Weekly Market Insights 10.02.23

A Breakthrough

Financial Markets

After what seemed like ages, Congress made a breakthrough in a temporary funding action by passing a Continuing Resolution. What seemed as perfunctory in years past was held up by a smallish group of ideologues in Congress. Clearly, ideology collapsed, as it became evident that voters were turning against them. Joseph Schumpeter was right. Self-interest trumps all else.

Equity markets proved again that September is historically the worst month for stocks. For the week, the Dow fell 1.34%, the S&P 500 fell 0.74%, while the NASDAQ rose 0.06%. For the month, the respective returns were down 3.50%, 4.87%, and 5.81%. Obviously, it was more than the September curse that frightened investors. The above-mentioned threat of a government shutdown and the FOMC meeting were the major events this month that shook investors. We will cover more about the Fed, the fear of higher rates, and continued inflation in the economics section.

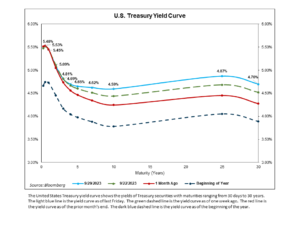

Yield Curve Update

We saw a continuation of the steepening trend that began following the FOMC meeting the week before last, with the curve becoming less inverted by 17 bps. Longer-dated yields rose while shorter-dated yields largely held steady. The “higher for longer” message from the September 20th Fed meeting remains the major factor driving rates higher, but fears over the now-avoided government shutdown and subsequent credit downgrades likely played a role as well.

The Economy

It is often fascinating to observe investor behavior and what is happening in the world. Given what we wrote about how markets behaved in September, readers may be surprised to see some of the headlines from major publications. From the Financial Times: “Fed’s preferred inflation gauge falls to its lowest level since 2021;” “Eurozone inflation falls to lowest rate in almost two years;” “Global bond sell-off eases as investors welcome inflation figures.” This is not an argument that all is right in the financial and investing world, but, rather, a reminder that investors can become tied to an argument that overshadows all else. There are certainly legitimate reasons for concern. The legislation Congress passed is only temporary and they might very well fail to follow through. The Fed, comprised of humans, may overtighten and drive the economy into a recession. Or, the economy may overheat, reignite inflation, and force the Fed into far more serious tightening. The point is that economic markets are social creatures that reflect many things. They can change rapidly or quite slowly.

When analyzing U.S. inflation, there are two interesting issues to consider—energy and housing. As most are aware, energy prices are impacted by global factors. There is very little the Fed, our principal inflation fighter, can do to tame oil prices. Housing, on the other hand, is quite different. There are two factors in the cost of buying a house—the price of the house and the cost of credit. As the cost of credit increases, it should put downward pressure on the price. Standard economics. That has not happened. So what is different this time? While there many forces at work, clearly, home owners with low-rate mortgages are reluctant to lose the advantageous rates and, therefore, unwilling to sell, reducing supply.

Conclusion

Investor sentiment has been down, and there are good reasons. The news cycle is filled with discussions of a government in disarray. Global relations and organizations seem to be rapidly changing, and financial markets have reflected this. All of this is true, but, interestingly, the United States economy appears to currently be in good shape. Employment remains high, inflation is slowing, albeit gradually, but slowing nonetheless. We have argued in the past that it is quite possible that the United States economy is in a state of change, most likely for the better. People, in general, don’t like change. They tend to fear it. This concern is reflected by their behavior in financial markets and in their political choices. Perhaps this is where we are.

Read pdf here.