Weekly Market Insights 11.20.23

Is it Real?

Financial Markets

United States equity markets continued to gain ground this past week as investors became more confident that this rally may be more than a correction. The S&P 500 increased by 2.24%, the Dow by 1.94%, and the tech-laden NASDAQ by 2.37%. The S&P 500 has gained nearly 10% since bottoming on October 27th. Market participants were encouraged by both fundamental and technical news. Last week’s economic releases prompted many analysts to argue that the Fed is on the right track and that the central bank’s efforts to slow the economy and inflation without triggering a recession (i.e. achieve a soft landing) is working.

Economics

Traders and investors had good reason to be enthused this past week. On Tuesday, the Consumer Price Index (CPI) came in lower than expected. The headline number was little-changed, but perhaps more important for market participants was that the core CPI rose less than expected, increasing 0.2% month-over-month rather than the expected 0.3%. Other important economic statistics released this past week were Retail Sales and Unemployment Insurance Claims. Retail Sales moderated relative to the prior month and jobless claims increased more than expected. Taken together, these data points indicated a slowing of the economy, which should be music to Jerome Powell’s ears. Retail Sales numbers can be a bit tricky to analyze. Notably, when the Commerce Department releases Retail Sales figures, they are not inflation-adjusted. This past month’s report is a good example. The headline Retail Sales number fell month-over-month, but Retail Sales (excluding auto fuel spending) increased, defying expectations for a decline. The CPI report received earlier in the week sheds some light on this divergence, as it showed fuel prices fell. That means it is quite possible that at least some of the retail sales decline was simply due to a decline in energy prices rather than a decline in demand. This is just an example of how economic releases can be very difficult to analyze and even misleading if details are ignored.

Politics, of course, remains a wild card. A continuing resolution was passed, but several hurdles remain. Internationally, plenty is happening. The war in Ukraine remains at a stalemate. It is hard to imagine much can change for quite some time. We have had plenty of experience with long drawn-out wars, and now there is the war in the Middle East.

China remains in a very difficult position with no easy way out. We have written a lot about China. The country represents the world’s second largest economy and it is having serious economic problems. We have compared China’s problems to Japan in the 1990’s, but they are far worse. In 1978, when Deng took control of China after Mao’s death, the country began the long journey from peasant economy to modernity. Interestingly, Deng followed in the steps of the Japanese at the end of World War II, only from a far less advanced position. Both built a one-sided economy. In a few weeks, we will discuss these similar paths and where they seriously diverged.

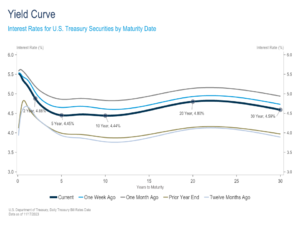

Yield Curve Update

The Treasury yield curve experienced a notable downward shift last week, with intermediate-term maturities declining more than the long and short ends. 2-year yields fell 17 basis points, 5-year yields fell 21 basis points, and 10-year yields fell 18 basis points. The motivation for this week’s moves was economic releases and implications for Federal Reserve monetary policy.

The most significant move came on Tuesday following the release of the October Consumer Price Index (CPI), with both the headline and core CPI measures coming in lower than consensus estimates. The softer inflation data provided market participants with increased confidence that the disinflation trend that has been in place since June of 2022 would continue and added to optimism that the Fed’s rate hiking campaign has concluded. Wednesday’s Retail Sales and Producer Price Index (PPI) reports continued the soft landing momentum. PPI posted a surprise contraction, and, while sales growth declined month-over-month, the drop was less severe than expected. The final notable economic release came on Thursday with jobless claims increasing more than expected and the total number of people filing for unemployment insurance reaching its highest level since November 2021.

Taken together, this week’s economic releases fit the Fed’s ideal situation where we see improved labor market balance, a moderation in consumer demand, and continued disinflation towards their 2% target. Investors’ interest rate and inflation expectations adjusted accordingly, and markets are now completely pricing out a December rate hike along with two rate cuts by July of next year.

Conclusion

Unquestionably, things look better on the inflation front. Markets show investor confidence is improving and corporate earnings have been better than expected. Serious problems certainly remain, but confidence is creeping back into the financial markets. We caution readers to remember that many questions remain unanswered. It appears that the economy is moving in the Fed’s intended direction, but don’t ignore the Chairman’s comments. The Federal Reserve will not tolerate any resurgence in inflation. As we have touched in prior letters, campaign season is upon us and many odd things will be said. Investor sentiment can be easily whipsawed. As to the question posed in the title—we don’t know, but the waters are less muddy.

Read pdf here.