Weekly Market Insights 08.28.23

Markets Struggle with Good News

Financial Markets

The long-awaited Jackson Hole meeting came and went, and Chairman Powell’s speech, although not particularly bullish, was far from bearish. Throughout the week, there were a number of positive economic reports. Earnings reports were generally fine and the market ended mixed. The Dow lost 0.45%, the S&P 500 gained 0.82%, and the NASDAQ Composite gained 2.26%. Given the events of the week, one could have expected better. There are a number of reasons for this muted market reaction. Some have argued that August is almost always a bad month for the markets because so many investors are on vacation. That is certainly possible, but there are also some concerning factors, both domestic and global, investors must consider.

Economics

As we mentioned, while Chairman Powell’s speech at Jackson Hole was not particularly positive, it was certainly not bearish. To this point, the Wall Street Journal published an article headlined, “Some Fed Officials Are Turning Cautious about Raising Rates Too High.” A balanced stance from the Federal Reserve should help soothe the concerns of investors who feared that Powell would take a more hawkish position. Former St. Louis Fed President James Bullard noted no screaming bull has argued that recession fears have been overblown. There are of course good arguments on the other side.

The view from Europe is less sanguine than in the United States. Christine Lagarde, head of the European Central Bank (ECB), said at Jackson Hole that the recent upheaval in the global economy threatens to result in long lasting changes, keeping inflationary pressures higher than normal. Europe is behind the United States in fighting inflation, and its largest economic engine, Germany, is faced with an economic slowdown, which could influence Ms. Lagarde’s view.

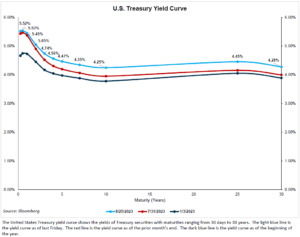

The Yield Curve

Starting this week, we will be including a chart of the United States Treasury yield curve at the end of each update. Our discussion on this topic begins with a relatively basic explanation of the yield curve and moves on to what many investors view as its predictive powers. The yield is a useful and complex tool. It shows the yield on Treasury securities with maturities ranging from 30 days to 30 years. The increase in yield from one maturity to the next is called the term premium, and the size of the term premium most often indicates investors’ expectations for inflation. It graphically measures the time value of money because Treasuries do not carry default risk. This curve is usually upward sloping because lenders require a higher yield to compensate for inflation uncertainty and the related risk of interest rate changes over time. Two major reasons the slope and/or level of the curve can change are Fed policy and variances in economic activity changing the demand for money. There are of course other reasons, but, in trying to judge the path of the economy, analysts concentrate on the slope. For this, we will look at the two ways the Fed influences the slope of the curve and why.

Today the yield curve is inverted with short-term rates higher than long-term, and historically there has been a very powerful correlation between an inverted yield curve and an eventual recession. However, correlation is not causation, and even though historical evidence argues strongly that a recession is nigh, it is not absolute. The argument that a recession is not inevitable is the last economic cycle was interrupted by the pandemic, which caused structural changes in the economy, making monetary policy less effective than in the past. The restart of global supply lines, the reemergence of global trade, and U.S. government‘s spending programs may provide enough fiscal stimulus to offset or balance the Fed’s current restrictive monetary policy stance.

International

The international economy is by far the most interesting to analyze. The recent changes in the Chinese government and economy have been stunning. China has gone from what many observers thought to be the heir-apparent to the United States, in terms of economic leadership, to that of Japan of the 90’s. This transition and recent efforts from the BRICS (Brazil, Russia, India, China, and South Africa) group of nations to develop a country economic organization mimicking the World Bank and the International Monetary Fund have been fascinating to follow. Next week, we will spend more time on these issues.

Conclusion

Recession or no recession remains an open question with powerful arguments on both sides. The Fed did not make any decisive comments at Jackson Hole, and they really shouldn’t have. Inflation is coming down, and economic activity should slow as the impacts of restrictive monetary policy continue to materialize throughout the economy. But, there are plenty of signs that the economy remains strong. The European Union is in the midst of fighting inflation with the odd circumstance that their most economically powerful member country is mired in recession. China continues to weaken, seemingly without a plan to get out. The United States certainly appears to be in the most favorable economic environment.

Read pdf here.