands of the Fed. So, it is not quite as big a factor as one might think. The labor market remains strong. This may be a concern as it relates to wages and services inflation and should be carefully watched. However, the labor market, along with many other cyclical parts of the economy, move slowly and almost never in a straight a straight line. Fed officials regularly comment on the state of economy, and, for the most part, what they have said has not been earth shattering. A good suggestion may be to focus more on what Jerome Powell, the Fed Chair, has to say.

Global instability is seldom a positive. In the United States, the economy, dollar, and markets have generally been safe havens and remain so. A large measure of confidence should come from the House passing the Ukraine/Israel funding bill over the weekend, with the Senate likely to approve the legislation early this week.

Conclusion

Although it may be unsettling, watch the progress or regress of both conflicts overseas, as they have a lot to do with both inflation and international trade. There is very little doubt that the Fed’s current bias is towards rate cuts rather than hikes, but investors must remember that the consequences for moving too fast are far greater than going too slow.

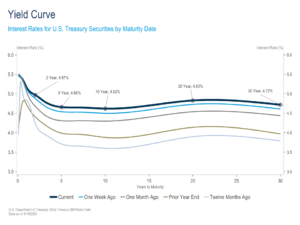

Yield Curve Update

Yields rose this past week, continuing on the upward trend that has been in place for the last month. Over the course of the week, the 2-year yield increased 9 basis points, the 10-year yield increased 10 basis points, and the yield curve inversion remained relatively constant at -37 basis points. The rise in yields has been much more pronounced over the past month, with the 2-year and 10-year yields increasing by 40 basis points and 42 basis points, respectively.

The driving force behind last week’s moves was the barrage of hawkish “Fedspeak”[1] we received, the most notable of which came from Chairman Powell in his remarks at a policy forum Wednesday. Powell sent a strong signal to the market that the first rate cut may be further away than hoped, suggesting that stronger than expected inflation data to start 2024 has introduced uncertainty over the timing and number of cuts this year. Ultimately, Powell and the Fed will need to see more progress on inflation before cutting rates in order to gain the necessary confidence that inflation is on a sustainable path to their 2% target. Several other Fed officials spoke throughout the week, all more or less reinforcing Chairman Powell’s message that the Fed will keep policy on hold until the incoming data warrants changes.

Stronger than expected economic growth and inflation data so far this year, especially data received over the past few weeks, has pushed out and reduced market expectations for rate cuts this year. While stable economic growth and a strong labor market are certainly symptoms of a healthy economy, the Fed wants to prevent an acceleration to the point of sparking another wave of inflation. Striking this balance is tricky to say the least. The Fed will meet for their May FOMC meeting next week, and, while the Fed Funds Rate will almost certainly be held steady, we will receive valuable updates on where monetary policy is headed. As always, we will keep readers abreast of how the situation develops.

Read pdf here.

[1] The term Fedspeak is what Alan Blinder called “a turgid dialect of English” used by Federal Reserve Board chairs in making wordy, vague, and ambiguous statements.